Global Animal Feed Ingredient Market Size, Share & Trends Analysis Report, Forecast Period, 2024-2030

Report ID: MS-818 | Healthcare and Pharma | Last updated: Apr, 2025 | Formats*:

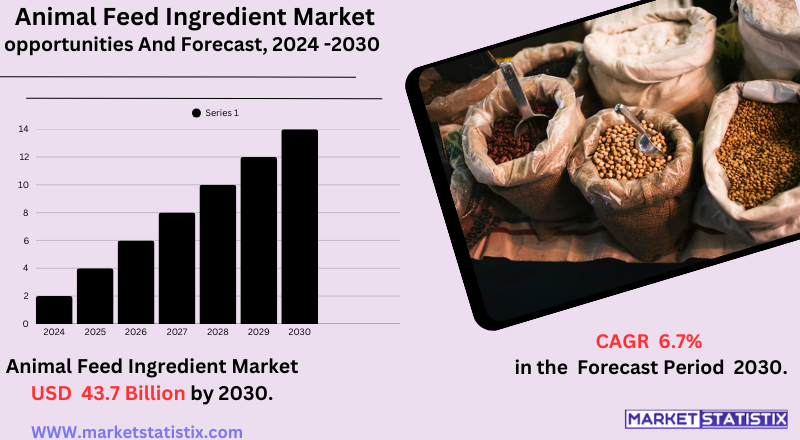

Animal Feed Ingredient Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 6.7% |

| Forecast Value (2030) | USD 43.7 Billion |

| By Product Type | Compound feed, Traditional feed, Premixes |

| Key Market Players |

|

| By Region |

Animal Feed Ingredient Market Trends

The ingredient market in animal feed has been undergoing several major trends affecting its future. One major trend has been that alternative feed ingredients in animal feeding, especially sustainable or eco-friendly feed ingredients, have recently gained attention from researchers and companies alike. Therefore, insect proteins, algae, and plant-based alternative protein sources have been researched to minimise the environmental impact usually associated with regular animal feed ingredients. Besides, there is increasing emphasis on a circular economy that helps to utilise agricultural byproducts or food wastes as alternative feed sources to minimise waste and efficiently utilise resources. Another trend gaining importance is in the field of precision nutrition and customized feed solutions. A combination of advancements in animal nutrition science and technology has facilitated the formulation of animal feed that fits the specific character of each animal species and its subgroups at different life stages. This helps in the benefits of animal health, growth performance, and feed efficiency while reducing waste.Animal Feed Ingredient Market Leading Players

The key players profiled in the report are BIOMIN Holding GmbH, BASF SE, Alltech, Inc., Cargill, Incorporated, Lallemand Inc., Evonik Industries AG, DSM, Centafarm SRL, ADM, Kemin Industries, Inc., Nutreco, Adisseo, Ajinomoto Co., Inc., Novonesis., ElancoGrowth Accelerators

The rapidly rising demand from the global marketplace for animal-based products moves this market toward the consumption of animal-feed ingredients. Since the population is growing and per capita income is rising in developing countries, the intake of meat, dairy products, and eggs is being consumed more each passing day. The high-pressure demand for these products would lead to higher requirements for quality animal feed by livestock and aquaculture for the growth and productivity of these biotic components. Awareness of the nutritional value of meats and dairy products would bring consumers to seek better quality in animal protein, which would, in turn, show its impact on increased demand for nutrient-rich feed ingredients. Health and well-being considerations for animals are another major factor in the advancement of animal nutrition science. Finally, having recognised the importance of feeding a balanced and nutritious diet to livestock, many of them are adopting this practice for improved health, better feed efficiency, and prevention of diseases. As a result, there is increased demand for specialised feed ingredients such as vitamins, minerals, amino acids, and enzymes that improve animal performance while minimising antibiotic use.Animal Feed Ingredient Market Segmentation analysis

The Global Animal Feed Ingredient is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Compound feed, Traditional feed, Premixes . The Application segment categorizes the market based on its usage such as Pigs, Chickens, Cattle. Geographically, the market is assessed across key Regions like {regionNms} and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive landscape of the animal feed ingredient market is characterised by a mix of global giants and regional players, thus rendering a moderately fragmented industry. Major players include companies such as Cargill, ADM (Archer Daniels Midland), BASF, DSM, and Evonik Industries, which have an extensive international reach and a large variety of feed ingredients. These companies typically have integrated supply chains, substantial research and development capabilities, and far-reaching distribution networks that enable them to serve various animal species and geographic regions. However, competition is tough from the local and specialised ingredient manufacturers with a focus on specific product types or regional markets. In some major livestock- and aquaculture-producing countries, this regional competition can be very tough. Pricing, innovative products (such as the development of sustainable and alternative ingredients), nutritional expertise, and sound customer relationships have been key determinants for gaining market share and maintaining it.Challenges In Animal Feed Ingredient Market

Several challenges hinder the growth and stability of the animal feed ingredient market. The main problem is the volatile raw material prices of some key animal feed ingredients like corn, soy, and wheat. Such price fluctuations arise from unpredictable weather conditions, global disruptions in supply chains, and geopolitical tensions; they make it virtually impossible to stabilise production costs and profit margins for manufacturers. The increased cost of feed, which constitutes up to 70% of the total production cost, keeps increasing pressure on producers and livestock farmers, especially in developing regions with diminished purchasing power. The other major challenge resides in further tightening regulations and changing consumer perspectives. Regulatory bodies in various regions have placed strict limits on the use of antibiotics and some additives in animal feed, leaving the manufacturers to turn towards alternative solutions like probiotics, prebiotics, and natural supplement alternatives. The perennial concerns today are the safety of feed and food, animal welfare, and environmental concerns; all these put continuous pressure on manufacturers to innovate and adapt.Risks & Prospects in Animal Feed Ingredient Market

The key drivers for this are intensifying productive livestock-dominated industries, innovations in feed formulation technologies, and an increased interest in animal health and nutrition. Sustainable and alternative proteins – such as plant-based and insect-based proteins, along with functional additives like probiotics for remodelling an industry – also gain widespread acceptance. By region, Asia-Pacific has been topping both sales and volume in the animal feed ingredient market, accompanied by the fast growth of slaughter space, feeding need, and increasing government incentives for feed quality improvements in some key countries such as China, India, and Japan. North America is expected to have the highest growth rate in acceptance and use of new feed technologies and precision nutrition practices, yet Europe still ranks among the largest markets owing to its specialised livestock sectors in addition to legally mandated regulations in animal and food safety. Each has its own drivers, as well as problems, making it ideal for each market player to set up strategies that fit the unique dynamics of each region.Key Target Audience

, The commercial animal feed ingredient market is primarily targeted at groups such as livestock farmers, aquaculture farmers, pet food manufacturers, and commercial feed producers. All these groups demand ingredients such as amino acids, vitamins, minerals, and probiotics to ensure animal health, enhance growth rates, and improve feed efficiency. The major factors affecting their buying decisions include ingredient quality, nutritional benefits, price stability, and compliance with safety standards, as well as a growing preference for natural and sustainable feed options., Regulatory agencies, research institutions, and feed additive developers are also important secondary audiences. This group of stakeholders influences innovations and compliance in the market toward the ideals of cleaner labels, functional ingredients, and solutions liberating antibiotics in feeding. Furthermore, with consumers standing today towards more ethically produced animal products, feed ingredient companies have to become more compliant and attuned to evolving standards and sustainability goals to remain competitive and relevant, not only to their direct buyers but also in the interests of influential regulatory bodies.Merger and acquisition

Recently, there has been widespread merger and acquisition activity in the market for animal feed ingredients, mainly through companies that desire to build product portfolios and secure stronger market positions. General Mills paid approximately $1.45 billion for the acquisition of Cloud Star and Tiki Pets from Whitebridge Pet Brands, making this move its fifth foray into the pet-food market. This move is highly strategic for General Mills as it solidifies the company's ability to earn revenue from premium wet cat food, which is the highest-growth category in its fast-growing U.S. premium pet food market, where estimates project growth from about $150 billion in 2024 to $200 billion by 2030. Phibro Animal Health has further announced an agreement to buy the medicated-feed-additive product portfolio of Zoetis for the value of $350 million. The deal, which will be closed soon, is expected to boost Phibro's margins and EBITDA profit margins and may boost adjusted per-share earnings by at least 60 cents in its first year. The acquired portfolio, which chalked up around $400 million in revenue in 2023, complements Phibro businesses mainly in nutritional specialities and vaccines. These moves show the industry trend toward consolidation and diversification to serve changing consumer needs while also pursuing sustainable growth. >Analyst Comment

The market for animal feed ingredients has kept on growing steadily as it translates to increasing global demand for high-quality animal protein, developments in feed formulation technology, and an upsurge in livestock production. The market in 2025 is pegged at about USD 42.7 billion in value and is estimated at USD 60.2 billion by 2035. The most important ones for this growth include the greater emphasis on richer protein diets, the increased acceptance of greener sustainable feed additives, and the fast-growing demand for meat-based food items in developing economies, such as India and China. Soybean meal and fish meal, among protein-based feed ingredients, are still very important because they are crucial to animal nutrition.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Animal Feed Ingredient- Snapshot

- 2.2 Animal Feed Ingredient- Segment Snapshot

- 2.3 Animal Feed Ingredient- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Animal Feed Ingredient Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Traditional feed

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Compound feed

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Premixes

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Animal Feed Ingredient Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Chickens

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Pigs

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Cattle

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Competitive Landscape

- 6.1 Overview

- 6.2 Key Winning Strategies

- 6.3 Top 10 Players: Product Mapping

- 6.4 Competitive Analysis Dashboard

- 6.5 Market Competition Heatmap

- 6.6 Leading Player Positions, 2022

7: Company Profiles

- 7.1 ADM

- 7.1.1 Company Overview

- 7.1.2 Key Executives

- 7.1.3 Company snapshot

- 7.1.4 Active Business Divisions

- 7.1.5 Product portfolio

- 7.1.6 Business performance

- 7.1.7 Major Strategic Initiatives and Developments

- 7.2 Ajinomoto Co.

- 7.2.1 Company Overview

- 7.2.2 Key Executives

- 7.2.3 Company snapshot

- 7.2.4 Active Business Divisions

- 7.2.5 Product portfolio

- 7.2.6 Business performance

- 7.2.7 Major Strategic Initiatives and Developments

- 7.3 Inc.

- 7.3.1 Company Overview

- 7.3.2 Key Executives

- 7.3.3 Company snapshot

- 7.3.4 Active Business Divisions

- 7.3.5 Product portfolio

- 7.3.6 Business performance

- 7.3.7 Major Strategic Initiatives and Developments

- 7.4 Alltech

- 7.4.1 Company Overview

- 7.4.2 Key Executives

- 7.4.3 Company snapshot

- 7.4.4 Active Business Divisions

- 7.4.5 Product portfolio

- 7.4.6 Business performance

- 7.4.7 Major Strategic Initiatives and Developments

- 7.5 Inc.

- 7.5.1 Company Overview

- 7.5.2 Key Executives

- 7.5.3 Company snapshot

- 7.5.4 Active Business Divisions

- 7.5.5 Product portfolio

- 7.5.6 Business performance

- 7.5.7 Major Strategic Initiatives and Developments

- 7.6 Lallemand Inc.

- 7.6.1 Company Overview

- 7.6.2 Key Executives

- 7.6.3 Company snapshot

- 7.6.4 Active Business Divisions

- 7.6.5 Product portfolio

- 7.6.6 Business performance

- 7.6.7 Major Strategic Initiatives and Developments

- 7.7 BASF SE

- 7.7.1 Company Overview

- 7.7.2 Key Executives

- 7.7.3 Company snapshot

- 7.7.4 Active Business Divisions

- 7.7.5 Product portfolio

- 7.7.6 Business performance

- 7.7.7 Major Strategic Initiatives and Developments

- 7.8 BIOMIN Holding GmbH

- 7.8.1 Company Overview

- 7.8.2 Key Executives

- 7.8.3 Company snapshot

- 7.8.4 Active Business Divisions

- 7.8.5 Product portfolio

- 7.8.6 Business performance

- 7.8.7 Major Strategic Initiatives and Developments

- 7.9 Cargill

- 7.9.1 Company Overview

- 7.9.2 Key Executives

- 7.9.3 Company snapshot

- 7.9.4 Active Business Divisions

- 7.9.5 Product portfolio

- 7.9.6 Business performance

- 7.9.7 Major Strategic Initiatives and Developments

- 7.10 Incorporated

- 7.10.1 Company Overview

- 7.10.2 Key Executives

- 7.10.3 Company snapshot

- 7.10.4 Active Business Divisions

- 7.10.5 Product portfolio

- 7.10.6 Business performance

- 7.10.7 Major Strategic Initiatives and Developments

- 7.11 Centafarm SRL

- 7.11.1 Company Overview

- 7.11.2 Key Executives

- 7.11.3 Company snapshot

- 7.11.4 Active Business Divisions

- 7.11.5 Product portfolio

- 7.11.6 Business performance

- 7.11.7 Major Strategic Initiatives and Developments

- 7.12 Novonesis.

- 7.12.1 Company Overview

- 7.12.2 Key Executives

- 7.12.3 Company snapshot

- 7.12.4 Active Business Divisions

- 7.12.5 Product portfolio

- 7.12.6 Business performance

- 7.12.7 Major Strategic Initiatives and Developments

- 7.13 DSM

- 7.13.1 Company Overview

- 7.13.2 Key Executives

- 7.13.3 Company snapshot

- 7.13.4 Active Business Divisions

- 7.13.5 Product portfolio

- 7.13.6 Business performance

- 7.13.7 Major Strategic Initiatives and Developments

- 7.14 Evonik Industries AG

- 7.14.1 Company Overview

- 7.14.2 Key Executives

- 7.14.3 Company snapshot

- 7.14.4 Active Business Divisions

- 7.14.5 Product portfolio

- 7.14.6 Business performance

- 7.14.7 Major Strategic Initiatives and Developments

- 7.15 Nutreco

- 7.15.1 Company Overview

- 7.15.2 Key Executives

- 7.15.3 Company snapshot

- 7.15.4 Active Business Divisions

- 7.15.5 Product portfolio

- 7.15.6 Business performance

- 7.15.7 Major Strategic Initiatives and Developments

- 7.16 Adisseo

- 7.16.1 Company Overview

- 7.16.2 Key Executives

- 7.16.3 Company snapshot

- 7.16.4 Active Business Divisions

- 7.16.5 Product portfolio

- 7.16.6 Business performance

- 7.16.7 Major Strategic Initiatives and Developments

- 7.17 Kemin Industries

- 7.17.1 Company Overview

- 7.17.2 Key Executives

- 7.17.3 Company snapshot

- 7.17.4 Active Business Divisions

- 7.17.5 Product portfolio

- 7.17.6 Business performance

- 7.17.7 Major Strategic Initiatives and Developments

- 7.18 Inc.

- 7.18.1 Company Overview

- 7.18.2 Key Executives

- 7.18.3 Company snapshot

- 7.18.4 Active Business Divisions

- 7.18.5 Product portfolio

- 7.18.6 Business performance

- 7.18.7 Major Strategic Initiatives and Developments

- 7.19 Elanco

- 7.19.1 Company Overview

- 7.19.2 Key Executives

- 7.19.3 Company snapshot

- 7.19.4 Active Business Divisions

- 7.19.5 Product portfolio

- 7.19.6 Business performance

- 7.19.7 Major Strategic Initiatives and Developments

8: Analyst Perspective and Conclusion

- 8.1 Concluding Recommendations and Analysis

- 8.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Animal Feed Ingredient in 2030?

+

-

Which type of Animal Feed Ingredient is widely popular?

+

-

What is the growth rate of Animal Feed Ingredient Market?

+

-

What are the latest trends influencing the Animal Feed Ingredient Market?

+

-

Who are the key players in the Animal Feed Ingredient Market?

+

-

How is the Animal Feed Ingredient } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Animal Feed Ingredient Market Study?

+

-

What geographic breakdown is available in Global Animal Feed Ingredient Market Study?

+

-

How are the key players in the Animal Feed Ingredient market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Animal Feed Ingredient market?

+

-