Global Electrolysis Manufacturing Market - Industry Dynamics, Size, And Opportunity Forecast To 2032

Report ID: MS-365 | Chemicals And Materials | Last updated: Feb, 2025 | Formats*:

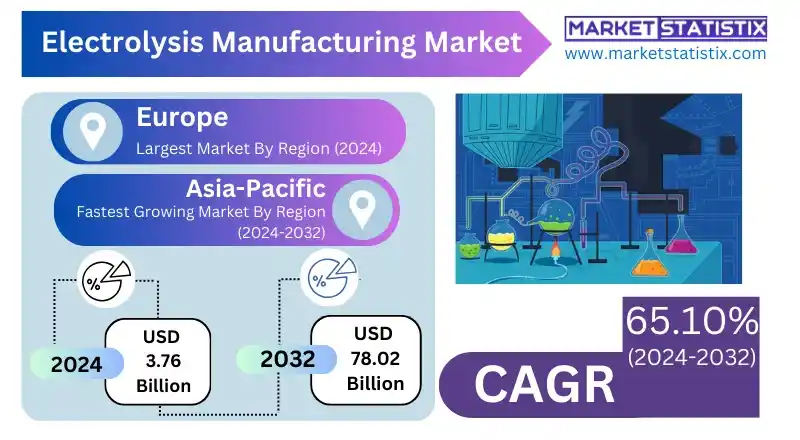

Electrolysers Manufacturing Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2032 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 65.10% |

| Forecast Value (2032) | USD 78.02 Billion |

| By Product Type | Proton Exchange Membrane (PEM) Electrolyzers, Alkaline Electrolyzers, Solid Oxide Electrolyzers |

| Key Market Players |

|

| By Region |

|

Electrolysers Manufacturing Market Trends

The electrolyzer manufacturing sector is undergoing some innovative work with all efforts put into efficiency and cost improvements. Activities include research and development of materials, designs, and manufacturing processes for a wide variety of electrolyzers: alkaline, PEM, and solid oxide. It is further observed that there are huge efforts directed toward developing larger-scale systems that are modular, which will cater to the increasing demand for green hydrogen in industrial applications and for energy storage in the grid. Another identifiable trend is the rising incorporation of electrolyzers with renewable sources of energy such as solar and wind resources. This allows the direct generation of green hydrogen, making this process more sustainable and cheaper to serve as an energy carrier. More and more, electrolyzer manufacturers, renewable energy providers, and end users are entering into partnerships and collaborations that facilitate the advancement of integrated hydrogen solutions, thereby scaling up the commercialization of electrolyzer technology across a range of sectors.Electrolysers Manufacturing Market Leading Players

The key players profiled in the report are Hydrogenics, Cummins Inc., Bloom Energy, Siemens Energy, ITM Power, McPhy Energy, Air Liquide, Nel Hydrogen, Plug Power Inc., Iberdrola S.A., McPhy Energy, Toshiba Corporation, Asahi Kasei, Air Products and Chemicals Inc., ITM PowerGrowth Accelerators

The key market drivers for the electrolyzer manufacturing market lie in the increased demand for green hydrogen, governmental policy, and renewable technologies. Industries chasing decarbonization are more attracted to green hydrogen produced from electrolysis as a clean substitute for fossil fuel. Hydrogen usage in transportation, chemicals, and steel-making industries has gained traction to meet their sustainability goals, hence propelling the demand for electrolyzers. The increase in research and development (R&D) efforts is improving the efficiency, scaling, and durability of electrolyzers, which promotes their commercialization. In addition, collaborations among energy companies, research institutions, and the government foster innovation and broaden production capacity. As such, with global efforts directed toward energy transition, there will be considerable growth potential for the electrolyzer manufacturing market with its stimulus toward clean energy technologies.Electrolysers Manufacturing Market Segmentation analysis

The Global Electrolysers Manufacturing is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Proton Exchange Membrane (PEM) Electrolyzers, Alkaline Electrolyzers, Solid Oxide Electrolyzers . The Application segment categorizes the market based on its usage such as Industrial Gas Production, Green Hydrogen Production, Energy Storage. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The electrolyzer’s manufacturing market has mixed competition between old players and new innovators. Major global companies such as Siemens Energy, Nel Hydrogen, and ITM Power control the market with various electrolyzer types, including the alkaline, PEM, and solid oxide varieties. These players with advanced technologies and large-scale plants manufacture electrolyzers, which find applications in various fields, including hydrogen production, fuel cell technology, and the integration of renewable energy. Their market position is further enhanced by strategic partnerships with energy producers and governments.Challenges In Electrolysers Manufacturing Market

Well, now the market for electrolyzer manufacture has to contend with quite a few challenges. One of the major ones here is production cost. This is primarily driven by expensive materials like platinum and iridium that various electrolyzer types require. This very cost factor makes green hydrogen production less competitive against conventional methods of hydrogen production and thus acts as a deterrent to further adoption. Durability and reliability of the electrolyzer are another challenge. These devices must work effectively and reliably for long periods, sometimes under quite difficult conditions. Technical issues related to material degradation, system integration, and performance optimization must be solved to make large-scale green hydrogen production economically viable. Then there's the supply chain bottleneck for some key components in the market; it also needs some standardized testing and certification mechanisms for quality and safety.Risks & Prospects in Electrolysers Manufacturing Market

The electrolyzer manufacturing market could see significant opportunities due to the impending demand for green hydrogen. The growing necessity for clean hydrogen as a fuel and feedstock is on the rise as governments and industries in every part of the world are actively involved in setting decarbonization targets. This, therefore, presents an ample opportunity for electrolyzer manufacturers to move into mass production and supply cost-competitive options based on the newfound market demand. Manufacturers that invest along these lines can set themselves apart competitively and work towards capturing a larger share of the market. The production of more efficient and cheaper electrolyzers would, on the other hand, speed the adoption of green hydrogen across early and upcoming developing sectors thereby setting in motion a wealth-generating cycle for the electrolyzers manufacturing market.Key Target Audience

The electrolyzers manufacturing market highlights its foremost audiences as industries engaged in hydrogen production through water electrolysis, such as energy, chemicals, and other industrial sectors. Hydrogen-producing companies are the prime consumers since they employ electrolyzers for creating green hydrogen for fuel cells, energy storage solutions, industrial applications, etc. The renewable energy market will be a major user of electrolyzers because of their role in power-to-gas technologies to store surplus renewable energy as hydrogen.,, Automotive manufacturers and other companies involved in fuel cell technology see a growing market for these electrolyzers in the production of hydrogen for fuel cell vehicles. A larger emerging market consists of research organizations and innovators trying to enhance the performance and scaling up of electrolyzer technologies towards general adoption in a low-carbon economy.Merger and acquisition

The electrolyzer manufacturing market has recently witnessed an unprecedented number of mergers and acquisitions, with a view to bolstering hydrogen production technology capabilities. Key transactions involve Plug Power's acquisition of GINER ELX and United Hydrogen, thereby strengthening its PEM electrolyzer segment. Also, Siemens Energy and Air Liquide are planning to jointly develop large-scale PEM electrolyzers, further showcasing strategic partnerships that are creating the lay of the land in this market. On top of that, the recent merger agreement between H2B2 Electrolysis Technologies and RMG Acquisition Corp. indicates what could be the initiation of public investment in electrolyzer technology. It is anticipated that the merger will assist H2B2 to develop in the green hydrogen sector, offering integrated solutions for hydrogen production. The ongoing acquisition activities are strategic for companies intending to innovate and scale their operations in the fast-expanding electrolyzer market, given the ever-increasing demand for clean energy solutions. >Analyst Comment

"There is rapid growth within the electrolyzer manufacturing market due to a growing global demand for green hydrogen. This demand has arisen as an urgency for the decarbonization of transportation, industrial sectors, and power generation. In all parts of the world, governments have started putting forth policies and incentives to boost hydrogen technologies, and this is in turn pulling increased market growth. Key players are focusing on electrolyzer efficiency, cost reduction, and an increased production capacity for coping with the ever-increasing demand. On the other hand, innovations in electrolyzer technologies like AEM electrolyzer stimulate market growth through a balance of cost and performance. The electrolyzers manufacturing market will experience a significant upsurge shortly, thus forming one of the pillars for a hydrogen-based economic transition."- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Electrolysers Manufacturing- Snapshot

- 2.2 Electrolysers Manufacturing- Segment Snapshot

- 2.3 Electrolysers Manufacturing- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Electrolysers Manufacturing Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Alkaline Electrolyzers

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Proton Exchange Membrane (PEM) Electrolyzers

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Solid Oxide Electrolyzers

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Electrolysers Manufacturing Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Green Hydrogen Production

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Industrial Gas Production

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Energy Storage

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Electrolysers Manufacturing Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Toshiba Corporation

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Hydrogenics

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Iberdrola S.A.

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 McPhy Energy

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Air Liquide

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Bloom Energy

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 ITM Power

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Siemens Energy

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Cummins Inc.

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Nel Hydrogen

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Asahi Kasei

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Plug Power Inc.

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Air Products and Chemicals Inc.

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 McPhy Energy

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 ITM Power

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Electrolysers Manufacturing in 2032?

+

-

Which application type is expected to remain the largest segment in the Global Electrolysers Manufacturing market?

+

-

How big is the Global Electrolysers Manufacturing market?

+

-

How do regulatory policies impact the Electrolysers Manufacturing Market?

+

-

What major players in Electrolysers Manufacturing Market?

+

-

What applications are categorized in the Electrolysers Manufacturing market study?

+

-

Which product types are examined in the Electrolysers Manufacturing Market Study?

+

-

Which regions are expected to show the fastest growth in the Electrolysers Manufacturing market?

+

-

Which application holds the second-highest market share in the Electrolysers Manufacturing market?

+

-

Which region is the fastest growing in the Electrolysers Manufacturing market?

+

-