Global Aerospace Materials Market – Industry Trends and Forecast to 2031

Report ID: MS-5 | Aerospace and Defence | Last updated: Jun, 2025 | Formats*:

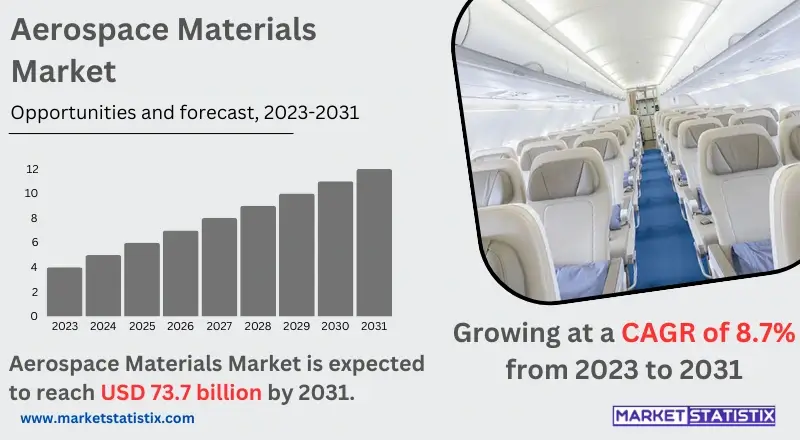

Aerospace Materials Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 8.7% |

| By Product Type | Super Alloys, Steel Alloys, Aluminium Alloys, Composite Materials, Titanium Alloys, Others |

| Key Market Players |

|

| By Region |

Aerospace Materials Market Trends

The aerospace materials market is trending towards the integration of modern lighter materials such as composites, titanium alloys, and aluminium lithium alloys for better aircraft performance and fuel efficiency. These materials help to reduce the weight of aircraft, improving fuel efficiency and increasing the flight range. These materials are demanded from the commercial aviation industry and the military as their users wish to increase the effectiveness of operation and lower the emissions. Another trend is the stubbornness of the marketing strategies, as growing emphasis on sustainability is evident and as the aerospace sector is actively seeking out eco-friendly materials and consideration of recycling practices. Fabricating thermoplastics that can endure harsh environmental stresses and yet are recyclable or naturally sourced is cut out to be the major challenge.Aerospace Materials Market Leading Players

The key players profiled in the report are AMG N.V, ATI Metals., Teijin Ltd., Kobe Steel Ltd, Du Pont, Constellium N.V, Toray Industries Inc., Cytec Solvay group, Aleris, Alcoa CorporationGrowth Accelerators

The aerospace materials market globally includes research, designing. manufacturing, and marketing of aerospace materials. Aerospace materials are materials that are used in the maintenance of the aircraft, or they should have or exhibit certain qualities depending on the service, such as a high strength-to-weight ratio, temperature resistance, corrosion resistance, and fatigue resistance due to the nature of the operation or flight. The range of aerospace materials includes a number of different metals (aluminium, titanium, steel), polymers (carbon prepreg, glass prepreg), and ceramics. The global market for aerospace materials is likely to grow due to new materials and technologies, as the demand for commercial and military aircraft carriers and space vehicles is on the rise for many reasons, such as increased air traffic, advanced technology, and the need for greener and more efficient modes of transportation.Aerospace Materials Market Segmentation analysis

The Global Aerospace Materials is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Super Alloys, Steel Alloys, Aluminium Alloys, Composite Materials, Titanium Alloys, Others . The Application segment categorizes the market based on its usage such as Interior, Propulsion System. Geographically, the market is assessed across key Regions like {regionNms} and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The aerospace materials sector is primarily characterised by the presence of a handful of players producing modern materials such as aluminium, titanium, and composites, as well as some high-performance plastics. Leading companies in the market include Alcoa, Hexcel Corporation, and Toray Industries, which specialise in providing lightweight and high-strength materials that adhere to the high-performance standards of the aviation industry. These firms invest heavily in R&D, seeking to produce new materials that allow for fuel-saving, emission-reducing, and performance-improving engines. The same phenomenon is reflective of the growing consumption of composite materials, which are lighter relative to metals but equally stronger. New players and small-scale companies are powered by technology and collaboration within wise dispersion of their activities; for instance, targets like aerospace 3D printing materials and advanced ceramics have been harnessedChallenges In Aerospace Materials Market

The aerospace materials market is faced with challenges such as the advanced materials that are costly, for example, carbon composites, titanium alloys, and ceramics, among others. These materials are vital in fuel efficiency gain, weight reduction, and aircraft performance elevation, but their manufacturing is costly and consumes a lot of resources. This escalates the overall cost of production for the aerospace companies, and in this regard, pricing becomes paramount, especially for the manufacturers of commercial aeroplanes. Another major challenge is the need to comply with high regulations and safety standards. Diagnostic, therapeutic, and surgical materials are used under extreme environmental conditions (high temperature and pressure variations) and should still provide safety and reliability. New materials, especially composites, are subjected to extensive evaluation, and this, coupled with the long implementation process, may impede the introduction of new materials.Risks & Prospects in Aerospace Materials Market

The aerospace materials market is an attractive one because there is an ever-increasing demand for lightweight yet strong materials to improve onboard performance and efficiency in aircraft, which also translates to less fuel consumption. Today’s composite materials, such as carbon-fibre-reinforced polymers and high-performance alloys, allow manufacturers to decrease the weight of an aircraft without endangering its structural integrity. The higher availability of next-gen aircraft, such as all-electric and hybrid aircraft, enhances the market as there is a need for new materials that possess advanced features and high energy efficiency that can withstand extreme conditions. In addition to that, the environmental strategy being embraced by many countries has presented some market prospects for the development of biocompatible materials and recycling processes for use in aeronautical engineering. Due to pressure on the airlines and the government to reduce carbon footprints, more attention has to be paid to the materials that promote green aviation. This has opened doors for investigation and production of bio composite and other recyclable materials for the aerospace sector to meet changing policies and practices.Key Target Audience

Primary stakeholders of the aerospace materials market comprise manufacturers of aircraft and aerospace parts who need light, durable, and high-functioning materials such as composites, alloys, and polymers. These materials aid in the upsurge of fuel economy and alleviation of weight as well as in the performance of commercial, military, and space worthy vehicles. Players within the industry deal with materials that are required to endure rigorous conditions and at the same time meet the requirements of various laws and safety codes.,, In addition, other important participants are research and development organisations as well as material science companies, which deal with innovations such as advanced composites and nanomaterials intended to enhance the designs of aircraft. We also have the government and its agencies and regulatory bodies that lay out laws on the standardisation of materials used for performance and safety. Similarly, maintenance, repair, and overhaul service providers are also relevant since they also require the aerospace materials in the aircraft they service, so as to enhance their service delivery and safety in the long run.Merger and acquisition

The latest movement in the aerospace materials sector has been marked by mergers and acquisitions as a way of improving technological developments and widening the product range. In 2024 also, BAE Systems, which had earlier bought Ball Aerospace for 5.5 billion dollars, helped in reinforcing its science, space, and defence capabilities as the company's political headquarters geospatial and mission systems had just been established. Moreover, it is worth mentioning Parker-Hannifin’s acquisition of Meggitt PLC worth £6.3 billion in 2022, which deepened its range of offers of aerospace and defence components. The rationale for these acquisitions is the strengthening of the positions in the markets as well as expansions in the industry, which is characterised by stiff competition. Also, Airbus Defence and Space strengthened its cyber skills force by purchasing Infodas in March 2024. Amongst the other significant transactions is the THALES’ acquisition of Cobham Aerospace Communications for $1.1 billion with the aim of developing interactive co-cocks for aircraft. These activities make it evident that the aerospace industries are using acquisitions and mergers as strategies to broaden their scope so as to be in the market and meet the changes.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Aerospace Materials- Snapshot

- 2.2 Aerospace Materials- Segment Snapshot

- 2.3 Aerospace Materials- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Aerospace Materials Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Steel Alloys

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Aluminium Alloys

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Composite Materials

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Super Alloys

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Titanium Alloys

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

- 4.7 Others

- 4.7.1 Key market trends, factors driving growth, and opportunities

- 4.7.2 Market size and forecast, by region

- 4.7.3 Market share analysis by country

5: Aerospace Materials Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Interior

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Propulsion System

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

6: Aerospace Materials Market by Aircraft Type

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Military Aircraft

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Business & General Aviation

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Commercial Aircraft

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Helicopters

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

- 6.6 Others

- 6.6.1 Key market trends, factors driving growth, and opportunities

- 6.6.2 Market size and forecast, by region

- 6.6.3 Market share analysis by country

7: Competitive Landscape

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Cytec Solvay group

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Du Pont

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Kobe Steel Ltd

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Teijin Ltd.

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Toray Industries Inc.

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 ATI Metals.

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Constellium N.V

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 AMG N.V

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Aleris

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Alcoa Corporation

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Aircraft Type |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

Which application type is expected to remain the largest segment in the Global Aerospace Materials market?

+

-

How do regulatory policies impact the Aerospace Materials Market?

+

-

What major players in Aerospace Materials Market?

+

-

What applications are categorized in the Aerospace Materials market study?

+

-

Which product types are examined in the Aerospace Materials Market Study?

+

-

Which regions are expected to show the fastest growth in the Aerospace Materials market?

+

-

What are the major growth drivers in the Aerospace Materials market?

+

-

Is the study period of the Aerospace Materials flexible or fixed?

+

-

How do economic factors influence the Aerospace Materials market?

+

-

How does the supply chain affect the Aerospace Materials Market?

+

-