Global Intravenous Iv therapy and Vein Access Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2031

Report ID: MS-2013 | Medical Devices | Last updated: Dec, 2024 | Formats*:

Intravenous iv therapy and vein access Report Highlights

| Report Metrics | Details |

|---|---|

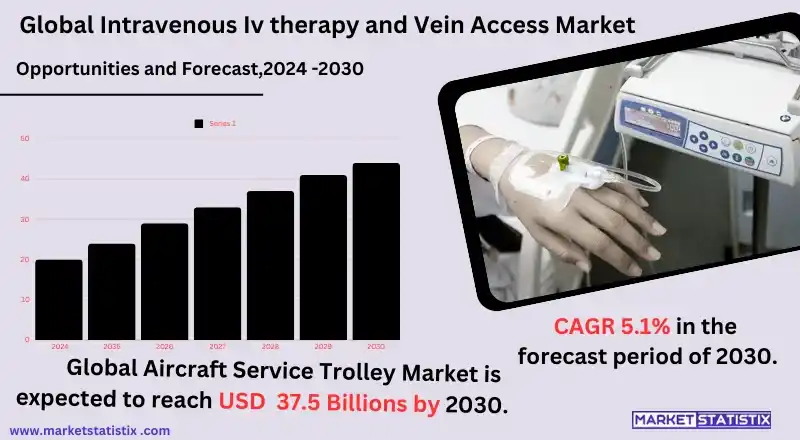

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 5.1% |

| Forecast Value (2031) | USD 37.5 billion |

| By Product Type | Continuous IV Therapy, Intermittent IV Therapy, IV Push Therapy |

| Key Market Players |

|

| By Region |

|

Intravenous iv therapy and vein access Market Trends

The intravenous (IV) therapy and vein access market is undergoing changes towards advanced technologies that are less invasive and optimised for patient comfort while reducing complications. One notable trend is the enhanced adoption of ultrasound-guided vein access devices that improve needle placement, especially in patients with challenging vein access. Also, there is increased uptake of anti-microbial catheters and securement devices as healthcare providers seek to control infections and enhance patient outcomes. These innovations are especially meaningful in intensive care units and for patients on prolonged intravenous therapy. Moreover, the theragnostic branch of medicine is evidenced by the increasing shift towards home healthcare and ambulatory application of IV therapy treatments, where the demand for treatment without inflexible, expensive solutions is increasing. Due to advanced ages and increased chronic illness rates, patients are more often being hydrated, treated with antibiotics, or undergoing chemotherapy without the confines of a hospital. This has called for the invention of small, consumer-grade IV good pumps, IV access devices that can be placed on the arm, and IV therapy enhanced by telemedicine services, which are convenient for the patients and ease the load on the healthcare system.Intravenous iv therapy and vein access Market Leading Players

The key players profiled in the report are B.Braun SE, Baxter International Inc., Becton Dickinson and Co., Cardinal Health Inc., Fresenius SE and Co. KGaA, ICU Medical Inc., IRadimed Corp., Medtronic Plc, Poly Medicure Ltd., Smith and Nephew plc, Tekni Plex Inc., Teleflex Inc., Terumo Corp., Vygon SASGrowth Accelerators

The market for IV therapy and venous access devices is largely attributable to the increasing incidence of chronic illnesses and situations, such as cancer, diabetes, and autoimmune disorders, that necessitate prolonged antibiotic treatment by IV medication. Cancer-related illnesses and complications are responsible for the increased demand for effective vein access and IV therapy solutions owing to the faster-growing ageing population. As a result, older populations usually get sustained medical attention in shorter intervals. Furthermore, the rise in the number of surgeries and lodgings across countries raises the need for IV therapy, which is critical in that it supplies fluids, medicines, and nutrition to patients who are incapable of ingestion. Technological progress in tube systems and sutures that has been crucial in improving use by patients, minimising the risk of infections, and helping the health workers in the working process is another important factor. These active developments, such as ultrasound vein access devices for placing central venous catheters, needle-free connectors, and antimicrobial catheters, are responding to the demand for safer, more effective, and less invasive intravenous means by the medical market. In addition, there is a rising need for portable and easy-to-use IV therapy devices on the market due to the increasing trend of patients opting for medical care at home rather than in hospitals.Intravenous iv therapy and vein access Market Segmentation analysis

The Global Intravenous iv therapy and vein access is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Continuous IV Therapy, Intermittent IV Therapy, IV Push Therapy . The Application segment categorizes the market based on its usage such as Medication administration, Blood-based products, Nutrition and buffer solution, Volume expander. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Challenges In Intravenous iv therapy and vein access Market

The IV therapy and vein access market grapples with a number of issues, most notably that of patient safety and complications associated with vein access. Among these challenges, the prevention of numerous infective and inflammatory complications, e.g., phlebitis, infiltration, and sepsis, with the most ubiquitous complication being the recurrent use of IV access, is a major challenge. Hence, healthcare systems and providers are obliged to follow very stringent protocols to contain such risks, which entails periodic retraining and supervision of health workers together with maintenance of the clean environment, which is very laborious and expensive. Besides, the problem of control pertains to infections in the context of resistance to such treatment, which therefore complicates and necessitates the need for high-level containment strategies. Markedly, there is another major challenge that presents itself in the form of patient population, for instance, elderly obese and diabetic individuals who have less visible or accessible veins and therefore present difficulties in IV therapy. In such situations, more often than not, locating a suitable vein for IV therapy requires special expertise and, in some instances, sophisticated methods such as ultrasound, which entail extra expenses and a higher level of training for medical practitioners. Furthermore, due to the cost impact on healthcare systems, the introduction of new technologies that are intended to enhance the efficiency of vein access and improve patient management is often not embraced.Risks & Prospects in Intravenous iv therapy and vein access Market

The IV therapy and vein access market has several attractive opportunities, especially due to the increasing burden of chronic illnesses and the greater need for efficacious administration of drugs in a fast manner. As the number of patients diagnosed with cancer, diabetes, cardiovascular diseases, and other conditions increases, there is a frequent need for IV therapies, which include and do not limit to chemotherapy, pain relief, and nutrition infusion that all depend on reliable vein access provision. Such a trend provides room for the development of better IV therapy devices that are more user-friendly, reduce the risk of infection during the process, and are precise when inserting them, especially for the elderly and people with hard-to-find veins. Another major opportunity is the innovation of portable and home-use intravenous therapy systems as the healthcare pattern turns towards outpatient and house call services. The expansion of telemedicine and home healthcare services has also increased the need for small and simple vein access devices that allow treatment of the patient without being confined to a hospital. This has also triggered the development of advanced devices for vein access, remote device monitoring, and the provision of intravenous therapy that is less invasive and guided home healthcare in the day-to-day care of a patient that has distinct benefits for health givers and the patients seeking care. The IV therapy and vein access market has several attractive opportunities, especially due to the increasing burden of chronic illnesses and the greater need for efficacious administration of drugs in a fast manner. As the number of patients diagnosed with cancer, diabetes, cardiovascular diseases, and other conditions increases, there is a frequent need for IV therapies, which include and do not limit to chemotherapy, pain relief, and nutrition infusion that all depend on reliable vein access provision. Such a trend provides room for the development of better IV therapy devices that are more user-friendly, reduce the risk of infection during the process, and are precise when inserting them, especially for the elderly and people with hard-to-find veins. Another major opportunity is the innovation of portable and home-use intravenous therapy systems as the healthcare pattern turns towards outpatient and house call services. The expansion of telemedicine and home healthcare services has also increased the need for small and simple vein access devices that allow treatment of the patient without being confined to a hospital. This has also triggered the development of advanced devices for vein access, remote device monitoring, and the provision of intravenous therapy that is less invasive and guided home healthcare in the day-to-day care of a patient that has distinct benefits for health givers and the patients seeking care.Key Target Audience

The IV therapy and vein access market primarily looks to healthcare service providers, such as hospitals, outpatient clinics, and long-term care facilities, at which intravenous therapy becomes a must for direct intravenous infusion of fluids, medicines, and nutrients into patients' blood streams. Physicians, nurses, medical professionals, and other staff members who look for reliable, easy-to-use vein access devices that ensure safe and efficient patient care, especially in situations requiring extended therapy or high-accuracy medication delivery, fall into this category. Increasing prevalence of chronic diseases and an ageing population are among the factors with which the demand for IV therapy is increasing in the home care setting, where care providers and carers require simple and minimally invasive vein access technologies.,, Another relevant party in this market includes pharmaceutical companies and medical device manufacturers. They design advanced IV therapy products, such as needle-free devices, smart IV pumps, and catheter stabilization products that are designed to maximize safety, comfort, and compliance with demanding regulatory standards. Research centre with regards to innovative vein access technologies are also considered relevant parties since they are working with products that will reduce discomfort for patients, minimize the risk of infection, and maximize efficiency in various clinical settings.Merger and acquisition

Fresenius Ka bi and ICU Medical have also been active in the intravenous (IV) therapy and vein access market thanks to recent mergers and acquisitions. Fresenius Ka bi announced that it had completed the acquisition of the infusion therapy company Ivenix for 240 million dollars plus performance-based milestones. The acquisition is expected to strengthen Fresenius Kabi’s offerings through the addition of Ivenix’s modern infusion technology that is poised for growth in the MedTech sector and enhancing patient care in the whole of the USA. Likewise, ICU Medical also informed about the acquisition of Hospira Infusion Systems from Pfizer for 1 billion dollars, which will cement the company's rank as the dedicated infusion therapy provider. The purpose of this merger is to develop an entire product line that includes IV solutions along with pumps and devices, which upgrades the company's competitiveness in the international market. In the wake of these significant transactions, Vivo Infusion incorporated Infusion Associates, taking its reach to close to 80 ambulatory infusion centres in 15 states. This is intended to bolster Vivo’s operational capacity and improve patient care delivery in those areas where services have been previously limited. Dynamic Infusion has also remained busy by bringing in Infuzicare and Columbus Speciality Nursing, thereby making it possible for the company to provide home infusion nursing services to additional territories. These developments are part of a larger picture of continued consolidation within the infusion therapy market as companies look to enhance their service provision while dealing with the increasing appetite for niche health care services.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Intravenous iv therapy and vein access- Snapshot

- 2.2 Intravenous iv therapy and vein access- Segment Snapshot

- 2.3 Intravenous iv therapy and vein access- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Intravenous iv therapy and vein access Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Continuous IV Therapy

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Intermittent IV Therapy

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 IV Push Therapy

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Intravenous iv therapy and vein access Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Medication administration

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Blood-based products

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Nutrition and buffer solution

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Volume expander

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

6: Intravenous iv therapy and vein access Market by Device Type

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Peripheral IV Catheters

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Central Venous Catheters

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Midline Catheters

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

7: Intravenous iv therapy and vein access Market by Patient Type

- 7.1 Overview

- 7.1.1 Market size and forecast

- 7.2 Pediatric Patients

- 7.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.2 Market size and forecast, by region

- 7.2.3 Market share analysis by country

- 7.3 Adult Patients

- 7.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.2 Market size and forecast, by region

- 7.3.3 Market share analysis by country

- 7.4 Geriatric Patients

- 7.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.2 Market size and forecast, by region

- 7.4.3 Market share analysis by country

8: Intravenous iv therapy and vein access Market by Region

- 8.1 Overview

- 8.1.1 Market size and forecast By Region

- 8.2 North America

- 8.2.1 Key trends and opportunities

- 8.2.2 Market size and forecast, by Type

- 8.2.3 Market size and forecast, by Application

- 8.2.4 Market size and forecast, by country

- 8.2.4.1 United States

- 8.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.1.2 Market size and forecast, by Type

- 8.2.4.1.3 Market size and forecast, by Application

- 8.2.4.2 Canada

- 8.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.2.2 Market size and forecast, by Type

- 8.2.4.2.3 Market size and forecast, by Application

- 8.2.4.3 Mexico

- 8.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.2.4.3.2 Market size and forecast, by Type

- 8.2.4.3.3 Market size and forecast, by Application

- 8.2.4.1 United States

- 8.3 South America

- 8.3.1 Key trends and opportunities

- 8.3.2 Market size and forecast, by Type

- 8.3.3 Market size and forecast, by Application

- 8.3.4 Market size and forecast, by country

- 8.3.4.1 Brazil

- 8.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.1.2 Market size and forecast, by Type

- 8.3.4.1.3 Market size and forecast, by Application

- 8.3.4.2 Argentina

- 8.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.2.2 Market size and forecast, by Type

- 8.3.4.2.3 Market size and forecast, by Application

- 8.3.4.3 Chile

- 8.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.3.2 Market size and forecast, by Type

- 8.3.4.3.3 Market size and forecast, by Application

- 8.3.4.4 Rest of South America

- 8.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.3.4.4.2 Market size and forecast, by Type

- 8.3.4.4.3 Market size and forecast, by Application

- 8.3.4.1 Brazil

- 8.4 Europe

- 8.4.1 Key trends and opportunities

- 8.4.2 Market size and forecast, by Type

- 8.4.3 Market size and forecast, by Application

- 8.4.4 Market size and forecast, by country

- 8.4.4.1 Germany

- 8.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.1.2 Market size and forecast, by Type

- 8.4.4.1.3 Market size and forecast, by Application

- 8.4.4.2 France

- 8.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.2.2 Market size and forecast, by Type

- 8.4.4.2.3 Market size and forecast, by Application

- 8.4.4.3 Italy

- 8.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.3.2 Market size and forecast, by Type

- 8.4.4.3.3 Market size and forecast, by Application

- 8.4.4.4 United Kingdom

- 8.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.4.2 Market size and forecast, by Type

- 8.4.4.4.3 Market size and forecast, by Application

- 8.4.4.5 Benelux

- 8.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.5.2 Market size and forecast, by Type

- 8.4.4.5.3 Market size and forecast, by Application

- 8.4.4.6 Nordics

- 8.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.6.2 Market size and forecast, by Type

- 8.4.4.6.3 Market size and forecast, by Application

- 8.4.4.7 Rest of Europe

- 8.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 8.4.4.7.2 Market size and forecast, by Type

- 8.4.4.7.3 Market size and forecast, by Application

- 8.4.4.1 Germany

- 8.5 Asia Pacific

- 8.5.1 Key trends and opportunities

- 8.5.2 Market size and forecast, by Type

- 8.5.3 Market size and forecast, by Application

- 8.5.4 Market size and forecast, by country

- 8.5.4.1 China

- 8.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.1.2 Market size and forecast, by Type

- 8.5.4.1.3 Market size and forecast, by Application

- 8.5.4.2 Japan

- 8.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.2.2 Market size and forecast, by Type

- 8.5.4.2.3 Market size and forecast, by Application

- 8.5.4.3 India

- 8.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.3.2 Market size and forecast, by Type

- 8.5.4.3.3 Market size and forecast, by Application

- 8.5.4.4 South Korea

- 8.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.4.2 Market size and forecast, by Type

- 8.5.4.4.3 Market size and forecast, by Application

- 8.5.4.5 Australia

- 8.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.5.2 Market size and forecast, by Type

- 8.5.4.5.3 Market size and forecast, by Application

- 8.5.4.6 Southeast Asia

- 8.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.6.2 Market size and forecast, by Type

- 8.5.4.6.3 Market size and forecast, by Application

- 8.5.4.7 Rest of Asia-Pacific

- 8.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 8.5.4.7.2 Market size and forecast, by Type

- 8.5.4.7.3 Market size and forecast, by Application

- 8.5.4.1 China

- 8.6 MEA

- 8.6.1 Key trends and opportunities

- 8.6.2 Market size and forecast, by Type

- 8.6.3 Market size and forecast, by Application

- 8.6.4 Market size and forecast, by country

- 8.6.4.1 Middle East

- 8.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 8.6.4.1.2 Market size and forecast, by Type

- 8.6.4.1.3 Market size and forecast, by Application

- 8.6.4.2 Africa

- 8.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 8.6.4.2.2 Market size and forecast, by Type

- 8.6.4.2.3 Market size and forecast, by Application

- 8.6.4.1 Middle East

- 9.1 Overview

- 9.2 Key Winning Strategies

- 9.3 Top 10 Players: Product Mapping

- 9.4 Competitive Analysis Dashboard

- 9.5 Market Competition Heatmap

- 9.6 Leading Player Positions, 2022

10: Company Profiles

- 10.1 B.Braun SE

- 10.1.1 Company Overview

- 10.1.2 Key Executives

- 10.1.3 Company snapshot

- 10.1.4 Active Business Divisions

- 10.1.5 Product portfolio

- 10.1.6 Business performance

- 10.1.7 Major Strategic Initiatives and Developments

- 10.2 Baxter International Inc.

- 10.2.1 Company Overview

- 10.2.2 Key Executives

- 10.2.3 Company snapshot

- 10.2.4 Active Business Divisions

- 10.2.5 Product portfolio

- 10.2.6 Business performance

- 10.2.7 Major Strategic Initiatives and Developments

- 10.3 Becton Dickinson and Co.

- 10.3.1 Company Overview

- 10.3.2 Key Executives

- 10.3.3 Company snapshot

- 10.3.4 Active Business Divisions

- 10.3.5 Product portfolio

- 10.3.6 Business performance

- 10.3.7 Major Strategic Initiatives and Developments

- 10.4 Cardinal Health Inc.

- 10.4.1 Company Overview

- 10.4.2 Key Executives

- 10.4.3 Company snapshot

- 10.4.4 Active Business Divisions

- 10.4.5 Product portfolio

- 10.4.6 Business performance

- 10.4.7 Major Strategic Initiatives and Developments

- 10.5 Fresenius SE and Co. KGaA

- 10.5.1 Company Overview

- 10.5.2 Key Executives

- 10.5.3 Company snapshot

- 10.5.4 Active Business Divisions

- 10.5.5 Product portfolio

- 10.5.6 Business performance

- 10.5.7 Major Strategic Initiatives and Developments

- 10.6 ICU Medical Inc.

- 10.6.1 Company Overview

- 10.6.2 Key Executives

- 10.6.3 Company snapshot

- 10.6.4 Active Business Divisions

- 10.6.5 Product portfolio

- 10.6.6 Business performance

- 10.6.7 Major Strategic Initiatives and Developments

- 10.7 IRadimed Corp.

- 10.7.1 Company Overview

- 10.7.2 Key Executives

- 10.7.3 Company snapshot

- 10.7.4 Active Business Divisions

- 10.7.5 Product portfolio

- 10.7.6 Business performance

- 10.7.7 Major Strategic Initiatives and Developments

- 10.8 Medtronic Plc

- 10.8.1 Company Overview

- 10.8.2 Key Executives

- 10.8.3 Company snapshot

- 10.8.4 Active Business Divisions

- 10.8.5 Product portfolio

- 10.8.6 Business performance

- 10.8.7 Major Strategic Initiatives and Developments

- 10.9 Poly Medicure Ltd.

- 10.9.1 Company Overview

- 10.9.2 Key Executives

- 10.9.3 Company snapshot

- 10.9.4 Active Business Divisions

- 10.9.5 Product portfolio

- 10.9.6 Business performance

- 10.9.7 Major Strategic Initiatives and Developments

- 10.10 Smith and Nephew plc

- 10.10.1 Company Overview

- 10.10.2 Key Executives

- 10.10.3 Company snapshot

- 10.10.4 Active Business Divisions

- 10.10.5 Product portfolio

- 10.10.6 Business performance

- 10.10.7 Major Strategic Initiatives and Developments

- 10.11 Tekni Plex Inc.

- 10.11.1 Company Overview

- 10.11.2 Key Executives

- 10.11.3 Company snapshot

- 10.11.4 Active Business Divisions

- 10.11.5 Product portfolio

- 10.11.6 Business performance

- 10.11.7 Major Strategic Initiatives and Developments

- 10.12 Teleflex Inc.

- 10.12.1 Company Overview

- 10.12.2 Key Executives

- 10.12.3 Company snapshot

- 10.12.4 Active Business Divisions

- 10.12.5 Product portfolio

- 10.12.6 Business performance

- 10.12.7 Major Strategic Initiatives and Developments

- 10.13 Terumo Corp.

- 10.13.1 Company Overview

- 10.13.2 Key Executives

- 10.13.3 Company snapshot

- 10.13.4 Active Business Divisions

- 10.13.5 Product portfolio

- 10.13.6 Business performance

- 10.13.7 Major Strategic Initiatives and Developments

- 10.14 Vygon SAS

- 10.14.1 Company Overview

- 10.14.2 Key Executives

- 10.14.3 Company snapshot

- 10.14.4 Active Business Divisions

- 10.14.5 Product portfolio

- 10.14.6 Business performance

- 10.14.7 Major Strategic Initiatives and Developments

11: Analyst Perspective and Conclusion

- 11.1 Concluding Recommendations and Analysis

- 11.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Device Type |

|

By Patient Type |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Intravenous iv therapy and vein access in 2031?

+

-

How big is the Global Intravenous iv therapy and vein access market?

+

-

How do regulatory policies impact the Intravenous iv therapy and vein access Market?

+

-

What major players in Intravenous iv therapy and vein access Market?

+

-

What applications are categorized in the Intravenous iv therapy and vein access market study?

+

-

Which product types are examined in the Intravenous iv therapy and vein access Market Study?

+

-

Which regions are expected to show the fastest growth in the Intravenous iv therapy and vein access market?

+

-

What are the major growth drivers in the Intravenous iv therapy and vein access market?

+

-

Is the study period of the Intravenous iv therapy and vein access flexible or fixed?

+

-

How do economic factors influence the Intravenous iv therapy and vein access market?

+

-