Global Flanges Market Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-2534 | Machinery and Equipment | Last updated: Feb, 2025 | Formats*:

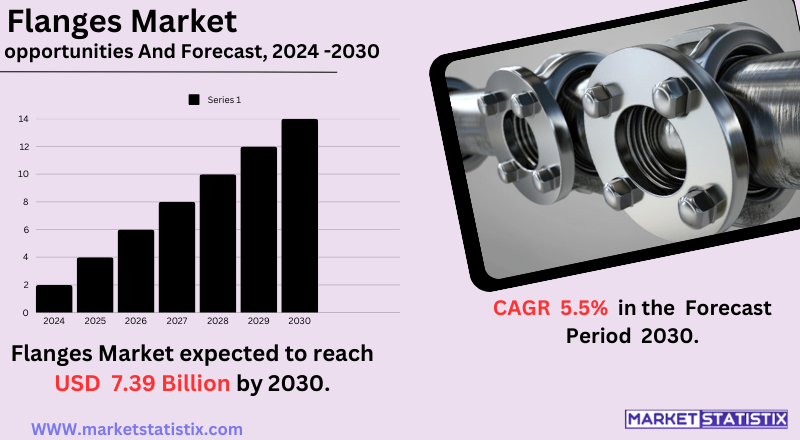

Flanges Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 5.5% |

| Forecast Value (2030) | USD 7.39 Billion |

| By Product Type | Weld Neck Flanges, Blind Flanges, Slip-On Flanges, Socket Weld Flanges, Threaded Flanges |

| Key Market Players |

|

| By Region |

|

Flanges Market Trends

In addition, there is a very popular trend now in the flange market, which is the acceptance of lightweight materials such as composites and advanced alloys. The driving factors include better performance and lighter weight for improved corrosion resistance. These have been included as prerequisites for industries such as aerospace and automotive, where weight optimisation is paramount. Lately, increasing attention to sustainability is also running among manufacturers in selecting greener materials and processes. Another main trend is that flange manufacturing increasingly adopts automation and features smart technologies, such as robotics, AI, digital twins, etc., in its production processes. These technological advancements are optimising the production process together with the complexities of customer-required flange solutions.Flanges Market Leading Players

The key players profiled in the report are Metalfar S.p.A., Simtech Process Systems, Kerkau Manufacturing, Star Pipe Products, Ltd., Pro-Flange, OCoastal Flange Inc, Hitachi, Texas Flange, Holdings, Inc., Kohler Corporation, Maass Global Group, SSI Technologies, Inc., Flanschenwerk Bebitz GmbH, Piping Technology & Products, Inc., utokumpu Armetal Stainless Pipe Co Ltd.Growth Accelerators

Continual expansion of primary end-use industries, such as oil and gas, chemical processing, and water treatment, has constantly driven the flanges market. All these sectors are heavily relying on strong piping systems in connecting and maintaining these systems to create a regular market for flanges. In addition, increased investment in infrastructure development and new pipelines and industrial facilities, especially in developing economies, further adds oil to the fire in demand for flanges. This includes increased growth of safety focus for the industry and the prevention of leaks. Establishing high-quality flanges is critical to ensuring the integrity of piping systems and minimising possible accidents. With such safety precautions and strict regulations, the industries are compelled to accept advanced flange technologies and materials, thus driving up the market.Flanges Market Segmentation analysis

The Global Flanges is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Weld Neck Flanges, Blind Flanges, Slip-On Flanges, Socket Weld Flanges, Threaded Flanges . The Application segment categorizes the market based on its usage such as Oil & Gas, Chemical Industry, Wastewater Management, Power Generation, Petrochemical, Others. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The flanges sector consists of a mixture of well-established global firms and some smaller manufacturers for regional markets. Factors that affect competition include quality of goods, price, reliability in delivery, and technological innovation. Leading companies tend to use differentiators such as specialised types of flanges, customised solutions, and superior materials that meet the needs presented by a given industrial sector. There is also an increasing trend toward consolidation in the flanges market by means of mergers and acquisitions, as companies try to consolidate and broaden their product ranges, geographic reach, and production capacities. In addition to these factors, the competitive landscape has also been shaped by other variables such as availability of raw materials, labour costs, government regulations, and so on. Nowadays, most companies are focusing on sustainable manufacturing processes and designing green flanges to comply with the latest environmental regulations. To succeed in this highly competitive market, the ability to respond dynamically to changes in market patterns, to carry out research and development, and to cultivate strong relationships with customers is imperative.Challenges In Flanges Market

In between the challenges, the ever-fluctuating prices of raw materials, especially steel and alloys, simply reflect how production costs and profits/returns are influenced for the flanges market. Loose ends in the supply chain mark such things as transportation delays and geopolitical tensions that only worsen raw material availability for projects. The rising demand for customised and high-performance flanges in sectors such as oil & gas, petrochemicals, power generation, and others is an additional challenge because it requires very advanced manufacturing capability. Another big challenge for the market is increased competition from low-cost alternatives, welded connections that can substitute the traditional flanges quite cheaply. Also, another challenge for companies in this case may be the incorporation of new-age technology for the purposes of going digital and for automation due to the lack of infrastructure or expertise.Risks & Prospects in Flanges Market

The flanges market presents enormous opportunities because of the concurrent demand increase in the oil industry, gas industry, petrochemicals, water-waste-water treatment, and power generation businesses. With the rise in infrastructure development and pace of industrialisation in developing markets, the flanges industry is pushed further toward growth. Newer material advancements to stainless steel and alloy-based flanges increasing their durability and performance are also positively influencing demand. Regionally, The Asia-Pacific region covers the maximum share of the flanges market attributable to rapidly growing industries, urbanisation, and high investments in energy and infrastructural development projects, especially in China and India. North America is the next in line owing to the shale gas exploration and offshore drilling activities in this region. In Europe, market trends are being influenced by the stringent rules promoting sustainable construction and safety standards in pipeline activities. Whereas the Middle East and Africa have remained strategic players due to ongoing large-scale operations in oil and gas and the gradual growth of Latin America, with increasing endeavours for infrastructure and industrialisation projects.Key Target Audience

, The flanges market serves multiple industries that consider fluid transfer systems as their core business. Hence, customers include oil and gas companies that demand flanges for pipelines, refinery works, and offshore platforms. Chemical processing plants represent another important segment that heavily utilises flanges in transporting corrosive and hazardous materials., Apart from such industries, flanges are also used in power generation, water and wastewater treatment, aerospace, and even food and beverage processing. Within each of these industries, the various segments can also include engineers who will design and maintain piping systems, procurement managers who will source the components, and maintenance operators in charge of installation and repairs.Merger and acquisition

The flanges market has been recently undergoing significant rounds of M&A activity that reflect the general trends within the industrial sector. The merger between ExxonMobil and Pioneer, valued at $60 billion, was consummated in May of 2024, the biggest oil-and-gas acquisition in the last 20 years. This acquisition will enhance ExxonMobil's production activities in the Permian Basin, wherein production could ramp up to 2 million barrels a day by 2027. Chevron's acquisition of Hess Corporation for $53 billion strengthened Chevron's portfolio and hastened production growth, reflecting a growing trend in consolidation in the energy sector that will also weigh on flange manufacturing as demand for industrial components increases. These major acquisitions also speak about the desire for technology valorisation in industrial applications. Cisco's acquisition of Splunk worth $28 billion broadly speaks to this. Enhanced security and observability solutions are expected to be delivered for different sectors, including those depending on flanges and piping systems. >Analyst Comment

The flanges market is on a steady growth path as key industries such as oil and gas, chemical processing, and power generation expand. These industries rely on piping systems, warranting steady demand for flanges to provide safe and secure connections. Further, investments in infrastructure and water management projects will also facilitate growth in the market. Innovation and product development characterize the market, with manufacturers inclined toward improving the performance, durability, and corrosion proof of their flanges. New materials and manufacturing processes are being introduced for meeting the ever-changing demands of diverse industries.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Flanges- Snapshot

- 2.2 Flanges- Segment Snapshot

- 2.3 Flanges- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Flanges Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Weld Neck Flanges

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Slip-On Flanges

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Blind Flanges

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Socket Weld Flanges

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Threaded Flanges

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

5: Flanges Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Oil & Gas

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Petrochemical

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Power Generation

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Wastewater Management

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Chemical Industry

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

- 5.7 Others

- 5.7.1 Key market trends, factors driving growth, and opportunities

- 5.7.2 Market size and forecast, by region

- 5.7.3 Market share analysis by country

6: Flanges Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Flanschenwerk Bebitz GmbH

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Hitachi

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Holdings

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Inc.

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Kerkau Manufacturing

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Kohler Corporation

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Maass Global Group

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Metalfar S.p.A.

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 OCoastal Flange Inc

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Piping Technology & Products

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Inc.

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Pro-Flange

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Simtech Process Systems

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 SSI Technologies

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Inc.

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 Star Pipe Products

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 Ltd.

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

- 8.18 Texas Flange

- 8.18.1 Company Overview

- 8.18.2 Key Executives

- 8.18.3 Company snapshot

- 8.18.4 Active Business Divisions

- 8.18.5 Product portfolio

- 8.18.6 Business performance

- 8.18.7 Major Strategic Initiatives and Developments

- 8.19 utokumpu Armetal Stainless Pipe Co Ltd.

- 8.19.1 Company Overview

- 8.19.2 Key Executives

- 8.19.3 Company snapshot

- 8.19.4 Active Business Divisions

- 8.19.5 Product portfolio

- 8.19.6 Business performance

- 8.19.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Flanges in 2030?

+

-

Which type of Flanges is widely popular?

+

-

What is the growth rate of Flanges Market?

+

-

What are the latest trends influencing the Flanges Market?

+

-

Who are the key players in the Flanges Market?

+

-

How is the Flanges } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Flanges Market Study?

+

-

What geographic breakdown is available in Global Flanges Market Study?

+

-

Which region holds the second position by market share in the Flanges market?

+

-

How are the key players in the Flanges market targeting growth in the future?

+

-