Global Histoplasmosis Treatment Market – Industry Trends and Forecast to 2032

Report ID: MS-2505 | Healthcare and Pharma | Last updated: Feb, 2025 | Formats*:

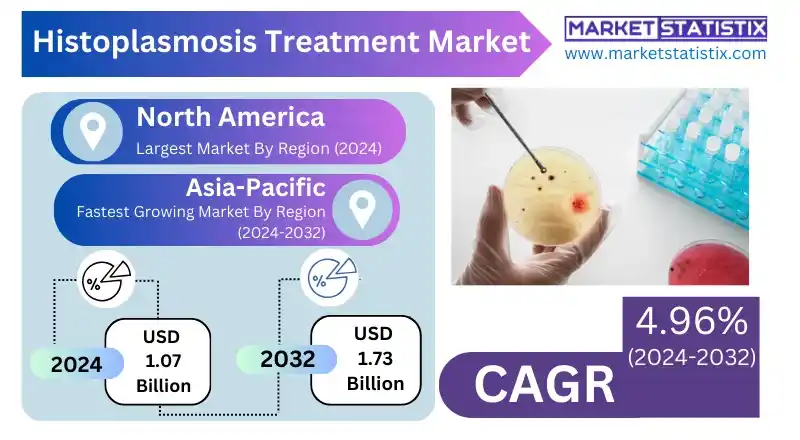

Histoplasmosis Treatment Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2032 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 4.96% |

| Forecast Value (2032) | USD 1.73 Billion |

| Key Market Players |

|

| By Region |

|

Histoplasmosis Treatment Market Trends

The histoplasmosis treatment market is expected to grow on changes regarding the increasing incidences across regions worldwide and focus on developing new antifungal agents for treatment. This does include the ongoing effort to formulate new drug formulations and some targeted medications for reducing the period of treatment and adverse effects associated with administration. Moreover, advancements in the diagnostic methods are also aiding in the early detection and better management of the disease, further adding to the demand in the relevant market. Conventional trends in the current setting are such as the management of antifungal resistance, combination therapy, immunomodulatory therapy, and advanced diagnosis technologies. They also amplify the part of patient education and support programs with telemedicine and distance talks in serving patients' care improvement. Such initiatives combined with growing awareness and better access to health care would have a positive impact on the further growth of the market for histoplasmosis treatment.Histoplasmosis Treatment Market Leading Players

The key players profiled in the report are Amgen, GlaxoSmithKline, Eli Lilly, Johnson and Johnson, Gilead Sciences, AstraZeneca, AbbVie, Novartis, Teva Pharmaceuticals, Sanofi, BristolMyers Squibb, Pfizer, Merck and Co, Baxter International, RocheGrowth Accelerators

The growth of the market for histoplasmosis treatment is propelled by heightened incidence of histoplasmosis, particularly in some occupational groups such as construction work and poultry farming, and among those who are immunosuppressed. The increasing prevalence of human immunodeficiency virus (HIV) is boosting market growth since the treatment of histoplasmosis in AIDS patients is required to control fungal infection and lower mortality. Another factor likely to flourish in this market is the increasing incidences of chronic disorders, which severely compromise the immune response of the human body. Other factors pushing this market include increased research and development, technological innovations, and the developed healthcare system in regions like North America. Major companies are now introducing many novel treatments, notably advanced formulations of Itraconazole for the effective management of fungal infections. Currently, there is governmental emphasis on infectious diseases and healthcare management primarily in the Asia-Pacific area, and this is favourably contributing to the growing need for advanced diagnostics and therapies for histoplasmosis.Histoplasmosis Treatment Market Segmentation analysis

The Global Histoplasmosis Treatment is segmented by Application, and Region. . The Application segment categorizes the market based on its usage such as Clinics, Hospitals, Home Healthcare. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

Competitiveness has become important for the histoplasmosis treatment market, which sees its software from key pharmaceutical companies and healthcare providers focusing primarily on antifungal therapies. Pfizer, Merck & Co., Astellas Pharma, and Gilead Sciences dominate the market, having a strong antiform scale, including drugs like itraconazole and amphotericin B. The competition is driven primarily by the advancement of skills in drug formulations, the development of new antifungal chemicals, and the growing awareness relating to fungal infections in patients, especially among the immunocompromised ones. They will also have some influence on innovation in biotechnology companies and research institutions developing new treatment and diagnostic approaches for early detection of disease. Competitive position, however, will be very dependent on regulatory approvals, pricing strategies, and access to antifungal treatment in emerging markets.Challenges In Histoplasmosis Treatment Market

The histoplasmosis treatment market is impeded by different challenges. One key challenge is that the diagnosis of the infection in its early days is hard. Histoplasmosis begins with a slew of non-specific symptoms that can mimic other respiratory maladies; as such, misdiagnosis leads to a consequential delay in treatment. Delay in treatment can allow the disease to progress and culminate in complications, especially among the vulnerable populations, such as the immunocompromised. Another challenge with a potential impact on histoplasmosis treatment is that there is a very limited number of antifungal agents with good activity against this infection and that these agents might often be unavailable in resource-restricted places. Some of the classic antifungal medications can have serious side effects; drug resistance is emerging as an additional challenge.Risks & Prospects in Histoplasmosis Treatment Market

Such great opportunities to enter this histoplasmosis treatment market lie ahead. The first one would be general, as it would be histoplasmosis among infected and immunocompromised areas, which would push for the need for treatment. This is an entry point for pharmaceutical companies to invest in drug development and marketing by way of introducing novel antifungal agents having improved efficacy and reduced side effects. Moreover, the increasing awareness of histoplasmosis among healthcare professionals and the public spurs timely diagnosis and intervention, further resulting in growth in the market. In addition, the growing combination therapy use, which combines multiple antifungal agents to treat the infection, is opening up avenues for research and development in the histoplasmosis market. Companies willing to invest in these areas will emerge at the forefront and will be pacesetters in better management of this fungal infection.Key Target Audience

The primary target audience for the histoplasmosis treatment market consists of healthcare professionals, including physicians (especially pulmonologists and those who specialise in infectious diseases), pharmacists, and other medical personnel concerned with the diagnosis and treatment of fungal infections. These professionals are involved in the identification of histoplasmosis, prescription of antifungal medication, and monitoring of the patient. Their professional decisions regarding patient management are based on information regarding available treatment options, efficacy, safety profile, and cost-effectiveness.,, Beyond healthcare professionals, the target audience spans to include patients undergoing treatment for histoplasmosis and their careers. Patients must obtain information about the disease itself, its treatment options, possible side effects, and long-term management. In concert with the other parties, specifically patient groups and support organizations, information dissemination and awareness initiatives promote indirect marketing efforts, empowering patients to seek timely and appropriate treatment.Merger and acquisition

Merger and acquisition activity in the histoplasmosis treatment market has occurred primarily among companies interested in either broadening their portfolios or strengthening their market position. For example, in March 2024, Switzerland-based Sandoz Group AG has acquired the CIMERLI business from Coherus for an undisclosed amount. This acquisition was made to strengthen Sandoz's ophthalmic portfolio with CIMERLI and provide leadership in the U.S. biosimilar market with an expansion of access to affordable treatments for vision impairment. Coherus BioSciences Inc. is a U.S.-based biotech company specialising in treating histoplasmosis. On a broader scale, extensive M&A activity is occurring within the pharma arena that would indirectly impact the histoplasmosis treatment market through the expansion of portfolios and strategic realignment. Novartis will acquire MorphoSys AG to strengthen its oncology pipeline . AstraZeneca has acquired Fusion Pharmaceuticals to strengthen its oncology segment. Sanofi has announced that it intends to acquire Inhibrx, Inc., to strengthen its drug development portfolio. Johnson & Johnson will acquire Ambrx Biopharma Inc., a biotech firm focused on tumour-targeting antibodies. >Analyst Comment

The histoplasmosis therapies market is thriving with the rise in incidence of the disease in certain occupational groups and among those with weakened immune systems. The global histoplasmosis treatment market was valued at USD 4.88 billion in 2024 and is expected to reach USD 12.65 billion by 2037. This growth is attributed to awareness, market opportunities for better diagnostic methods, new antifungal drugs, and therapies. Market drivers include the high prevalence of histoplasmosis found in specific geographic areas, mainly the Americas, Africa, and Asia, and an increasing level of awareness among the treating professionals, which aids with diagnosis and hence treats much earlier and with efficacy. North America remains the key area in the market, having the best healthcare system with specialised treatment programs. Meanwhile, Asia Pacific would be the one region poised to grow rapidly due to urbanisation and an increase in healthcare spending.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Histoplasmosis Treatment- Snapshot

- 2.2 Histoplasmosis Treatment- Segment Snapshot

- 2.3 Histoplasmosis Treatment- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Histoplasmosis Treatment Market by Application / by End Use

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Hospitals

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Clinics

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Home Healthcare

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Histoplasmosis Treatment Market by Drug Type

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Azoles

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Polyene Antifungals

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Echinocandins

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Corticosteroids

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

6: Histoplasmosis Treatment Market by Route of Administration

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Oral

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Intravenous

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Topical

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

7: Histoplasmosis Treatment Market by Disease Severity

- 7.1 Overview

- 7.1.1 Market size and forecast

- 7.2 Acute Histoplasmosis

- 7.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.2 Market size and forecast, by region

- 7.2.3 Market share analysis by country

- 7.3 Chronic Histoplasmosis

- 7.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.2 Market size and forecast, by region

- 7.3.3 Market share analysis by country

- 7.4 Disseminated Histoplasmosis

- 7.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.2 Market size and forecast, by region

- 7.4.3 Market share analysis by country

8: Histoplasmosis Treatment Market by Region

- 8.1 Overview

- 8.1.1 Market size and forecast By Region

- 8.2 North America

- 8.2.1 Key trends and opportunities

- 8.2.2 Market size and forecast, by Type

- 8.2.3 Market size and forecast, by Application

- 8.2.4 Market size and forecast, by country

- 8.2.4.1 United States

- 8.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.1.2 Market size and forecast, by Type

- 8.2.4.1.3 Market size and forecast, by Application

- 8.2.4.2 Canada

- 8.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.2.2 Market size and forecast, by Type

- 8.2.4.2.3 Market size and forecast, by Application

- 8.2.4.3 Mexico

- 8.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.3.2 Market size and forecast, by Type

- 8.2.4.3.3 Market size and forecast, by Application

- 8.2.4.1 United States

- 8.3 South America

- 8.3.1 Key trends and opportunities

- 8.3.2 Market size and forecast, by Type

- 8.3.3 Market size and forecast, by Application

- 8.3.4 Market size and forecast, by country

- 8.3.4.1 Brazil

- 8.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.1.2 Market size and forecast, by Type

- 8.3.4.1.3 Market size and forecast, by Application

- 8.3.4.2 Argentina

- 8.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.2.2 Market size and forecast, by Type

- 8.3.4.2.3 Market size and forecast, by Application

- 8.3.4.3 Chile

- 8.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.3.2 Market size and forecast, by Type

- 8.3.4.3.3 Market size and forecast, by Application

- 8.3.4.4 Rest of South America

- 8.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.4.2 Market size and forecast, by Type

- 8.3.4.4.3 Market size and forecast, by Application

- 8.3.4.1 Brazil

- 8.4 Europe

- 8.4.1 Key trends and opportunities

- 8.4.2 Market size and forecast, by Type

- 8.4.3 Market size and forecast, by Application

- 8.4.4 Market size and forecast, by country

- 8.4.4.1 Germany

- 8.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.1.2 Market size and forecast, by Type

- 8.4.4.1.3 Market size and forecast, by Application

- 8.4.4.2 France

- 8.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.2.2 Market size and forecast, by Type

- 8.4.4.2.3 Market size and forecast, by Application

- 8.4.4.3 Italy

- 8.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.3.2 Market size and forecast, by Type

- 8.4.4.3.3 Market size and forecast, by Application

- 8.4.4.4 United Kingdom

- 8.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.4.2 Market size and forecast, by Type

- 8.4.4.4.3 Market size and forecast, by Application

- 8.4.4.5 Benelux

- 8.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.5.2 Market size and forecast, by Type

- 8.4.4.5.3 Market size and forecast, by Application

- 8.4.4.6 Nordics

- 8.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.6.2 Market size and forecast, by Type

- 8.4.4.6.3 Market size and forecast, by Application

- 8.4.4.7 Rest of Europe

- 8.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.7.2 Market size and forecast, by Type

- 8.4.4.7.3 Market size and forecast, by Application

- 8.4.4.1 Germany

- 8.5 Asia Pacific

- 8.5.1 Key trends and opportunities

- 8.5.2 Market size and forecast, by Type

- 8.5.3 Market size and forecast, by Application

- 8.5.4 Market size and forecast, by country

- 8.5.4.1 China

- 8.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.1.2 Market size and forecast, by Type

- 8.5.4.1.3 Market size and forecast, by Application

- 8.5.4.2 Japan

- 8.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.2.2 Market size and forecast, by Type

- 8.5.4.2.3 Market size and forecast, by Application

- 8.5.4.3 India

- 8.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.3.2 Market size and forecast, by Type

- 8.5.4.3.3 Market size and forecast, by Application

- 8.5.4.4 South Korea

- 8.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.4.2 Market size and forecast, by Type

- 8.5.4.4.3 Market size and forecast, by Application

- 8.5.4.5 Australia

- 8.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.5.2 Market size and forecast, by Type

- 8.5.4.5.3 Market size and forecast, by Application

- 8.5.4.6 Southeast Asia

- 8.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.6.2 Market size and forecast, by Type

- 8.5.4.6.3 Market size and forecast, by Application

- 8.5.4.7 Rest of Asia-Pacific

- 8.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.7.2 Market size and forecast, by Type

- 8.5.4.7.3 Market size and forecast, by Application

- 8.5.4.1 China

- 8.6 MEA

- 8.6.1 Key trends and opportunities

- 8.6.2 Market size and forecast, by Type

- 8.6.3 Market size and forecast, by Application

- 8.6.4 Market size and forecast, by country

- 8.6.4.1 Middle East

- 8.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.6.4.1.2 Market size and forecast, by Type

- 8.6.4.1.3 Market size and forecast, by Application

- 8.6.4.2 Africa

- 8.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.6.4.2.2 Market size and forecast, by Type

- 8.6.4.2.3 Market size and forecast, by Application

- 8.6.4.1 Middle East

- 9.1 Overview

- 9.2 Key Winning Strategies

- 9.3 Top 10 Players: Product Mapping

- 9.4 Competitive Analysis Dashboard

- 9.5 Market Competition Heatmap

- 9.6 Leading Player Positions, 2022

10: Company Profiles

- 10.1 Novartis

- 10.1.1 Company Overview

- 10.1.2 Key Executives

- 10.1.3 Company snapshot

- 10.1.4 Active Business Divisions

- 10.1.5 Product portfolio

- 10.1.6 Business performance

- 10.1.7 Major Strategic Initiatives and Developments

- 10.2 Baxter International

- 10.2.1 Company Overview

- 10.2.2 Key Executives

- 10.2.3 Company snapshot

- 10.2.4 Active Business Divisions

- 10.2.5 Product portfolio

- 10.2.6 Business performance

- 10.2.7 Major Strategic Initiatives and Developments

- 10.3 Johnson and Johnson

- 10.3.1 Company Overview

- 10.3.2 Key Executives

- 10.3.3 Company snapshot

- 10.3.4 Active Business Divisions

- 10.3.5 Product portfolio

- 10.3.6 Business performance

- 10.3.7 Major Strategic Initiatives and Developments

- 10.4 Teva Pharmaceuticals

- 10.4.1 Company Overview

- 10.4.2 Key Executives

- 10.4.3 Company snapshot

- 10.4.4 Active Business Divisions

- 10.4.5 Product portfolio

- 10.4.6 Business performance

- 10.4.7 Major Strategic Initiatives and Developments

- 10.5 GlaxoSmithKline

- 10.5.1 Company Overview

- 10.5.2 Key Executives

- 10.5.3 Company snapshot

- 10.5.4 Active Business Divisions

- 10.5.5 Product portfolio

- 10.5.6 Business performance

- 10.5.7 Major Strategic Initiatives and Developments

- 10.6 Eli Lilly

- 10.6.1 Company Overview

- 10.6.2 Key Executives

- 10.6.3 Company snapshot

- 10.6.4 Active Business Divisions

- 10.6.5 Product portfolio

- 10.6.6 Business performance

- 10.6.7 Major Strategic Initiatives and Developments

- 10.7 Amgen

- 10.7.1 Company Overview

- 10.7.2 Key Executives

- 10.7.3 Company snapshot

- 10.7.4 Active Business Divisions

- 10.7.5 Product portfolio

- 10.7.6 Business performance

- 10.7.7 Major Strategic Initiatives and Developments

- 10.8 Merck and Co

- 10.8.1 Company Overview

- 10.8.2 Key Executives

- 10.8.3 Company snapshot

- 10.8.4 Active Business Divisions

- 10.8.5 Product portfolio

- 10.8.6 Business performance

- 10.8.7 Major Strategic Initiatives and Developments

- 10.9 Pfizer

- 10.9.1 Company Overview

- 10.9.2 Key Executives

- 10.9.3 Company snapshot

- 10.9.4 Active Business Divisions

- 10.9.5 Product portfolio

- 10.9.6 Business performance

- 10.9.7 Major Strategic Initiatives and Developments

- 10.10 AbbVie

- 10.10.1 Company Overview

- 10.10.2 Key Executives

- 10.10.3 Company snapshot

- 10.10.4 Active Business Divisions

- 10.10.5 Product portfolio

- 10.10.6 Business performance

- 10.10.7 Major Strategic Initiatives and Developments

- 10.11 AstraZeneca

- 10.11.1 Company Overview

- 10.11.2 Key Executives

- 10.11.3 Company snapshot

- 10.11.4 Active Business Divisions

- 10.11.5 Product portfolio

- 10.11.6 Business performance

- 10.11.7 Major Strategic Initiatives and Developments

- 10.12 Gilead Sciences

- 10.12.1 Company Overview

- 10.12.2 Key Executives

- 10.12.3 Company snapshot

- 10.12.4 Active Business Divisions

- 10.12.5 Product portfolio

- 10.12.6 Business performance

- 10.12.7 Major Strategic Initiatives and Developments

- 10.13 BristolMyers Squibb

- 10.13.1 Company Overview

- 10.13.2 Key Executives

- 10.13.3 Company snapshot

- 10.13.4 Active Business Divisions

- 10.13.5 Product portfolio

- 10.13.6 Business performance

- 10.13.7 Major Strategic Initiatives and Developments

- 10.14 Sanofi

- 10.14.1 Company Overview

- 10.14.2 Key Executives

- 10.14.3 Company snapshot

- 10.14.4 Active Business Divisions

- 10.14.5 Product portfolio

- 10.14.6 Business performance

- 10.14.7 Major Strategic Initiatives and Developments

- 10.15 Roche

- 10.15.1 Company Overview

- 10.15.2 Key Executives

- 10.15.3 Company snapshot

- 10.15.4 Active Business Divisions

- 10.15.5 Product portfolio

- 10.15.6 Business performance

- 10.15.7 Major Strategic Initiatives and Developments

11: Analyst Perspective and Conclusion

- 11.1 Concluding Recommendations and Analysis

- 11.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Application |

|

By Drug Type |

|

By Route of Administration |

|

By Disease Severity |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Histoplasmosis Treatment in 2032?

+

-

Which application type is expected to remain the largest segment in the Global Histoplasmosis Treatment market?

+

-

How big is the Global Histoplasmosis Treatment market?

+

-

How do regulatory policies impact the Histoplasmosis Treatment Market?

+

-

What major players in Histoplasmosis Treatment Market?

+

-

What applications are categorized in the Histoplasmosis Treatment market study?

+

-

Which product types are examined in the Histoplasmosis Treatment Market Study?

+

-

Which regions are expected to show the fastest growth in the Histoplasmosis Treatment market?

+

-

Which region is the fastest growing in the Histoplasmosis Treatment market?

+

-

What are the major growth drivers in the Histoplasmosis Treatment market?

+

-