Global Hydrogen Fuel Cell Engine Market – Industry Trends and Forecast to 2030

Report ID: MS-2121 | Automotive and Transport | Last updated: Dec, 2024 | Formats*:

Hydrogen Fuel Cell Engine Report Highlights

| Report Metrics | Details |

|---|---|

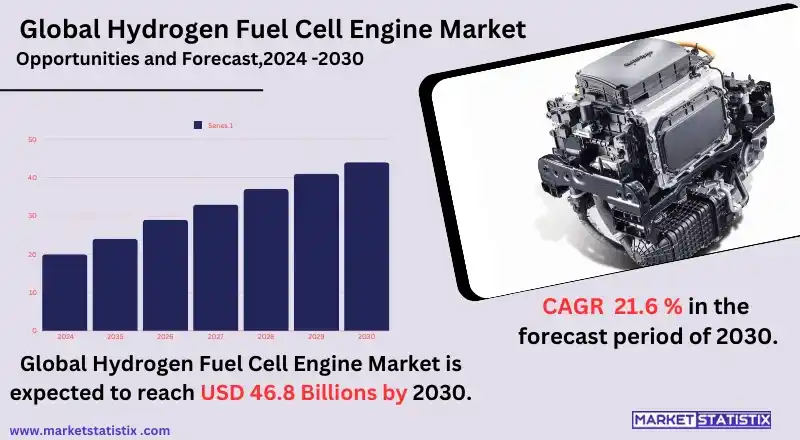

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 21.6% |

| Forecast Value (2030) | USD 46.8 Billion |

| By Product Type | Proton Exchange Membrane Fuel Cell, Solid Oxide Fuel Cell, Phosphoric Acid Fuel Cell, Others |

| Key Market Players |

|

| By Region |

|

Hydrogen Fuel Cell Engine Market Trends

The market for hydrogen fuel cell engines is booming primarily owing to growing inclination towards clean energy options coupled with government policies aimed at cutting down on emissions. Some of the major trends include improved storage technologies for hydrogen, the designing of efficient fuelling causes that will be cheaper to install and use, and the growth of hydrogen filling station networks across the globe. Industries like transport, especially in heavy-duty vehicles such as buses and trucks, are increasingly relying on hydrogen fuel cells due to their superior long-range capabilities, fast refuelling time, and zero emission of pollutants. Furthermore, drones and unmanned surface vessels are some examples of systems that take advantage of hydrogen fuel cell capabilities utterly different from ground transport. Government-private-research institutions’ collaborations are enhancing innovative capabilities and scalability of the market. In addition, erecting usage of hydrogen fuel cells in various sectors is a securing factor because the prices of green hydrogen produced using renewable energy are coming down. Hence, this makes the market fit for aggressive expansion in the next few years.Hydrogen Fuel Cell Engine Market Leading Players

The key players profiled in the report are Ceres Power (U.K.), AVL (Austria), Pragma Industries (France), Mitsubishi Hitachi Power Systems (Japan), W.L. Gore & Associates (U.S.), Nedstack Fuel Cell Technology (Netherlands), Proton Motor Fuel Cell GmbH (Germany), Bloom Energy (U.S.), Elcogen (Estonia), Nexceris LLC (U.S.), SFS Energy AG (Germany), Blue World Technologies (Denmark), Roland Gumpert (Germany), AISIN (Japan), Convion (Finland), ITM Power (U.K.), Plug Power (U.S.), Nuvera Fuel Cells, LLC (U.S.), FuelCell Energy (U.S.)Growth Accelerators

In the recent few decades, there has been increasing global focus towards the reduction of carbon emissions and the adoption of cleaner energy sources that has positively impacted the hydrogen fuel cell engine market. In every nation, there are strict emission controls, and governments also support these technologies by subsidizing their introduction in transportation and manufacturing processes that employ hydrogen fuel cells. Focus on the production of renewable sources of energy and improvements in hydrogen infrastructure, which includes production, storage, and distribution, also enhances the growth of this market. Moreover, the increasing need for zero-emission vehicles (ZEVs) from the automotive, marine, and spacecraft industries is another key growth factor. Hydrogen fuel cells have a number of advantages, including high energy efficiency, quick refuelling, and long range, which make them a better option than conventional vehicles with internal combustion engines and battery-operated vehicles. Also, the rising investment by the major market players in research and development and collaborations for increasing the hydrogen fuel cell production capacity are also helping to increase the adoption of hydrogen fuel cells in the market.Hydrogen Fuel Cell Engine Market Segmentation analysis

The Global Hydrogen Fuel Cell Engine is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Proton Exchange Membrane Fuel Cell, Solid Oxide Fuel Cell, Phosphoric Acid Fuel Cell, Others . The Application segment categorizes the market based on its usage such as Transport, Stationary, Portable. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive landscape of the hydrogen fuel cell engine market is a mix of interactions between the players from the automotive, energy, and technology industries. Toyota, Hyundai, and Honda are the dominating players with their respective hydrogen fuel cell vehicles (FCVs), such as the Toyota Mirai and the Hyundai Nexon, among others. Such companies typically pursue a strategy supported by intensive research in order to enhance the performance of fuel cells, cut costs, and increase the availability of hydrogen. Moreover, Nikola Corporation and Plug Power are new entrants who are proving the competition by venturing into hydrogen-powered commercial vehicles and trucks, as well as industrial applications, respectively. At the same time, the formation of strategic alliances and joint ventures emerges as one of the significant tactics in the market, as they allow the enterprises to improve their technologies as well as develop hydrogen fuel networks. Car manufacturers are acting in partnership with energy companies and infrastructure operators to construct refuelling stations in order to further promote the use of hydrogen fuel cells.Challenges In Hydrogen Fuel Cell Engine Market

There are several hurdles that the hydrogen fuel cell engine market is overcoming concerning infrastructure and affordability. One of the main challenges is the lack of hydrogen filling stations, which is predominant in all other areas apart from the primary markets such as Europe, Japan, and California. This introduction in certain areas limits market acceptance, as consumers and businesses are not likely to spend on hydrogen fuel cell cars without the guarantee that the cars can easily be refuelled. Moreover, there are high costs concerning hydrogen fuel supply, especially due to the processes involved in obtaining hydrogen and keeping it in storage. Another issue is the construction of integrated systems for hydrogen fuel cell vehicles (FCVs). Finally, thanks to technological progress in production fuel cell systems and construction materials like platinum catalysts, they are still relatively pricey. This impacts the hydrogen-powered car as much as vehicle-owning businessmen and women, making the sales of such cars lower than those of electric vehicles that already have existing manufacturing and are less expensive. And last, it is the concerns over the sustainability of hydrogen production through non-renewable resources that irks the green consumers and advocates policy change.Risks & Prospects in Hydrogen Fuel Cell Engine Market

Several factors motivate the emergence of the hydrogen fuel cell engines market as a result of the prevailing trends advocating for clean energy and decarbonization. More government policies and spending geared towards hydrogen infrastructure and support of stringent emission controls are favourable for adsorption. Transportation, power generation, and heavy machinery industries have begun substituting hydrogen in place of fossil fuels, especially in long-distance trucking, shipping, and fuelling buses where battery solutions are limited. Moreover, improvements in the fuel cell have cut down on the price and made the energy more efficient. The automotive sector is also becoming more active in the use of hydrogen with the help of research and development collaborations, which in turn aids in the expansion of the market. Developing countries too are financing hydrogen initiatives to enhance energy security, enhancing the growth of the market.Key Target Audience

The hydrogen fuel cell engine market is primarily aimed at businesses involved in manufacturing and heavy industries, such as automotive and transportation, who wish to cut carbon emissions while enhancing energy efficiency. This market is appealing to big players in the industry, particularly those engaged in electric vehicles (EVs), who are eager to expand their product mix by incorporating green energy options. Major stakeholders include automotive original equipment manufacturers (OEMs), fleet owners, and transport and logistics companies planning on implementing hydrogen fuel cells in buses, trucks, and trains, including other commercial vehicles with less detrimental effects on the environment than the internal combustion engine powered by fossil fuels.,, In addition, governments and environmental organizations are also considered target audiences since they facilitate the adoption of clean energy technologies through influence and funding. As part of being stakeholders, they are also engaged in the development and promotion of hydrogen fuel cell systems due to the progressive environmental regulations as well as the achievement of carbon-neutral objectives. They also form an important market segment, as they deal with hydrogen technologies and their global energy transition as well.Merger and acquisition

It has been observed that the hydrogen fuel cell engine sector has experienced rapid improvements primarily through strategic mergers and acquisitions. Recently, HD Hydrogen announced that it would pay FSC Technologies a total of €72 million for Convion Oy, which is located in Finland. Since the announcement was made in November 2023, it is clear that HD Hydrogen’s interest in solid oxide fuel cell and electrolyzer technologies is focused on helping the company’s prospects in the hydrogen fuel cell-targeted growth market. Cooperation is expected to improve stationary power generation and marine fuel cell technology, as the latter is more favourable with growth in demand for the clean energy-based solutions because of the industry reshaping mergers and acquisitions. In addition to HD Hydrogen's acquisition, marketplace shares are also being created through the use of strategic partnerships by other market players. For example, scouts from Honda and General Motors showed a teaser of the next-gen hydrogen fuel cell technology during the recent European Hydrogen Week in March, which means they entered into a joint development agreement to work on fuel cell technology. In this regard, it is hoped that the relationship between the two companies will help provide more products in the hydrogen market, especially due to the rising government and private investment, which is key in hydrogen infrastructure and vehicle development.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Hydrogen Fuel Cell Engine- Snapshot

- 2.2 Hydrogen Fuel Cell Engine- Segment Snapshot

- 2.3 Hydrogen Fuel Cell Engine- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Hydrogen Fuel Cell Engine Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Proton Exchange Membrane Fuel Cell

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Solid Oxide Fuel Cell

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Phosphoric Acid Fuel Cell

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Others

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

5: Hydrogen Fuel Cell Engine Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Transport

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Stationary

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Portable

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Hydrogen Fuel Cell Engine Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Ceres Power (U.K.)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 AVL (Austria)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Pragma Industries (France)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Mitsubishi Hitachi Power Systems (Japan)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 W.L. Gore & Associates (U.S.)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Nedstack Fuel Cell Technology (Netherlands)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Proton Motor Fuel Cell GmbH (Germany)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Bloom Energy (U.S.)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Elcogen (Estonia)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Nexceris LLC (U.S.)

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 SFS Energy AG (Germany)

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Blue World Technologies (Denmark)

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Roland Gumpert (Germany)

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 AISIN (Japan)

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Convion (Finland)

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 ITM Power (U.K.)

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 Plug Power (U.S.)

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

- 8.18 Nuvera Fuel Cells

- 8.18.1 Company Overview

- 8.18.2 Key Executives

- 8.18.3 Company snapshot

- 8.18.4 Active Business Divisions

- 8.18.5 Product portfolio

- 8.18.6 Business performance

- 8.18.7 Major Strategic Initiatives and Developments

- 8.19 LLC (U.S.)

- 8.19.1 Company Overview

- 8.19.2 Key Executives

- 8.19.3 Company snapshot

- 8.19.4 Active Business Divisions

- 8.19.5 Product portfolio

- 8.19.6 Business performance

- 8.19.7 Major Strategic Initiatives and Developments

- 8.20 FuelCell Energy (U.S.)

- 8.20.1 Company Overview

- 8.20.2 Key Executives

- 8.20.3 Company snapshot

- 8.20.4 Active Business Divisions

- 8.20.5 Product portfolio

- 8.20.6 Business performance

- 8.20.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Hydrogen Fuel Cell Engine in 2030?

+

-

How big is the Global Hydrogen Fuel Cell Engine market?

+

-

How do regulatory policies impact the Hydrogen Fuel Cell Engine Market?

+

-

What major players in Hydrogen Fuel Cell Engine Market?

+

-

What applications are categorized in the Hydrogen Fuel Cell Engine market study?

+

-

Which product types are examined in the Hydrogen Fuel Cell Engine Market Study?

+

-

Which regions are expected to show the fastest growth in the Hydrogen Fuel Cell Engine market?

+

-

What are the major growth drivers in the Hydrogen Fuel Cell Engine market?

+

-

Is the study period of the Hydrogen Fuel Cell Engine flexible or fixed?

+

-

How do economic factors influence the Hydrogen Fuel Cell Engine market?

+

-