Global Electronic Toll Collection Market - Industry Dynamics, Size, And Opportunity Forecast To 2032

Report ID: MS-2395 | Electronics and Semiconductors | Last updated: Jan, 2025 | Formats*:

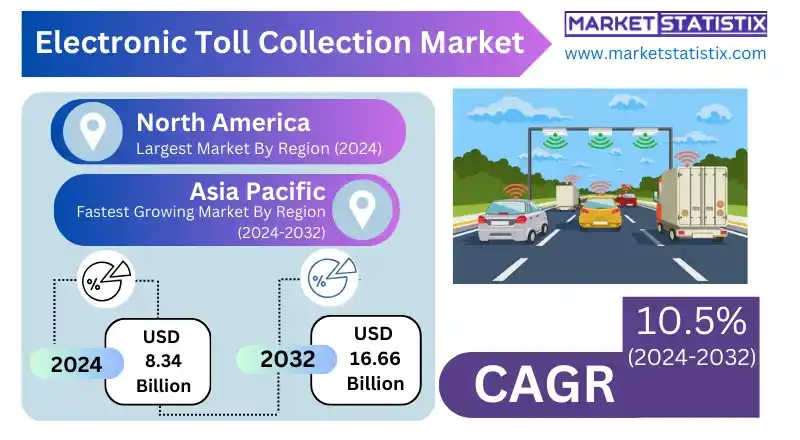

Electronic Toll Collection Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2032 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 10.5% |

| Forecast Value (2032) | USD 16.66 Billion |

| By Product Type | Violation Enforcement System (VES), Automatic Vehicle Classification (AVC), Automatic Vehicle Identification System (AVIS), Others (Transaction Processing/Back Office) |

| Key Market Players |

|

| By Region |

|

Electronic Toll Collection Market Trends

The Electronic Toll Collection (ETC) market is currently undergoing some important trends. Where a major trend is the rise in free-flow multi-lane systems enabling vehicles to pass under toll gates without stopping, this in turn provides improved traffic flow and reduced congestion. Another important trend is the connection between ETC systems and other intelligent transportation systems (ITS), including traffic control systems and incident detection systems. With this integration, more effective traffic control can be achieved and road safety can be enhanced. Moreover, the market is also affected by the emergence of the smart city trend and the sustainable mobility trend in the world. Electronic tolling solutions are being funded by governments and transportation authorities as one of the ways to improve road utilization, limit carbon emissions, and encourage environmentally friendly modes of transport.Electronic Toll Collection Market Leading Players

The key players profiled in the report are Honeywell International Inc. (U.S.), Kapsch TrafficCom AG (Austria), Mitsubishi Heavy Industries Ltd. (Japan), EFKON (Austria), Q-Free (Norway), TRMI Systems Integration (Japan), Perceptics (U.S.), IRD (Canada), Transcore Holdings Inc. (U.S.), Thales Group (U.S.)Growth Accelerators

The electronic toll collection (ETC) market is mainly guided by the increase of the need for a more effective and noncontact solution for tolling that, on the one side, can help alleviate traffic congestion and, on the other side, make the operation more efficient. Due to growing urbanization and vehicle counts, conventional tolling mechanisms are no longer sufficient, and governments and transport authorities are switching over to ETC systems for efficient and quick toll collection. These systems minimize the number of manual cash transactions, enhance traffic flow, and diminish operational costs, which makes them very appealing for public infrastructure works. A significant factor is the increasing focus on smart transportation systems and better road safety and environmental sustainability. ETC solutions facilitate integration with next-generation technologies, including GPS, RFID, and cloud computing, allowing real-time data acquisition and more enhanced routing management. Moreover, the momentum of carbon footprint reduction by traffic flow decoupling and vehicular idle time reduction deters ETC implementation. Governments also consider ETC as a means to improve toll revenue collection accuracy and enable future developments of autonomous and interconnected vehicles.Electronic Toll Collection Market Segmentation analysis

The Global Electronic Toll Collection is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Violation Enforcement System (VES), Automatic Vehicle Classification (AVC), Automatic Vehicle Identification System (AVIS), Others (Transaction Processing/Back Office) . The Application segment categorizes the market based on its usage such as Highway, Urban Area. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The electronic toll collection (ETC) market competitive landscape is composed of a combination of traditional and new players providing innovative solutions. Main actors are international players in the field, like Kapsch TrafficCom, TransCore, and Siemens, who hold the major part of the market by providing complete end-to-end ETC systems, including hardware (e.g., RFID tags, sensors, gantries) and software for toll control. These companies are competing on the strength of technological innovation, system integration, and the robustness of their tolling solutions as a highway or urban road network operator. Competition is also increased by the growth in using smart city efforts and adopting interoperable tolling systems throughout the regions, which entails substantial investment in research and development, keeping abreast of the market.Challenges In Electronic Toll Collection Market

High initial infrastructure cost is one of the main market challenges of the electronic toll collection (ETC) market. The deployment of ETC systems involves a substantial investment in hardware, software, and on-ground infrastructure, such as roadways, toll booths, and vehicles. This may represent a bottleneck for governments and private industry, especially in areas where the finances are constrained or there is a reluctance to use new technologies. Another challenge is data security and privacy concerns. Since ETC (electronic toll collection) systems store private information like vehicle identification, trajectory, and payment information, they are vulnerable to cyberattacks, e.g. However, ensuring that these systems can resist unauthorized access (the risk of a security breach) and adhere to data protection legislation is paramount. In addition, there is the task of gaining public acceptance, since some drivers are not willing to implement ETC due to the privacy concerns or surveillance thinking; thus, the stakeholders need to cultivate trust and address the advantage of the system.Risks & Prospects in Electronic Toll Collection Market

The ETC market presents several significant opportunities. Integration of ETC systems with other intelligent transportation/mobility technologies like intelligent transportation systems (ITS) and connected/autonomous vehicles is a prime focus. This integration can also be used to improve and in real-time control of traffic flow, optimize traffic, and hence transportation efficiency in general. An additional point of opportunity is in the design and deployment of advanced ETC technologies, e.g., high-technology video tolling and artificial intelligence (AI) for fraud detection and traffic management. These developments can also more accurately and efficiently execute toll collection while improving the user experience.Key Target Audience

The main user group of the electronic toll collection (ETC) market segment are transportation authorities, government entities, and municipality bodies in charge of monitoring toll roadways, bridges, and tunnels. These entities use ETC systems in order to optimize toll collection processes, decrease traffic congestion, and enhance revenue collection efficiency. Specifically, they propose to improve traffic flow, reduce human error, and offer drivers a smoother experience while guaranteeing transparency in toll prices through the deployment of automated systems.,, A secondary target of the audience is the logistics, transportation, and automotive businesses, including fleet operators and commercial vehicle fleet owners. These firms are assisted by ETC-based solutions through the utilization of real-time toll data, improved route planning, and the compression of administrative labor associated with manual toll collection.Merger and acquisition

Recent mergers and acquisitions in the electronic toll collection (ETC) market have focused not only on the need for technology but also on the need for service offerings. At the end of 2024, Kapsch TrafficCom AG revealed the buyout of TransCore Holdings Inc., a major step towards creating one giant market player in the North American segment. This acquisition is expected to combine Kapsch's advanced tolling technologies with TransCore's extensive experience in transportation solutions, thereby enhancing their capabilities in providing integrated electronic tolling systems. Moreover, Thales Group has also participated in the ETC field (acquisition of EFKON GmbH*, an Austrian company specializing in innovative tolling solutions). This acquisition, closed in January 2025, is intended to bring to the table EFKON's particular expertise in next-generation technologies in order to complement Thales's current offering for smart transportation systems. These strategic mergers are a reflection of a broader trend towards developing integrated solutions able to effectively administer traffic flow and optimize toll collection systems. >Analyst Comment

"The electronic toll collection (ETC) market is experiencing significant growth, driven by the increasing need for efficient and convenient transportation systems. ETC systems employ a range of technologies (e.g., RFID and license plate reading) to automate toll collection, hence alleviating traffic congestion and improving journey times. Main drivers of the market are governmental policy aimed at upgrading transport infrastructure, rising demand for cashless payment, and rising use of smart vehicles. ETC market is predicted to continue its growth over the coming years thanks to the improvement and the more and more general application of ETC systems with other smart city technologies."- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Electronic Toll Collection- Snapshot

- 2.2 Electronic Toll Collection- Segment Snapshot

- 2.3 Electronic Toll Collection- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Electronic Toll Collection Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Automatic Vehicle Classification (AVC)

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Violation Enforcement System (VES)

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Automatic Vehicle Identification System (AVIS)

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Others (Transaction Processing/Back Office)

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

5: Electronic Toll Collection Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Highway

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Urban Area

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

6: Electronic Toll Collection Market by Technology

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Radio Frequency Identification (RFID)

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Dedicated Short Range Communication (DSRC)

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Global Navigation Satellite System (GNSS)/GPS

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Video Analytics

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

- 6.6 Cell Phone Tolling

- 6.6.1 Key market trends, factors driving growth, and opportunities

- 6.6.2 Market size and forecast, by region

- 6.6.3 Market share analysis by country

- 6.7 Others (Barcode-based ETC)

- 6.7.1 Key market trends, factors driving growth, and opportunities

- 6.7.2 Market size and forecast, by region

- 6.7.3 Market share analysis by country

7: Electronic Toll Collection Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 Honeywell International Inc. (U.S.)

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Kapsch TrafficCom AG (Austria)

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 IRD (Canada)

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 Mitsubishi Heavy Industries Ltd. (Japan)

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Q-Free (Norway)

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 Transcore Holdings Inc. (U.S.)

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 TRMI Systems Integration (Japan)

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 Perceptics (U.S.)

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 EFKON (Austria)

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 Thales Group (U.S.)

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Technology |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Electronic Toll Collection in 2032?

+

-

Which application type is expected to remain the largest segment in the Global Electronic Toll Collection market?

+

-

How big is the Global Electronic Toll Collection market?

+

-

How do regulatory policies impact the Electronic Toll Collection Market?

+

-

What major players in Electronic Toll Collection Market?

+

-

What applications are categorized in the Electronic Toll Collection market study?

+

-

Which product types are examined in the Electronic Toll Collection Market Study?

+

-

Which regions are expected to show the fastest growth in the Electronic Toll Collection market?

+

-

Which application holds the second-highest market share in the Electronic Toll Collection market?

+

-

Which region is the fastest growing in the Electronic Toll Collection market?

+

-