Global Automotive Inverter Market Size, Share & Trends Analysis Report, Forecast Period, 2023-2031

Report ID: MS-1793 | Automation and Process Control | Last updated: Oct, 2024 | Formats*:

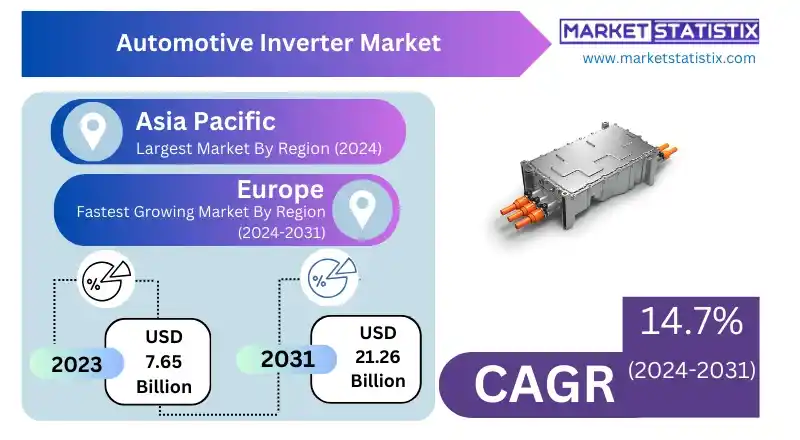

Automotive Inverter Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 14.7% |

| Key Market Players |

|

| By Region |

|

Automotive Inverter Market Trends

The global automotive inverter market is experiencing significant growth due to the increasing adoption of electric vehicles (EVs) and hybrid vehicles. Automotive inverters, which convert battery direct current (DC) power to alternating current (AC) for driving electric motors, are critical components in these vehicles. However, as the automotive industry moves towards electric mobility and sustainability, the demand for efficient, high-performance inverters is growing. Important advancements such as silicon carbide (SiC) and gallium nitride (GaN) semiconductors are enhancing energy efficiency and reducing the size and weight of inverters. Another important trend is the integration of advanced inverter technologies with vehicle management systems to enhance overall vehicle performance and energy management. Smart inverters that provide real-time diagnostics, better thermal management, and compatibility with fast-charging systems are increasingly becoming essential.Automotive Inverter Market Leading Players

The key players profiled in the report are GNK Automotive, Borgwarner Inc., NXP Semiconductors, STMicroelectronics, Robert Bosch, Danfoss, Infineon, Marelli, Lear Corporation, Mitsubishi Electric Corporation, Nissan Motor Corporation, VALEO, Continental AG, Denso Corporation, Toyota Industries Corporation, SensataTechnologies, Inc.Growth Accelerators

The electric cars and hybrid cars’ increased use have effectively created a market mostly geared towards hiring of the power conversion systems since they are more efficient. In automotive, inverters are significant in changing the direct current (DC) of a vehicle's battery into the alternating current (AC) required for electric motors. In essence, as a result of environmental regulations on electric vehicles (EVs) and sustainable transportation options, EVs and hybrids are becoming more in demand, resulting in a corresponding need for advanced inverters that help improve energy efficiency as well as overall vehicle performance. Also, another contributing factor is growth in inverter technology, whereby there is always a call to attain higher power density with efficient heat management capabilities. Semiconductor material innovations, including silicon carbide (SiC) and gallium nitride (GaN), are enhancing inverter performance as well as dependability, making it applicable to high-performance settings too. Besides, an increase in automotive investment in research and development, together with the expansion of charging infrastructure, have been other drivers for the market since these trends promote the adoption of electric cars besides hybrids.Automotive Inverter Market Segmentation analysis

The Global Automotive Inverter is segmented by and Region. . Geographically, the market is assessed across key Regions like North America(United States.Canada.Mexico), South America(Brazil.Argentina.Chile.Rest of South America), Europe(Germany.France.Italy.United Kingdom.Benelux.Nordics.Rest of Europe), Asia Pacific(China.Japan.India.South Korea.Australia.Southeast Asia.Rest of Asia-Pacific), MEA(Middle East.Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

In comparison to the traditional incumbents within the global automotive inverter marketplace, there exist both mature automotive electronic product manufacturers and newly emerging technology companies. Infineon Technologies, Renesas Electronics, NXP Semiconductors, and Panasonic dominate this field (semiconductors for vehicles). These enterprises are known for their inverter solutions, which they provide widely as a significant player in automotive semiconductors. They add value through innovation to enable them to retain a firm grip of global market share on fast-growing motorsport conversion factors. Some other players in the market are small-sized ones with specialisation who have interest in producing sophisticated converter technologies only or addressing select segments of this area. Such firms create opportunities for fresh ideas and establish an agile competitive space, giving way towards uniqueness in the car transducers’ arena.Challenges In Automotive Inverter Market

The global automotive inverter industry is confronted with several critical obstacles that are largely attributable to technological intricacy and expense. Automotive inverters, which convert direct current (DC) into alternating current (AC) for electric as well as hybrid vehicles, need complex technology for their efficacy and dependability. The high expense of producing and integrating such cutting-edge elements may deter some smaller producers or developing economies. Moreover, continued innovation in this area so as to keep pace with the progress in electric vehicle (EV) technology can stretch thin reservoirs and push up development expenditure. In addition, it is necessary for the market to cater to issues surrounding the durability of the components as well as their performances in different environmental conditions. These obstacles inquisitively demand constant research development and joint efforts among automobile manufacturers, suppliers, and technology providers in order to stimulate creativity while also sustaining competitiveness within an industry that changes too fast.Risks & Prospects in Automotive Inverter Market

The worldwide automotive inverter market is undergoing tremendous expansion brought on by the rising embrace of electric (EVs) and hybrid cars. In these types of vehicles, battery-powered direct current (DC) to motor-driven alternating current (AC) conversion is done using inverters, which are very important components. But with the move towards electric mobility and sustainability in the automotive industry, there is an increasing demand for highly efficient, high-performance inverters. Important advances such as silicon carbide (SiC) and gallium nitride (GaN) semiconductors are making them more energy efficient, though smaller and lighter. Another significant trend is integrating advanced inverter technologies into vehicle management systems to improve overall vehicle performance in terms of energy management. Smart inverters that have real-time diagnostics, efficient thermal management capabilities, and fast charging system compatibility have become increasingly important now.Key Target Audience

The aforementioned audience is the main target market for the global automotive inverter market, which includes car manufacturers in the sector of automotive, electric vehicle (EV) producers, and hybrid vehicle developers. Hence, they make use of inverters with which the direct current (DC) from the battery converts to an alternating current (AC) for powering electric engines (inverters). There has been an increasing demand for advanced inverter-generated electric drives due to various factors such as increased efficiency and performance as a result of this transformation.,, Other players include, amongst others, regulators, component suppliers of the automotive industry, and research and development (R&D) institutions who are working on improving technologies used in making car parts; these two parties have their own roles to play in ensuring vehicle manufacturers collaborate with them to develop better technology. For instance, demand for advanced inverter systems able to improve both performance and efficiency is growing as a result of changes in the composition of cars being produced today in order to respond positively to electric and hybrid car challenges.Merger and acquisition

Continuing demand for electric vehicles and the need for advanced power electronics solutions have resulted in notable merger and acquisition trends within the automotive inverter market globally. Key alliances include partnerships between well-known automotive parts suppliers and inverter producers as well as purchases of firms specialising in inverter technology. Objectives of these mergers and acquisitions include improving market shares, widening the range of products on offer, and hastening high-efficiency, low-cost inverter design processes. Some significant examples are tie-ups among major automakers such as Ford and MG, which focused on developing integrated electric powertrain systems that incorporate inverter units. In addition, established automobile manufacturers have purchased start-ups for inverter technologies in order to obtain cutting-edge technologies that can fast track their plans for electrification.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Automotive Inverter- Snapshot

- 2.2 Automotive Inverter- Segment Snapshot

- 2.3 Automotive Inverter- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Automotive Inverter Market by Inverter Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Traction Inverter

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Soft Switching Inverter

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Automotive Inverter Market by Propulsion Type

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Battery Electric Vehicle

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Plug In Hybrid Vehicle

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Hybrid Vehicle

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Automotive Inverter Market by Material Outlook

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Gallium Nitride

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Silicon

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Silicon Carbide

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Others

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

7: Automotive Inverter Market by Power Output

- 7.1 Overview

- 7.1.1 Market size and forecast

- 7.2 upto 200

- 7.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.2 Market size and forecast, by region

- 7.2.3 Market share analysis by country

- 7.3 2 00kW-300kW

- 7.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.2 Market size and forecast, by region

- 7.3.3 Market share analysis by country

- 7.4 Above 400kW

- 7.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.2 Market size and forecast, by region

- 7.4.3 Market share analysis by country

8: Automotive Inverter Market by Vehicle Type

- 8.1 Overview

- 8.1.1 Market size and forecast

- 8.2 Passenger Car

- 8.2.1 Key market trends, factors driving growth, and opportunities

- 8.2.2 Market size and forecast, by region

- 8.2.3 Market share analysis by country

- 8.3 Commercial Vehicles

- 8.3.1 Key market trends, factors driving growth, and opportunities

- 8.3.2 Market size and forecast, by region

- 8.3.3 Market share analysis by country

9: Automotive Inverter Market by Battery Voltage

- 9.1 Overview

- 9.1.1 Market size and forecast

- 9.2 Below 400 V

- 9.2.1 Key market trends, factors driving growth, and opportunities

- 9.2.2 Market size and forecast, by region

- 9.2.3 Market share analysis by country

- 9.3 Above 400 V

- 9.3.1 Key market trends, factors driving growth, and opportunities

- 9.3.2 Market size and forecast, by region

- 9.3.3 Market share analysis by country

10: Automotive Inverter Market by Region

- 10.1 Overview

- 10.1.1 Market size and forecast By Region

- 10.2 North America

- 10.2.1 Key trends and opportunities

- 10.2.2 Market size and forecast, by Type

- 10.2.3 Market size and forecast, by Application

- 10.2.4 Market size and forecast, by country

- 10.2.4.1 United States

- 10.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 10.2.4.1.2 Market size and forecast, by Type

- 10.2.4.1.3 Market size and forecast, by Application

- 10.2.4.2 Canada

- 10.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 10.2.4.2.2 Market size and forecast, by Type

- 10.2.4.2.3 Market size and forecast, by Application

- 10.2.4.3 Mexico

- 10.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 10.2.4.3.2 Market size and forecast, by Type

- 10.2.4.3.3 Market size and forecast, by Application

- 10.2.4.1 United States

- 10.3 South America

- 10.3.1 Key trends and opportunities

- 10.3.2 Market size and forecast, by Type

- 10.3.3 Market size and forecast, by Application

- 10.3.4 Market size and forecast, by country

- 10.3.4.1 Brazil

- 10.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 10.3.4.1.2 Market size and forecast, by Type

- 10.3.4.1.3 Market size and forecast, by Application

- 10.3.4.2 Argentina

- 10.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 10.3.4.2.2 Market size and forecast, by Type

- 10.3.4.2.3 Market size and forecast, by Application

- 10.3.4.3 Chile

- 10.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 10.3.4.3.2 Market size and forecast, by Type

- 10.3.4.3.3 Market size and forecast, by Application

- 10.3.4.4 Rest of South America

- 10.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 10.3.4.4.2 Market size and forecast, by Type

- 10.3.4.4.3 Market size and forecast, by Application

- 10.3.4.1 Brazil

- 10.4 Europe

- 10.4.1 Key trends and opportunities

- 10.4.2 Market size and forecast, by Type

- 10.4.3 Market size and forecast, by Application

- 10.4.4 Market size and forecast, by country

- 10.4.4.1 Germany

- 10.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.1.2 Market size and forecast, by Type

- 10.4.4.1.3 Market size and forecast, by Application

- 10.4.4.2 France

- 10.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.2.2 Market size and forecast, by Type

- 10.4.4.2.3 Market size and forecast, by Application

- 10.4.4.3 Italy

- 10.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.3.2 Market size and forecast, by Type

- 10.4.4.3.3 Market size and forecast, by Application

- 10.4.4.4 United Kingdom

- 10.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.4.2 Market size and forecast, by Type

- 10.4.4.4.3 Market size and forecast, by Application

- 10.4.4.5 Benelux

- 10.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.5.2 Market size and forecast, by Type

- 10.4.4.5.3 Market size and forecast, by Application

- 10.4.4.6 Nordics

- 10.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.6.2 Market size and forecast, by Type

- 10.4.4.6.3 Market size and forecast, by Application

- 10.4.4.7 Rest of Europe

- 10.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 10.4.4.7.2 Market size and forecast, by Type

- 10.4.4.7.3 Market size and forecast, by Application

- 10.4.4.1 Germany

- 10.5 Asia Pacific

- 10.5.1 Key trends and opportunities

- 10.5.2 Market size and forecast, by Type

- 10.5.3 Market size and forecast, by Application

- 10.5.4 Market size and forecast, by country

- 10.5.4.1 China

- 10.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.1.2 Market size and forecast, by Type

- 10.5.4.1.3 Market size and forecast, by Application

- 10.5.4.2 Japan

- 10.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.2.2 Market size and forecast, by Type

- 10.5.4.2.3 Market size and forecast, by Application

- 10.5.4.3 India

- 10.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.3.2 Market size and forecast, by Type

- 10.5.4.3.3 Market size and forecast, by Application

- 10.5.4.4 South Korea

- 10.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.4.2 Market size and forecast, by Type

- 10.5.4.4.3 Market size and forecast, by Application

- 10.5.4.5 Australia

- 10.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.5.2 Market size and forecast, by Type

- 10.5.4.5.3 Market size and forecast, by Application

- 10.5.4.6 Southeast Asia

- 10.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.6.2 Market size and forecast, by Type

- 10.5.4.6.3 Market size and forecast, by Application

- 10.5.4.7 Rest of Asia-Pacific

- 10.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 10.5.4.7.2 Market size and forecast, by Type

- 10.5.4.7.3 Market size and forecast, by Application

- 10.5.4.1 China

- 10.6 MEA

- 10.6.1 Key trends and opportunities

- 10.6.2 Market size and forecast, by Type

- 10.6.3 Market size and forecast, by Application

- 10.6.4 Market size and forecast, by country

- 10.6.4.1 Middle East

- 10.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 10.6.4.1.2 Market size and forecast, by Type

- 10.6.4.1.3 Market size and forecast, by Application

- 10.6.4.2 Africa

- 10.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 10.6.4.2.2 Market size and forecast, by Type

- 10.6.4.2.3 Market size and forecast, by Application

- 10.6.4.1 Middle East

- 11.1 Overview

- 11.2 Key Winning Strategies

- 11.3 Top 10 Players: Product Mapping

- 11.4 Competitive Analysis Dashboard

- 11.5 Market Competition Heatmap

- 11.6 Leading Player Positions, 2022

12: Company Profiles

- 12.1 GNK Automotive

- 12.1.1 Company Overview

- 12.1.2 Key Executives

- 12.1.3 Company snapshot

- 12.1.4 Active Business Divisions

- 12.1.5 Product portfolio

- 12.1.6 Business performance

- 12.1.7 Major Strategic Initiatives and Developments

- 12.2 Borgwarner Inc.

- 12.2.1 Company Overview

- 12.2.2 Key Executives

- 12.2.3 Company snapshot

- 12.2.4 Active Business Divisions

- 12.2.5 Product portfolio

- 12.2.6 Business performance

- 12.2.7 Major Strategic Initiatives and Developments

- 12.3 NXP Semiconductors

- 12.3.1 Company Overview

- 12.3.2 Key Executives

- 12.3.3 Company snapshot

- 12.3.4 Active Business Divisions

- 12.3.5 Product portfolio

- 12.3.6 Business performance

- 12.3.7 Major Strategic Initiatives and Developments

- 12.4 STMicroelectronics

- 12.4.1 Company Overview

- 12.4.2 Key Executives

- 12.4.3 Company snapshot

- 12.4.4 Active Business Divisions

- 12.4.5 Product portfolio

- 12.4.6 Business performance

- 12.4.7 Major Strategic Initiatives and Developments

- 12.5 Robert Bosch

- 12.5.1 Company Overview

- 12.5.2 Key Executives

- 12.5.3 Company snapshot

- 12.5.4 Active Business Divisions

- 12.5.5 Product portfolio

- 12.5.6 Business performance

- 12.5.7 Major Strategic Initiatives and Developments

- 12.6 Danfoss

- 12.6.1 Company Overview

- 12.6.2 Key Executives

- 12.6.3 Company snapshot

- 12.6.4 Active Business Divisions

- 12.6.5 Product portfolio

- 12.6.6 Business performance

- 12.6.7 Major Strategic Initiatives and Developments

- 12.7 Infineon

- 12.7.1 Company Overview

- 12.7.2 Key Executives

- 12.7.3 Company snapshot

- 12.7.4 Active Business Divisions

- 12.7.5 Product portfolio

- 12.7.6 Business performance

- 12.7.7 Major Strategic Initiatives and Developments

- 12.8 Marelli

- 12.8.1 Company Overview

- 12.8.2 Key Executives

- 12.8.3 Company snapshot

- 12.8.4 Active Business Divisions

- 12.8.5 Product portfolio

- 12.8.6 Business performance

- 12.8.7 Major Strategic Initiatives and Developments

- 12.9 Lear Corporation

- 12.9.1 Company Overview

- 12.9.2 Key Executives

- 12.9.3 Company snapshot

- 12.9.4 Active Business Divisions

- 12.9.5 Product portfolio

- 12.9.6 Business performance

- 12.9.7 Major Strategic Initiatives and Developments

- 12.10 Mitsubishi Electric Corporation

- 12.10.1 Company Overview

- 12.10.2 Key Executives

- 12.10.3 Company snapshot

- 12.10.4 Active Business Divisions

- 12.10.5 Product portfolio

- 12.10.6 Business performance

- 12.10.7 Major Strategic Initiatives and Developments

- 12.11 Nissan Motor Corporation

- 12.11.1 Company Overview

- 12.11.2 Key Executives

- 12.11.3 Company snapshot

- 12.11.4 Active Business Divisions

- 12.11.5 Product portfolio

- 12.11.6 Business performance

- 12.11.7 Major Strategic Initiatives and Developments

- 12.12 VALEO

- 12.12.1 Company Overview

- 12.12.2 Key Executives

- 12.12.3 Company snapshot

- 12.12.4 Active Business Divisions

- 12.12.5 Product portfolio

- 12.12.6 Business performance

- 12.12.7 Major Strategic Initiatives and Developments

- 12.13 Continental AG

- 12.13.1 Company Overview

- 12.13.2 Key Executives

- 12.13.3 Company snapshot

- 12.13.4 Active Business Divisions

- 12.13.5 Product portfolio

- 12.13.6 Business performance

- 12.13.7 Major Strategic Initiatives and Developments

- 12.14 Denso Corporation

- 12.14.1 Company Overview

- 12.14.2 Key Executives

- 12.14.3 Company snapshot

- 12.14.4 Active Business Divisions

- 12.14.5 Product portfolio

- 12.14.6 Business performance

- 12.14.7 Major Strategic Initiatives and Developments

- 12.15 Toyota Industries Corporation

- 12.15.1 Company Overview

- 12.15.2 Key Executives

- 12.15.3 Company snapshot

- 12.15.4 Active Business Divisions

- 12.15.5 Product portfolio

- 12.15.6 Business performance

- 12.15.7 Major Strategic Initiatives and Developments

- 12.16 SensataTechnologies

- 12.16.1 Company Overview

- 12.16.2 Key Executives

- 12.16.3 Company snapshot

- 12.16.4 Active Business Divisions

- 12.16.5 Product portfolio

- 12.16.6 Business performance

- 12.16.7 Major Strategic Initiatives and Developments

- 12.17 Inc.

- 12.17.1 Company Overview

- 12.17.2 Key Executives

- 12.17.3 Company snapshot

- 12.17.4 Active Business Divisions

- 12.17.5 Product portfolio

- 12.17.6 Business performance

- 12.17.7 Major Strategic Initiatives and Developments

13: Analyst Perspective and Conclusion

- 13.1 Concluding Recommendations and Analysis

- 13.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Inverter Type |

|

By Propulsion Type |

|

By Material Outlook |

|

By Power Output |

|

By Vehicle Type |

|

By Battery Voltage |

|

Report Licenses

Frequently Asked Questions (FAQ):

How do regulatory policies impact the Automotive Inverter Market?

+

-

What major players in Automotive Inverter Market?

+

-

What applications are categorized in the Automotive Inverter market study?

+

-

Which product types are examined in the Automotive Inverter Market Study?

+

-

Which regions are expected to show the fastest growth in the Automotive Inverter market?

+

-

What are the major growth drivers in the Automotive Inverter market?

+

-

Is the study period of the Automotive Inverter flexible or fixed?

+

-

How do economic factors influence the Automotive Inverter market?

+

-

How does the supply chain affect the Automotive Inverter Market?

+

-

Which players are included in the research coverage of the Automotive Inverter Market Study?

+

-