Global Hydrogen Car Market – Industry Trends and Forecast to 2030

Report ID: MS-2175 | Automotive and Transport | Last updated: Dec, 2024 | Formats*:

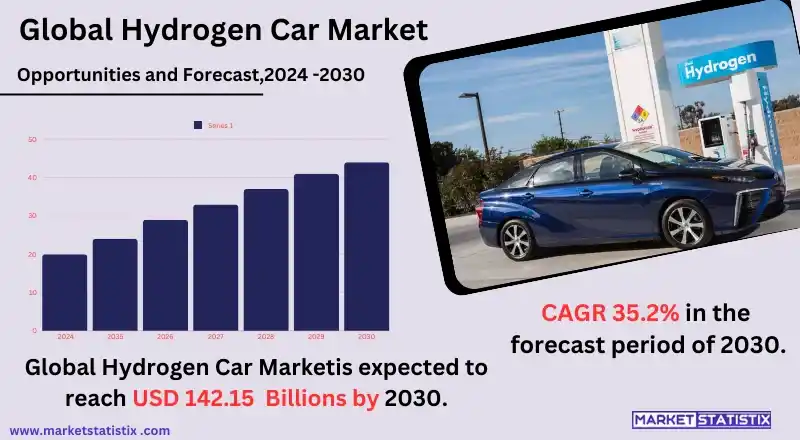

Hydrogen Car Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 35.2% |

| Forecast Value (2030) | USD 142.15 Billion |

| By Product Type | Passenger Cars, Commercial Vehicles |

| Key Market Players |

|

| By Region |

|

Hydrogen Car Market Trends

The hydrogen vehicle industry is booming, propelled by a global momentum toward carbon reduction and modal shift to sustainable travel. All around the world, governments have announced subsidies, tax benefits, and other policy support for the adoption of hydrogen fuel cell vehicles (FCEVs). Countries working on it are all largely focused on Japan, South Korea, Germany, and the U.S. Furthermore, improvements have been made with reference to hydrogen production, storage, and distribution technologies, which further improve the feasibility of hydrogen as a sustainable energy source for transportation. The growing publicity around hydrogen refuelling infrastructures is a prime factor responsible for fuelling market growth—the clinical engagement of leading manufacturers, namely Toyota, Hyundai, and Honda, in developing hydrogen fuel cell electric vehicles (FCEVs) will further boost growth in the coming years.Hydrogen Car Market Leading Players

The key players profiled in the report are Ballard Power Systems, BMW, Daimler AG (Mercedes-Benz), Honda Motor Co., Ltd, Hyundai Motor Company, ITM Power, Linde plc, Nel Hydrogen, Nikola Corporation, Plug Power Inc, Toyota Motor CorporationGrowth Accelerators

The market for hydrogen-powered cars is basically putting on evidence, pertaining to the increasing focus observed at international levels, in addition towards the urge and providing support for cleaner options of energy from its most significant parts to the 'old-fashioned' coal-burning and oil-dependent energy economies. Besides these, a lot of governments have introduced certain policy measures to reduce greenhouse emissions. Hence, all of these factors encourage and facilitate the adoption of zero-emission vehicles, such as hydrogen fuel cell electric vehicles (FCEVs). They also include tax benefits, subsidies, investments in hydrogen refuelling infrastructures, and so on. Another driving force has been the steadily increasing call for sustainable transport initiatives in areas that include those of logistics and public transit. Hydrogen cars offer even better ranges and quicker replenishment times than battery electric vehicles and are thus suited for over-the-road transport and heavy-duty vehicles. There are also alliances by auto companies, energy firms, and governments attempting to address making a hydrogen economy viable, with such endeavours being producing green hydrogen on a larger scale, developing supply chains, and deploying hydrogen fleets in cities.Hydrogen Car Market Segmentation analysis

The Global Hydrogen Car is segmented by Type, and Region. By Type, the market is divided into Distributed Passenger Cars, Commercial Vehicles . Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The hydrogen car market is highly competitive, wherein a few of the prominent players are competing against each other, such as Toyota, Hyundai, and Honda, founders in the development and commercial introduction of hydrogen fuel cell vehicles. These have long been spending on research and development, designing improvements on hydrogen cars in terms of performance and costs throughout the area of automotive manufacturing. Other big names include Hyundai Motor Company, GM, and Daimler AG. These are active participants in the deployment of hydrogen fuel cell technologies and the wider portfolio offerings. There are also many start-ups and smaller companies coming up focusing on niche areas of the hydrogen fuel cell ecosystem, such as components or hydrogen production technologies.Challenges In Hydrogen Car Market

Perhaps the biggest hurdle in hydrogen cars is the lack of a proper network of refuelling stations, as building these is a costly and difficult logistical affair. Original network density is practically impossible to achieve in most cases, especially from a consumer convenience perspective. The costs and energy requirements for producing, storing, and transporting hydrogen have unavoidably rendered it expensive and energy-intensive, especially if it comes from non-renewable sources, nullifying hydrogen's advantages in environmental terms. All these factors slow down the market and erode consumer confidence in technology. Another major hurdle is the contest with rapidly improving battery electric vehicles (BEVs). Technology improvements and cost reductions in BEV systems are matched by growing infrastructure utilities built upon a better charging network. At the same time, BEVs are seen as an easier option because of lower upfront costs and an easier energy distribution model. Concerns over the limited economies of scale that hydrogen vehicles can count on because their market remains quite niche compound hopes regarding hydrogen vehicles' scalability. Such low demand, thus, makes high costs, which discourage adoption. These hurdles require huge investment and innovation, as well as supporting government policies, to level the playing field.Risks & Prospects in Hydrogen Car Market

Hydrogen car markets have shown significant opportunities for growth owing to increased global efforts for sustainability and reduction in carbon emission levels. Incentives and policies have been driving governments all over the world to switch from traditional energy resource alternatives to new and clean energy. These policies create an easier platform for hydrogen fuel cell vehicle (FCV) adoption. Furthermore, innovations that support the production, storage, and refuelling infrastructure of hydrogen have combined with the decreasing costs of fuel cells to operate as key stimulants in speeding up the market. It is important to note that hydrogen cars are highly competitive among passenger and commercial vehicle segments with long driving ranges, quick refuelling times, and zero tailpipe emissions. Other available market opportunities also show promise for greater partnerships between automakers, energy companies, and nations concerned with developing hydrogen ecosystems. Such industries as logistics, public transport, and heavy-duty trucking are arguably now the readiest for hydrogen adoption since they rely on having such high energy density and fast refuelling. The rising awareness of energy security and diversification will also increase investments in the production of green hydrogen in line with global decarbonisation ambitions.Key Target Audience

The key target audience for hydrogen vehicles includes an extensive market that includes environmentally friendly consumers, as well as fleet operators and businesses seeking sustainable solutions. In fact, these vehicles attract one and all who wish to run a low-emission transport operation because they produce no greenhouse gas emissions while in operation, and they offer faster refuelling times compared with battery electric vehicles. This audience is most often represented by tech-savvy early adopters, eco-minded millennials, as well as urban commuters who search for efficient and green mobility alternatives.,, Another such important segment of the market includes industries demanding very high mileage requirements, like logistics, ride-hailing, and long-distance transport operators. These users will stand to benefit from hydrogen vehicles' long-range and quick refuelling capabilities to ensure their operations run continuously and heavily. Last, but sure to belong in any primary segment, are competing emerging markets in regions where hydrogen infrastructures are being created. Here, businesses and consumers will be involved in adopting technological caches as part of global sustainability goals.Merger and acquisition

In the realm of hydrogen car sectors, so much is happening in recent times about mergers and collaborations, all aimed towards better avenues into the industry's growth and technological advancement. HUTURE Ltd. signing a merger agreement with Aquaron Acquisition Corp. valued around $1 billion is one of them. HUTURE is the company that deals solely in the manufacture of hydrogen-enabled vehicles. The merger will help it develop its research & development prowess and carve a market presence as it steps into being a public company in the confines of the Nasdaq Stock Market. The deal is reported to take place later this year, subject to approvals from regulators and shareholders. Strategic partnerships—not just the organisations with mergers—will also change the face of hydrogen vehicles. Accordingly, Toyota announced a wide-ranging partnership in collaboration with BMW to enhance fuel cell technology and develop a new breed of hydrogen vehicles. The newly announced agreement builds upon the prior historic cooperation between these two giants; it provides a framework for standardising components in order to save costs and increase consumer affordability. It involves both parties, but they plan to launch their first mass-produced fuel cell electric vehicle (FCEV) by 2028, claiming that Toyota will supply primary components while BMW takes care of production purposes. Also, Hyundai goes together with Škoda to fast-track hydrogenization in Europe, again stressing technology and applications outside mobility, including heavy industries.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Hydrogen Car- Snapshot

- 2.2 Hydrogen Car- Segment Snapshot

- 2.3 Hydrogen Car- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Hydrogen Car Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Passenger Cars

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Commercial Vehicles

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Hydrogen Car Market by Vehicle

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Passenger cars

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Commercial vehicle

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Buses

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 TrucksPassenger cars

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Commercial vehicle

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

- 5.7 Buses

- 5.7.1 Key market trends, factors driving growth, and opportunities

- 5.7.2 Market size and forecast, by region

- 5.7.3 Market share analysis by country

- 5.8 Trucks

- 5.8.1 Key market trends, factors driving growth, and opportunities

- 5.8.2 Market size and forecast, by region

- 5.8.3 Market share analysis by country

6: Hydrogen Car Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Ballard Power Systems

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 BMW

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Daimler AG (Mercedes-Benz)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Honda Motor Co.

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Ltd

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Hyundai Motor Company

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 ITM Power

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Linde plc

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Nel Hydrogen

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Nikola Corporation

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Plug Power Inc

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Toyota Motor Corporation

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Vehicle |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Hydrogen Car in 2030?

+

-

How big is the Global Hydrogen Car market?

+

-

How do regulatory policies impact the Hydrogen Car Market?

+

-

What major players in Hydrogen Car Market?

+

-

What applications are categorized in the Hydrogen Car market study?

+

-

Which product types are examined in the Hydrogen Car Market Study?

+

-

Which regions are expected to show the fastest growth in the Hydrogen Car market?

+

-

What are the major growth drivers in the Hydrogen Car market?

+

-

Is the study period of the Hydrogen Car flexible or fixed?

+

-

How do economic factors influence the Hydrogen Car market?

+

-