Global MicroLED Technology Market – Industry Trends and Forecast to 2030

Report ID: MS-2112 | Electronics and Semiconductors | Last updated: Dec, 2024 | Formats*:

MicroLED Technology Report Highlights

| Report Metrics | Details |

|---|---|

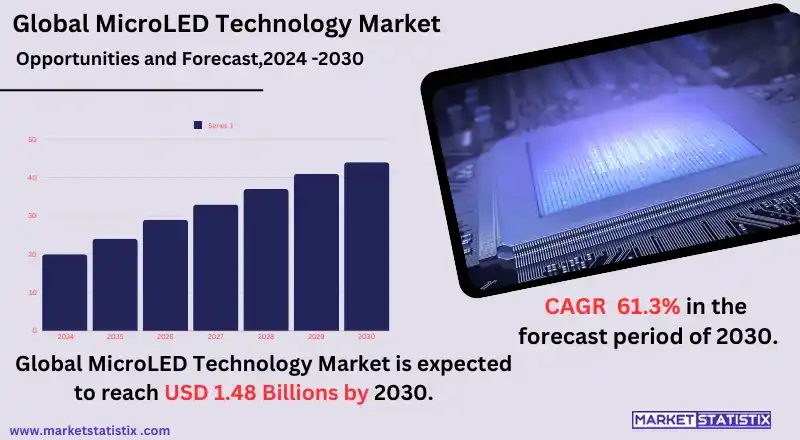

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 61.3% |

| Forecast Value (2030) | USD 1.48 Million |

| By Product Type | Display, Lighting |

| Key Market Players |

|

| By Region |

|

MicroLED Technology Market Trends

The global microLED technology market is on an upward trajectory due to the ability of microLED technology to deliver better display images than both LED and OLED technologies. In addition, the trend shows that there is an increase in the use of microLED technology in high-end television sets, wearables, and automotive displays. Major electronics manufacturers, especially those dealing with high-end product lines, are drawn to microLED technology because it can produce a display that is much brighter and more energy efficient with enhanced contrast and colour reproduction. On the other hand, there is an observable trend where various microLED technologies continue to be developed for the purpose of making them less expensive to manufacture. Companies are putting a lot of their funds into research with a view of making the assembly process easier, for instance, wafer-level bonding and applications of mass transfer to allow such components to be produced in large volumes economically. Such recent trends imply that microLED technology would become the mainstay in display technologies with its further development for commercialization in the other fields.MicroLED Technology Market Leading Players

The key players profiled in the report are Innolux Corporation, LG Display Co Ltd., Aledia SA., Epistar Corporation., Sony CorporationGrowth Accelerators

The global microLED technology market is largely influenced by the rising need for superior and low-energy visual solutions in many industries. MicroLED displays are brighter, more colour-accurate, and have better resolution than the typical OLED and LCD displays and so are well-suited for consumer electronics such as mobile gadgets, television sets, and smart wear. As end users of technology look for bigger, clearer, and more power-efficient screens, the technology of micro-LED is able to cater to these devices, explaining the adoption of such technology in high-end devices where growth of the market is witnessed. Another factor contributing to the market is the rapid adoption of microLED displays in the growing applications of augmented reality (AR) and virtual reality (VR). MicroLED technology’s superiority in high pixel density, low power consumption, and thinness of display makes it a perfect fit for use in AR/VR audiences encompassing headsets where very interactive experiences are expected. Furthermore, the emerging trends related to the growth in panoramic, seamless, high-definition screens for digital applications in arrangements such as that of automotive, digital signage, and entertainment further augment the expansion of the market.MicroLED Technology Market Segmentation analysis

The Global MicroLED Technology is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Display, Lighting . The Application segment categorizes the market based on its usage such as Smartphones & Tablets, NTE Devices, Televisions, Monitors and Laptops, Digital Signage, Smartwatches, Heads-up Display. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The macro trends that lease the interest of the microLED market involve the competition between big companies such as Sony Corporation, LG Display, Innolux Corporation, Aledia SA, and many others. These companies are heavily investing in research and development in order to improve and invent new technologies for microLED displays with the goal of mass production. Another common strategy that multiple companies employ is forming an alliance or a joint venture in order to be able to use different technologies and increase the geographical area of business operations. Also, new players looking to address specific usage within the microLED ecosystem have set in motion competition that is enhanced by the much greater eagerness of advancement in display technology.Challenges In MicroLED Technology Market

The high production costs are considered the main limiting factor for the growth of the global microLED technology market. The technology of micro-LED displays is complicated and involves a sophisticated process of attaching dozens of micro-LEDs to the display substrate. This process unfortunately entails high costs of fabrication, hence making micro-LED technologies expensive relative to the existing screen technologies, such as OLED and LCD displays. Hence, the use of microLED displays in consumer electronics is still constrained, especially in less expensive economies. One more hurdle lies in the scale-up and mass manufacturing of microLED screens. Although microLED systems present with the best attributes in terms of brightness, colour regelation, and energy efficiency, scaling the production of microLEDs to include complete devices, flat-screen televisions, mobile phones, and smart technology wearables is yet to be achieved. Aspects such as yield, uniformity, and integration with current display fabrication units present tremendous challenges.Risks & Prospects in MicroLED Technology Market

Thanks to the display, consumer electronics, and automotive sectors, the microLED technology market is characterized by a great scope of applications. Furthermore, since microLED displays can achieve higher brightness and energy efficiency while offering similar or superior brightness to traditional LCD or OLED displays, they are seen as a viable option for high-end televisions, smartphones, and smartwatches, among many others. The growth of advanced display technologies such as microLED is fuelled by increased demand for out-of-home displays and large-format screens in the entertainment, advertisement, and gaming sectors, thus increasing microLED adoption due to its unique features of thin, flexible, and scalable screens compared to other display technologies. Additionally, there exist optimistic outlooks in microLED technology in the automotive sector and the AR industry. With regards to automotive purposes, microLEDs can enhance traditional displays such as dashboard centres, head-up display units, and even back-view mirrors, improving the quality of inside space display systems. This is because microLEDs are very small and bright yet energy-saving; they support AR technologies, enabling lighter, and thus more convenient, solution spaces.Key Target Audience

The global microLED technology market primarily targets audiences such as display manufacturers, consumer electronics companies, and automotive industries. Display manufacturers are interested in microLED display technology with its possible superior brightness, colour gamut, and energy efficiency compared to the existing display technologies such as LCD and OLED. Additionally, consumer electronics manufacturers, particularly those involved in televisions, smartphones, and wearables, consider microLED a technology of the future that helps integrate rich and superior quality displays in their devices. Backlighting is not required for the technology to serve its purpose, colourful and clear images, and this is a great advantage for the high-end consumer electronics.,, At the same time, automotive manufacturers and advertising firms are also the major segments utilizing microLED technology. Automotive-producing companies are considering microLED technology for in-car displays, dashboards, and infotainment systems where high-quality imaging with low power and reliable components are required. Advertising agencies are also using microLED technology in large-format digital displays and posters in housing and street billboard applications where it can create very high-quality images in direct sunlight. Many sectors such as these are expected to propel the microLED market growth; hence it is anticipated that microLED will be a revolutionary technology across various sectors.Merger and acquisition

In recent years, the global microLED technology market has witnessed significant consolidation as players strive to become more competitive and technologically advanced. Most notably, Google recently acquired the microLED display startup Raxium, which specializes in displays for augmented and mixed reality. This deal, which was valued at nearly $1 billion, encourages the use of advanced displays in a myriad of devices, including a Google augmented reality headset billed for release in 2024, Project Iris. This move emphasizes the fact that the company is attempting to solidify its foothold in the AR ecosystem, considering the threat from rival companies like Apple and Meta Platforms. Furthermore, BOE Technology Group emerged to purchase HC-Semitek for $300 million, from which the funds for this acquisition will be used to set up a new microLED fabrication facility. The purpose of acquiring HC-Semitek is also to improve BOE’s performance in microLED, especially because microLED technology has increasingly become essential for high-definition displays in various areas, including consumer electronics and the automotive industry. In addition, the competition is also changing because, at the same time, microLED technologies are being developed by such companies as AUO and PlayNitride in order to meet the high appetite for high-end displays.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 MicroLED Technology- Snapshot

- 2.2 MicroLED Technology- Segment Snapshot

- 2.3 MicroLED Technology- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: MicroLED Technology Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Display

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Lighting

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: MicroLED Technology Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Smartphones & Tablets

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 NTE Devices

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Televisions

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Monitors and Laptops

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Digital Signage

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

- 5.7 Smartwatches

- 5.7.1 Key market trends, factors driving growth, and opportunities

- 5.7.2 Market size and forecast, by region

- 5.7.3 Market share analysis by country

- 5.8 Heads-up Display

- 5.8.1 Key market trends, factors driving growth, and opportunities

- 5.8.2 Market size and forecast, by region

- 5.8.3 Market share analysis by country

6: MicroLED Technology Market by Panel Size

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Micro-displays

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Large Panels

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

7: MicroLED Technology Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 Innolux Corporation

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 LG Display Co Ltd.

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 Aledia SA.

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 Epistar Corporation.

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Sony Corporation

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Panel Size |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of MicroLED Technology in 2030?

+

-

What is the growth rate of MicroLED Technology Market?

+

-

What are the latest trends influencing the MicroLED Technology Market?

+

-

Who are the key players in the MicroLED Technology Market?

+

-

How is the MicroLED Technology } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the MicroLED Technology Market Study?

+

-

What geographic breakdown is available in Global MicroLED Technology Market Study?

+

-

Which region holds the second position by market share in the MicroLED Technology market?

+

-

How are the key players in the MicroLED Technology market targeting growth in the future?

+

-

What are the opportunities for new entrants in the MicroLED Technology market?

+

-