Global Deployment Automation Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2031

Report ID: MS-46 | Application Software | Last updated: Oct, 2024 | Formats*:

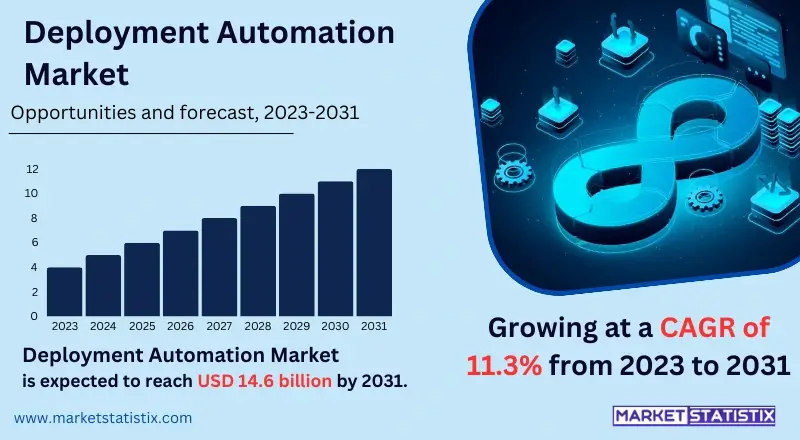

Deployment Automation Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 11.3% |

| Key Market Players |

|

| By Region |

Deployment Automation Market Trends

The market for deployment automation solutions is set to witness a surge in its growth due to the extensive adoption of DevOps by most organizations. Organisations are shifting more of their attention to the delivery of software in a shorter time and with many updates. Consequently, deployment automation tools are seen as crucial for enhancing the processes within the software development life cycle. These tools aid in continuous integration and deployment (CI/CD) by providing capabilities that help teams automate router processes, reduce human factor errors, and promote the interaction between software development and information technology operation departments. A further trend worth mentioning is the growing influence of cloud computing and containerisation in recent deployment automation. As organisations are moving to the cloud and using software containers like Docker or orchestration tools such as Kubernetes, there has been a considerable growth in the use of automated deployment processes that provide management for such environments. This change enables organisations to deliver applications in a more scalable, flexible, and cost-effective way.Deployment Automation Market Leading Players

The key players profiled in the report are Puppet Inc., Chef Software Inc., Ansible Inc., SaltStack Inc., Atlassian Corporation Plc, Red Hat Inc., Microsoft Corporation, IBM Corporation, CA Technologies (Broadcom Inc.), BMC Software Inc., Micro Focus International Plc, GitLab Inc., Flexagon LLC, CloudBees Inc., HashiCorp Inc., XebiaLabs (Digital.ai), JetBrains s.r.o., CircleCI, Octopus Deploy, Electric Cloud Inc.Growth Accelerators

The primary factor propelling the growth of the deployment automation market is the rising need for efficiency as well as speed in all aspects of software development and IT operations. In order to meet their goal of delivering applications and updates in the shortest time possible, deployment automation tools make it possible to implement integration and continuous delivery pipelines. This change tends to promote eliminating boring, repetitive work, thus improving the quality of work done by the teams as they are able to focus on more productive work instead and also fostering better teamwork between development and operations teams (DevOps). In addition, cloud computing has established its demand in the market, and consequently, there is a growing appetite for automated deployment solutions designed to handle intricate multi-cloud setups. With the increase in cyberattacks, there is an urge to implement assured application deployments by automating deployment processes. These elements combined explain the healthy development of the deployment automation industry.Deployment Automation Market Segmentation analysis

The Global Deployment Automation is segmented by Application, and Region. . The Application segment categorizes the market based on its usage such as Retail, IT and Telecommunications, BFSI, Healthcare, Manufacturing, Others. Geographically, the market is assessed across key Regions like {regionNms} and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The market for deployment automation is highly competitive, owing its source to its range of competitors that include the likes of technology behemoths, speciality players, and new upstart businesses. Microsoft, AWS, and IBM command more than 90% of the market thanks to their all-inclusive cloud deployment automation solutions that are developed to work effortlessly with their huge cloud infrastructures. These organisations utilise their huge budgets, technologies, and broad markets to provide deployment solutions that are aimed at different enterprise levels as well as the associated scales, flexibility, and safety. Such companies provide solutions, which include, among other things, CI/CD pipelines, configuration management, and monitoring of applications that increase operational efficiency and reduce the time of getting applications to the market. Besides the larger rivals, the market is not only dominated by the larger ones but also many others, such as Chef, Puppet, and Ansible, among others, who are more towards developing open-source tools and solutions for deployment automation. These organisations focus on developing tools with the support of the community, allowing the users to adapt their deployment process to their needs. The competition is also complicated by new trends such as DevOps and agile that encourage people to automate, which deploys as a manual process. Hence, greater vendor collaboration and emphasis on product development will be essential for providing a competitive edge in the market in response to the needs of companies that wish to improve their deployment processes.Challenges In Deployment Automation Market

The deployment automation market is fraught with a number of the challenges, most importantly, issues surrounding the integration of deployment automation technologies with the existing IT environments. Most organisations combine traditional and new applications, which complicates the application of deployment automation toolsets. It is not easy to integrate the tools into various environments, including the cloud, on-premises, and hybrid, which requires a lot of time and resources. This level of complexity may cause interruptions in deployment timelines and result in increased expenses, making deployment automation less appealing to organisations. The other considerable issue faced by organisations is the lack of skilled human resources and the ability to manage changes. The prompt usage or take-up of deployment automation tools, in most cases, demands professional competences like DevOps expertise, scripting, and configuration management. Most organisations are unable to look for the right people or train them to possess such skills and hence end up engaging third-party consultants or services.Risks & Prospects in Deployment Automation Market

The deployment automation market is poised for substantial growth because organisations are always looking for ways to improve their operating efficiencies and speed up the delivery of software applications to the market. As the demand for quicker and more dependable software development increases, deployment automation solutions eliminate processes that require human involvement, thus minimising the chances of mistakes or inconsistencies in deployment in different environments. In addition, shifting left practices such as those employed in DevOps, which require the collaboration of both the development and operational teams, creates a further need to deploy automation tools that enable CI/CD. Additionally, the increase in the use of cloud computing coupled with microservices architecture is expanding the scope of the deployment automation market. For the most part, the organisations are moving to the cloud and utilising container-based computer systems such as Docker and Kubernetes, which will require the deployment of applications to be done automatically. This change helps the organisation, in this case, to expand its infrastructure rapidly and cater to the demands of the business quickly.Key Target Audience

The primary target audience for deployment automation solutions developed within various IT vendors comprises mainly IT and DevOps Teams in organisations of any size. Their scope of work covers software releases, updates, and infrastructure alterations. Deployment automation tools optimise the work processes of these teams by automating the deployment steps and mitigating the risks of human fallibility while only having a consistent application performance across different environments. While this ensures the working of processes without interruption, the repetitive tasks are taken away from the team members, hence allowing them to devote their efforts on strategic ways of working and working together in software development and delivery instead.,, Furthermore, the cloud service provider and the managed service provider also play the role of targeting this market by availing better deployment options to their consumers. With the progressive need for faster application development and the practice of continuous integration and continuous delivery (CI/CD), it comes as a necessity that automation of deployment technologies is made available in order for enterprises to remain relevant in this cutthroat digital world.Merger and acquisition

The last few years have witnessed considerable merger and acquisition activity within the deployment automation market as firms seek to augment service delivery and grow their market share. Cisco Systems, for example, completed its acquisition of AppDynamics, a premier application performance monitoring solution, in a bid to boost AppDynamics’ automation features as well as offer visibility into application deployment and performance management. This relates to the broader pattern of deployment automation tools being integrated with other industry players cloud solutions offered by large traditional software companies as there is a rise in demand for application delivery. A similar acquisition occurred last year in 2022 when IBM acquired Turbonomic, which focused on application resource management in order to implement its hybrid cloud and automation strategies. This acquisition hoped to further bolster IBM’s capabilities in dealing with the challenges of allocating and managing resources within deep and complex IT ecosystems, thus offering products with regards to deployment automation. These mergers and acquisitions are indicative of the fact that there is an increasing focus on automation of IT operations by the companies, as well as an effort to take advantage of existing technologies and talents to enhance, improve, lessen the turn-around time for deployments, and foster the cause of digitalization. In light of the continuous upsurge in the need for flexible and faster deployment processes, it is expected that there will be more mergers in the deployment automation sector.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Deployment Automation- Snapshot

- 2.2 Deployment Automation- Segment Snapshot

- 2.3 Deployment Automation- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Deployment Automation Market by Application / by End Use

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Retail

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 IT and Telecommunications

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 BFSI

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Healthcare

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Manufacturing

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

- 4.7 Others

- 4.7.1 Key market trends, factors driving growth, and opportunities

- 4.7.2 Market size and forecast, by region

- 4.7.3 Market share analysis by country

5: Deployment Automation Market by Deployment Mode

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 On-Premises

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Cloud

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

6: Deployment Automation Market by Enterprise size

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Small and Medium Enterprises

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Large Enterprises

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

7: Deployment Automation Market by Component

- 7.1 Overview

- 7.1.1 Market size and forecast

- 7.2 Software

- 7.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.2 Market size and forecast, by region

- 7.2.3 Market share analysis by country

- 7.3 Services

- 7.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.2 Market size and forecast, by region

- 7.3.3 Market share analysis by country

8: Competitive Landscape

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 Puppet Inc.

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Chef Software Inc.

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 Ansible Inc.

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 SaltStack Inc.

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Atlassian Corporation Plc

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 Red Hat Inc.

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 Microsoft Corporation

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 IBM Corporation

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 CA Technologies (Broadcom Inc.)

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 BMC Software Inc.

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

- 9.11 Micro Focus International Plc

- 9.11.1 Company Overview

- 9.11.2 Key Executives

- 9.11.3 Company snapshot

- 9.11.4 Active Business Divisions

- 9.11.5 Product portfolio

- 9.11.6 Business performance

- 9.11.7 Major Strategic Initiatives and Developments

- 9.12 GitLab Inc.

- 9.12.1 Company Overview

- 9.12.2 Key Executives

- 9.12.3 Company snapshot

- 9.12.4 Active Business Divisions

- 9.12.5 Product portfolio

- 9.12.6 Business performance

- 9.12.7 Major Strategic Initiatives and Developments

- 9.13 Flexagon LLC

- 9.13.1 Company Overview

- 9.13.2 Key Executives

- 9.13.3 Company snapshot

- 9.13.4 Active Business Divisions

- 9.13.5 Product portfolio

- 9.13.6 Business performance

- 9.13.7 Major Strategic Initiatives and Developments

- 9.14 CloudBees Inc.

- 9.14.1 Company Overview

- 9.14.2 Key Executives

- 9.14.3 Company snapshot

- 9.14.4 Active Business Divisions

- 9.14.5 Product portfolio

- 9.14.6 Business performance

- 9.14.7 Major Strategic Initiatives and Developments

- 9.15 HashiCorp Inc.

- 9.15.1 Company Overview

- 9.15.2 Key Executives

- 9.15.3 Company snapshot

- 9.15.4 Active Business Divisions

- 9.15.5 Product portfolio

- 9.15.6 Business performance

- 9.15.7 Major Strategic Initiatives and Developments

- 9.16 XebiaLabs (Digital.ai)

- 9.16.1 Company Overview

- 9.16.2 Key Executives

- 9.16.3 Company snapshot

- 9.16.4 Active Business Divisions

- 9.16.5 Product portfolio

- 9.16.6 Business performance

- 9.16.7 Major Strategic Initiatives and Developments

- 9.17 JetBrains s.r.o.

- 9.17.1 Company Overview

- 9.17.2 Key Executives

- 9.17.3 Company snapshot

- 9.17.4 Active Business Divisions

- 9.17.5 Product portfolio

- 9.17.6 Business performance

- 9.17.7 Major Strategic Initiatives and Developments

- 9.18 CircleCI

- 9.18.1 Company Overview

- 9.18.2 Key Executives

- 9.18.3 Company snapshot

- 9.18.4 Active Business Divisions

- 9.18.5 Product portfolio

- 9.18.6 Business performance

- 9.18.7 Major Strategic Initiatives and Developments

- 9.19 Octopus Deploy

- 9.19.1 Company Overview

- 9.19.2 Key Executives

- 9.19.3 Company snapshot

- 9.19.4 Active Business Divisions

- 9.19.5 Product portfolio

- 9.19.6 Business performance

- 9.19.7 Major Strategic Initiatives and Developments

- 9.20 Electric Cloud Inc.

- 9.20.1 Company Overview

- 9.20.2 Key Executives

- 9.20.3 Company snapshot

- 9.20.4 Active Business Divisions

- 9.20.5 Product portfolio

- 9.20.6 Business performance

- 9.20.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Application |

|

By Deployment Mode |

|

By Enterprise size |

|

By Component |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the growth rate of Deployment Automation Market?

+

-

What are the latest trends influencing the Deployment Automation Market?

+

-

Who are the key players in the Deployment Automation Market?

+

-

How is the Deployment Automation } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Deployment Automation Market Study?

+

-

What geographic breakdown is available in Global Deployment Automation Market Study?

+

-

Which region holds the second position by market share in the Deployment Automation market?

+

-

How are the key players in the Deployment Automation market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Deployment Automation market?

+

-

What are the major challenges faced by the Deployment Automation Market?

+

-