Global Diesel Exhaust Fluid Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-2167 | Automotive and Transport | Last updated: Dec, 2024 | Formats*:

Diesel Exhaust Fluid Report Highlights

| Report Metrics | Details |

|---|---|

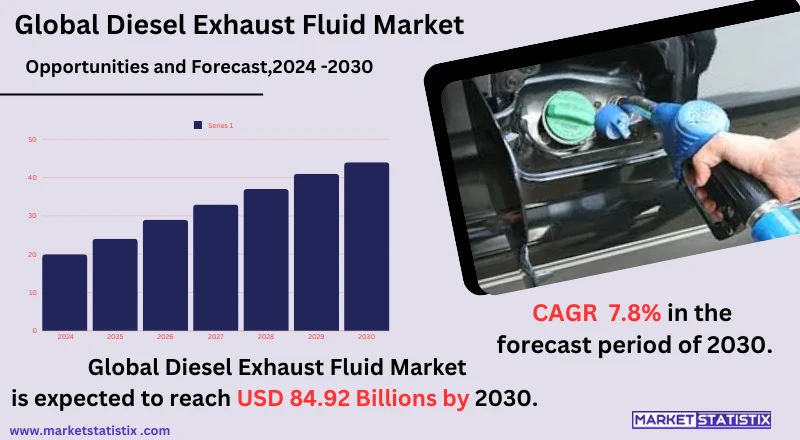

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 7.8% |

| Forecast Value (2030) | USD 84.92 Billion |

| By Product Type | Passenger Cars, LCVs, HCVs |

| Key Market Players |

|

| By Region |

|

Diesel Exhaust Fluid Market Trends

The Diesel Exhaust Fluid (DEF) market is poised to gain momentum as nations across Europe, North America, and Asia tighten environmental emission standards. Besides certain states insisting on tougher NOx emission laws, the DEF market is expected to realize significant increases, particularly from industries using diesel-powered vehicles and machines, for example, those industries involved in transportation, agriculture, and construction. Further, the increase in sustainability and environmental consciousness among consumers and businesses will strengthen the DEF market as well. Manufacturers are improving efficiencies and quality of DEF to give optimum efficiency and longer life to vehicles. The advent of newer modes of distribution, such as retail networks, online platforms, and mobile refuelling services, has also become the market trend, making DEF more available to end-users. The global automotive fleet growth and diesel engine application expansion are expected to further drive demand in the upcoming years. Further, the growing need for regulatory compliance will contribute to and push the DEF industry demand in the coming years.Diesel Exhaust Fluid Market Leading Players

The key players profiled in the report are Borealis AG, Royal Dutch Shell PLC, Mitsui Chemicals INC, Adeco doo, GreenChem, Nissan Chemical Corporation, BP PLC, Diesel Exhaust Fluid (AdBlue) Market Storage Solution Outlook, NOVAX Material & Technology Inc, Diesel Exhaust Fluid (AdBlue) Market Segmentation:, Tanks, Dispensers, Portable Containers, Bulk Storage, BASF SE, Yara, OthersGrowth Accelerators

Tightened environmental regulations are the prime drivers of the diesel exhaust fluid (DEF) market with the prime intention of reducing harmful emissions from diesel engines. Euro 6 and the U.S. EPA's Tier 3 emission standards, for instance, require heavy-duty vehicles to reduce the nitrogen oxide (NOx) emissions, which creates a huge opportunity for demand from DEF. The fluid is known to facilitate the selective catalytic reduction (SCR) process required in a diesel engine for which further compliance is made mandatory through such standards by different sectors such as transportation, agriculture, and logistics. The other factor driving the increase is the growing tendency towards diesel vehicles and ever-increasing global transport. Most importantly, diesel favours the price and efficiency of trucks, heavy-duty vehicles, and machinery, thus increasing the demand for DEF. Also, increasing awareness of the effects of diesel engines on the environment and a trend of using cleaner technologies make the market supportive, where individuals and firms will thereby invest in DEF to maximize internal combustion engine performance while reducing emissions.Diesel Exhaust Fluid Market Segmentation analysis

The Global Diesel Exhaust Fluid is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Passenger Cars, LCVs, HCVs . The Application segment categorizes the market based on its usage such as Automotive, Construction Machinery, Farm Machinery, Electronic Generators, Railway Engines Others. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The diesel exhaust fluid (DEF) market is burgeoning, with nearly hundreds of global and regional players involved in the production, distribution, and retailing of DEF products. Some of the key players in this market are international chemical manufacturers, oil and gas companies, and dedicated DEF producers competing vigorously for market share. These players are focusing on expanding portfolios, improving distribution networks, and partnering strategically to meet increased DEF demand fostered by stricter environmental regulations concerning nitrogen oxide (NOx) emissions from diesel vehicles. Innovation and quality assurance are the key factors of competition in this market. Manufacturers have invested in the development of higher-purity DEF formulations and improvement in supply chain capabilities, primarily since the demand figures rise for North America, Europe, and Asia-Pacific. In addition, the companies grow their business by developing systems for monitoring DEF through digitalization and focusing on sustainability for an increasing market on more eco-friendly products spread into the automotive and industrial sectors.Challenges In Diesel Exhaust Fluid Market

The DEF sector is entangled with an intricate mesh of supply chain constraints and the irrefutable volatile costs attached to the procurement of the raw materials for the manufacture of diesel exhaust fluids. For instance, urea, the basic raw material for the production of diesel exhaust fluids, is known to present raw material price volatility due to various agricultural situations and global supply and demand phenomena. Such uncertainties in the supply chain then give rise to price escalations and possible nonavailability, and both, in return, affect the cost and availability of DEF for end users, such as trucking firms and fleet operators. Moreover, it is placing a strand on the cord that is being held taut by the increasing usage of alternative fuels like electric vehicles (EVs) and hydrogen fuel cell-powered vehicle technologies, which may inhibit diesel-powered vehicles and thus reduce the need for DEF. The market would thus be shaped by these companies evolving and emitting directives, as regulations and emission standards are different between regions and may complicate matters for the end users as well as manufacturers who are trying to keep up with the changing environmental laws. Such pressures from regulatory framework changes may result in a need for constant innovations and changes in formulations and applications of DEF.Risks & Prospects in Diesel Exhaust Fluid Market

The above statement aptly depicts that the Diesel Exhaust Fluid (DEF) market is advancing significantly on the high tides of international regulatory standards for environmental protection. The regulations are becoming more stringent worldwide, especially in Europe, North America, and Asia-Pacific countries. When emissions standards become rigidly stringent, especially for diesel engines, the market will witness great potential for DEF as a major factor in the reduction of nitrogen oxide (NOx) emissions. It also identifies the enhanced adoption of diesel vehicles as well as their further penetration into commercial transport and heavy-duty vehicles as key indicators to usher in demand for DEF. Another important opportunity in DEF is the penetration into the electric and hybrid vehicle markets. DEF can be utilized in these emissions-compliant diesel engines for specific applications. Aspects such as technological progress in DEF injection systems and increased awareness of sustainability and fuel economy open up new possibilities for innovations. There are emerging markets where economic activities are increasing and infrastructure developing; demand for DEF in trucks, construction equipment, and other heavy-duty machinery is already burgeoning. Manufacturers can seize opportunities in such developing markets.Key Target Audience

Fleet operators, trucking companies, and even transportation services are the key potential customers targeted by the Diesel Exhaust Fluid (DEF) market. Such customers are quite motivated for such compliance regarding the emission-restrictive norms framed by various regulating authorities around the world, such as the Environmental Protection Agency (EPA) in the U.S. Therefore, DEF becomes indispensable when reducing nitrogen oxide (NOx) emissions in diesel vehicles equipped with selective catalytic reduction (SCR) systems. DEF thus becomes very essential to most commercial vehicle operators, being able to ensure fleet efficiency while at the same time maintaining regulatory compliance.,, The other emerging groups in the segment include diesel engine manufacturers and automotive OEMs (Original Equipment Manufacturers), who fit SCR systems into their new models of vehicles to meet the environmental standards. More than that, the demand will further extend from the agriculture, construction, and mining sectors, which have a significant reliance on diesel machinery and equipment. These industries will seek this product for business continuity with emission norms as compared to fewer emissions in the environment.Merger and acquisition

The DEF market is on the cusp of merger and acquisition activity, with a round of mergers and acquisitions initiated by major market players in their quest for consolidation and market reach expansion. Out of these, TotalEnergies made its move by acquiring BP's retail network and logistical assets for developing DEF distribution capacity in Mozambique. This strategic acquisition is expected to drive TotalEnergies' product sales of DEF significantly while aligning with the increasing demand as countries release more stringent emission regulations worldwide. Companies like BASF SE and Shell PLC are also focused on pursuing growth through mergers and acquisitions. Mergers are legacy strategies that have characterized the industry's rush for growth as the DEF market burgeons, primarily owing to the increasing application of selective catalytic reduction (SCR) in diesel vehicles. In fact, the DEF market is packed with well-known players such as Yara International and CF Industries that are using acquisitions to enhance their technological capabilities and offerings in their portion of the market. The compliance among regions of stringent emission standards has also ramped up usage of DEF in heavy-duty vehicles, thereby supplementing growth in the market. All these strategic movements go on to paint a picture of a very positive trend toward consolidation in the DEF market as companies strive to respond to emerging demands and regulatory requirements successfully.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Diesel Exhaust Fluid- Snapshot

- 2.2 Diesel Exhaust Fluid- Segment Snapshot

- 2.3 Diesel Exhaust Fluid- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Diesel Exhaust Fluid Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Passenger Cars

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 LCVs

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 HCVs

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Diesel Exhaust Fluid Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Automotive

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Construction Machinery

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Farm Machinery

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Electronic Generators

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Railway Engines Others

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

6: Diesel Exhaust Fluid Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Borealis AG

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Royal Dutch Shell PLC

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Mitsui Chemicals INC

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Adeco doo

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 GreenChem

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Nissan Chemical Corporation

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 BP PLC

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Diesel Exhaust Fluid (AdBlue) Market Storage Solution Outlook

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 NOVAX Material & Technology Inc

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Diesel Exhaust Fluid (AdBlue) Market Segmentation:

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Tanks

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Dispensers

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Portable Containers

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 Bulk Storage

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 BASF SE

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 Yara

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 Others

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Diesel Exhaust Fluid in 2030?

+

-

How big is the Global Diesel Exhaust Fluid market?

+

-

How do regulatory policies impact the Diesel Exhaust Fluid Market?

+

-

What major players in Diesel Exhaust Fluid Market?

+

-

What applications are categorized in the Diesel Exhaust Fluid market study?

+

-

Which product types are examined in the Diesel Exhaust Fluid Market Study?

+

-

Which regions are expected to show the fastest growth in the Diesel Exhaust Fluid market?

+

-

What are the major growth drivers in the Diesel Exhaust Fluid market?

+

-

Is the study period of the Diesel Exhaust Fluid flexible or fixed?

+

-

How do economic factors influence the Diesel Exhaust Fluid market?

+

-