Global Next-Generation Advanced Batteries Market - Industry Dynamics, Size, And Opportunity Forecast To 2031

Report ID: MS-376 | Chemicals And Materials | Last updated: Feb, 2025 | Formats*:

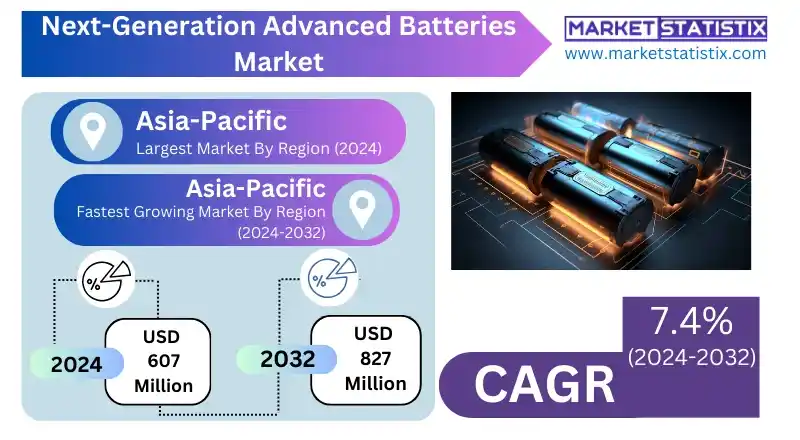

Next-Generation Advanced Batteries Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2032 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 10.24% |

| Forecast Value (2032) | USD 200.09 Billion |

| By Product Type | Solid-state Batteries, Sodium-ion Batteries, Lithium-Sulfur Batteries, Metal-air Batteries, Flow Batteries |

| Key Market Players |

|

| By Region |

|

Next-Generation Advanced Batteries Market Trends

The automotive industry is actively developing advanced battery technologies for improving range, charging speed, and safety in electric vehicles. Solid-state batteries, which provide higher energy density than lithium-ion batteries, thus furthering the growth of this segment, are considered to be safer. Next-generation advanced batteries will focus on sustainability and cost reduction. Manufacturers are actively exploring alternative battery chemistry that uses more abundant and sustainable materials to lessen the reliance on scarce resources, such as lithium. Furthermore, this involves modifying their production processes to drive down production costs and make advanced batteries economically accessible to a wider range of applications.Next-Generation Advanced Batteries Market Leading Players

The key players profiled in the report are LG Chem Ltd., CATL, Contemporary Amperex Technology Co. Ltd., A123 Systems LLC, SK Innovation Co. Ltd., BYD Company Ltd., Hitachi, Samsung SDI Co. Ltd., Toshiba, Panasonic Corporation, Godrej Boyce, Exide Industries Limited, FIAMM, AMARONGrowth Accelerators

There are multiple factors contributing to the major growth of the next-generation advanced battery market. Primary among them is the high demand for electric vehicles (EVs). With governments worldwide promulgating stricter emission regulations and consumers being more conscious of the environment, the adoption of EVs is gaining momentum. High demand for EVs, in turn, necessitates batteries with increased energy density, fast-charging capabilities, and longer lifespans, thereby accelerating the development and deployment of next-generation batteries. Technology advancement is another major driver for the next-generation advanced battery market. Research and development are aimed at improving battery performance, safety, and cost. With advances in materials science, battery chemistry, and manufacturing processes, a new class of batteries is being developed that possesses better characteristics than conventional lithium-ion batteries. Solid-state batteries possess higher energy density and greater safety than the liquid electrolyte type. Thus, as our next-generation batteries evolve, their impact has enormous potential to change the energy landscape and propel sustainable development.Next-Generation Advanced Batteries Market Segmentation analysis

The Global Next-Generation Advanced Batteries is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Solid-state Batteries, Sodium-ion Batteries, Lithium-Sulfur Batteries, Metal-air Batteries, Flow Batteries . The Application segment categorizes the market based on its usage such as Energy Storage Systems, Electric Vehicles, Wearable Devices, Power Tools, Medical Devices. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive landscape of the next-generation advanced batteries market is dynamic and evolving, with the presence of established firms and innovative startups competing for market share. Established companies, such as LG Chem, Panasonic, and Samsung SDI, leverage their experience and resources to develop advanced battery technologies and expand production capabilities. They emphasise strategic partnerships, increased R&D investments, and scaling production to satisfy the growing demand for advanced batteries. In addition, many startups and research institutes are pushing innovation in next-generation batteries. Companies such as QuantumScape, Solid Power, and SES are exploring disruptive technologies, including solid-state batteries, lithium-sulphur batteries, and metal-air batteries. Considerable investment and partnership opportunities are offered to these companies as they try to commercialise their technologies and disrupt the market.Challenges In Next-Generation Advanced Batteries Market

Several hurdles exist against the wide adoption of next-generation advanced battery technologies. One major problem is the cost of these advanced batteries, which have sometimes been much higher than that of traditional lithium-ion batteries. Costly materials and complex processes are often involved in the development and manufacture of next-generation batteries, thus raising production costs. This typical monetary barrier stands squarely in the way of price competition for these batteries against existing technologies in price-sensitive markets. Technological maturity represents another major challenge that some next-generation battery technologies face. Although these batteries demonstrate tremendous potential in performance and safety, many of them are just beginning to enter the development phase. Various considerations, such as scalability, lifespan, and reliability, need to be addressed for commercialisation on a much larger scale. Surmounting these difficulties through continued research, development, and standardisation efforts will be crucial for the successful adoption of next-generation advanced batteries.Risks & Prospects in Next-Generation Advanced Batteries Market

The market for next-generation advanced batteries offers extensive growth opportunities from steadily rising demand for energy storage solutions for electric vehicles, renewable energy integration, and portable electronics. The entire concept of next-generation solid lithium-sulphur and sodium-ion batteries promises to yield higher energy density, fast charging, and improved safety over conventional lithium-ion solutions. All these factors, coupled together with government incentives and investments in clean energy schemes, are quickening the rate of the market's expansion as countries seek to cut their carbon emissions and switch to sustainable energy sources. One major opportunity that exists is with industrial and grid-scale applications for energy storage. A viable energy storage path is an emerging requirement to stabilise inefficient and intermittent renewable energy sources like solar and wind. A strong demand is building up for these batteries, which afford performance and long life, eco-friendliness. Those firms developing next-generation chemistries of longer life and lesser environmental impact will definitely stand to gain a competitive advantage in this constantly evolving market.Key Target Audience

The next-generation advanced batteries business is primarily directed toward electric vehicle (EV) manufacturers, renewable energy firms, and consumer electronics companies. EV manufacturers are constantly on the lookout for batteries with high energy density, fast charge times, and long life to ensure proper performance and range of their vehicles. Renewable energy firms need advanced batteries that will store any excess energy from solar, wind, or any other renewable energy generation so that the energy can be produced in a timely and reliable manner.,, Apart from the major target audience, the next-generation advanced batteries market also caters to various sectors such as aerospace, defence, and grid-scale energy storage. Aerospace and defence applications require batteries that feature extreme energy density, long life, and temperature extremes. Comprehending the needs and requirements of the various target audiences will assist companies within the next-generation advanced battery market to develop, innovate, and commercialise advanced battery technologies that suit the growing market demand.Merger and acquisition

Another newly noted trend encompasses mergers and acquisitions in the Next-Generation Advanced Batteries Market, encompassing endeavours that will enhance technological prowess and market positioning. A case in point includes Britishvolt's acquisition of EAS, an advanced battery cell innovator, for USD 36 million in May 2023. This step suggests that the industry is keenly aware of the need to secure advanced technology and raw material supply chains to develop next-generation battery solutions. Also lining this train in collaboration, Mercedes-Benz partners with ProLogium to hasten solid-state battery technology development; this serves as an idea of strategic alignment between the sectors of automobile and battery making to innovate and fulfil rising demands for electric vehicles. Collaboration is becoming the name of the game, as a number of major players, including Honeywell and FREYR Battery SA, have established a strategic alliance to bring next-generation battery cells to market, committing to major offtake agreements for energy storage applications through 2030. These partnerships are thus fuelling technological advancement and securing a stable supply chain against increasing competition in the market. >Analyst Comment

While the next-generation advanced battery market is burgeoning with growth due to the increasing demand for electric vehicles, renewable energy storage, and next-generation consumer electronics, these batteries have greater energy density, faster charging time levels, and longer lifecycles than traditional lithium-ion batteries, thus having applications on the widespread. The entire market is characterized by intense research and development, with companies and research institutions engaged in developing innovative battery technologies such as solid-state batteries, lithium-sulphur batteries, and sodium-ion batteries.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Next-Generation Advanced Batteries- Snapshot

- 2.2 Next-Generation Advanced Batteries- Segment Snapshot

- 2.3 Next-Generation Advanced Batteries- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Next-Generation Advanced Batteries Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Lithium-Sulfur Batteries

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Solid-state Batteries

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Sodium-ion Batteries

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Metal-air Batteries

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Flow Batteries

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

5: Next-Generation Advanced Batteries Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Electric Vehicles

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Energy Storage Systems

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Wearable Devices

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Power Tools

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Medical Devices

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

6: Next-Generation Advanced Batteries Market by Electrochemical System

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Aqueous-based Systems

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Non-aqueous-based Systems

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Solid-state Systems

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

7: Next-Generation Advanced Batteries Market by Manufacturing Technology

- 7.1 Overview

- 7.1.1 Market size and forecast

- 7.2 Battery Cell Manufacturing

- 7.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.2 Market size and forecast, by region

- 7.2.3 Market share analysis by country

- 7.3 Battery Pack Assembly

- 7.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.2 Market size and forecast, by region

- 7.3.3 Market share analysis by country

- 7.4 Battery Management System Integration

- 7.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.2 Market size and forecast, by region

- 7.4.3 Market share analysis by country

8: Next-Generation Advanced Batteries Market by End-User Industry

- 8.1 Overview

- 8.1.1 Market size and forecast

- 8.2 Automotive

- 8.2.1 Key market trends, factors driving growth, and opportunities

- 8.2.2 Market size and forecast, by region

- 8.2.3 Market share analysis by country

- 8.3 Industrial

- 8.3.1 Key market trends, factors driving growth, and opportunities

- 8.3.2 Market size and forecast, by region

- 8.3.3 Market share analysis by country

- 8.4 Consumer Electronics

- 8.4.1 Key market trends, factors driving growth, and opportunities

- 8.4.2 Market size and forecast, by region

- 8.4.3 Market share analysis by country

- 8.5 Healthcare

- 8.5.1 Key market trends, factors driving growth, and opportunities

- 8.5.2 Market size and forecast, by region

- 8.5.3 Market share analysis by country

- 8.6 Aerospace

- 8.6.1 Key market trends, factors driving growth, and opportunities

- 8.6.2 Market size and forecast, by region

- 8.6.3 Market share analysis by country

9: Next-Generation Advanced Batteries Market by Region

- 9.1 Overview

- 9.1.1 Market size and forecast By Region

- 9.2 North America

- 9.2.1 Key trends and opportunities

- 9.2.2 Market size and forecast, by Type

- 9.2.3 Market size and forecast, by Application

- 9.2.4 Market size and forecast, by country

- 9.2.4.1 United States

- 9.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 9.2.4.1.2 Market size and forecast, by Type

- 9.2.4.1.3 Market size and forecast, by Application

- 9.2.4.2 Canada

- 9.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 9.2.4.2.2 Market size and forecast, by Type

- 9.2.4.2.3 Market size and forecast, by Application

- 9.2.4.3 Mexico

- 9.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 9.2.4.3.2 Market size and forecast, by Type

- 9.2.4.3.3 Market size and forecast, by Application

- 9.2.4.1 United States

- 9.3 South America

- 9.3.1 Key trends and opportunities

- 9.3.2 Market size and forecast, by Type

- 9.3.3 Market size and forecast, by Application

- 9.3.4 Market size and forecast, by country

- 9.3.4.1 Brazil

- 9.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 9.3.4.1.2 Market size and forecast, by Type

- 9.3.4.1.3 Market size and forecast, by Application

- 9.3.4.2 Argentina

- 9.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 9.3.4.2.2 Market size and forecast, by Type

- 9.3.4.2.3 Market size and forecast, by Application

- 9.3.4.3 Chile

- 9.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 9.3.4.3.2 Market size and forecast, by Type

- 9.3.4.3.3 Market size and forecast, by Application

- 9.3.4.4 Rest of South America

- 9.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 9.3.4.4.2 Market size and forecast, by Type

- 9.3.4.4.3 Market size and forecast, by Application

- 9.3.4.1 Brazil

- 9.4 Europe

- 9.4.1 Key trends and opportunities

- 9.4.2 Market size and forecast, by Type

- 9.4.3 Market size and forecast, by Application

- 9.4.4 Market size and forecast, by country

- 9.4.4.1 Germany

- 9.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.1.2 Market size and forecast, by Type

- 9.4.4.1.3 Market size and forecast, by Application

- 9.4.4.2 France

- 9.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.2.2 Market size and forecast, by Type

- 9.4.4.2.3 Market size and forecast, by Application

- 9.4.4.3 Italy

- 9.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.3.2 Market size and forecast, by Type

- 9.4.4.3.3 Market size and forecast, by Application

- 9.4.4.4 United Kingdom

- 9.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.4.2 Market size and forecast, by Type

- 9.4.4.4.3 Market size and forecast, by Application

- 9.4.4.5 Benelux

- 9.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.5.2 Market size and forecast, by Type

- 9.4.4.5.3 Market size and forecast, by Application

- 9.4.4.6 Nordics

- 9.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.6.2 Market size and forecast, by Type

- 9.4.4.6.3 Market size and forecast, by Application

- 9.4.4.7 Rest of Europe

- 9.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 9.4.4.7.2 Market size and forecast, by Type

- 9.4.4.7.3 Market size and forecast, by Application

- 9.4.4.1 Germany

- 9.5 Asia Pacific

- 9.5.1 Key trends and opportunities

- 9.5.2 Market size and forecast, by Type

- 9.5.3 Market size and forecast, by Application

- 9.5.4 Market size and forecast, by country

- 9.5.4.1 China

- 9.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.1.2 Market size and forecast, by Type

- 9.5.4.1.3 Market size and forecast, by Application

- 9.5.4.2 Japan

- 9.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.2.2 Market size and forecast, by Type

- 9.5.4.2.3 Market size and forecast, by Application

- 9.5.4.3 India

- 9.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.3.2 Market size and forecast, by Type

- 9.5.4.3.3 Market size and forecast, by Application

- 9.5.4.4 South Korea

- 9.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.4.2 Market size and forecast, by Type

- 9.5.4.4.3 Market size and forecast, by Application

- 9.5.4.5 Australia

- 9.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.5.2 Market size and forecast, by Type

- 9.5.4.5.3 Market size and forecast, by Application

- 9.5.4.6 Southeast Asia

- 9.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.6.2 Market size and forecast, by Type

- 9.5.4.6.3 Market size and forecast, by Application

- 9.5.4.7 Rest of Asia-Pacific

- 9.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 9.5.4.7.2 Market size and forecast, by Type

- 9.5.4.7.3 Market size and forecast, by Application

- 9.5.4.1 China

- 9.6 MEA

- 9.6.1 Key trends and opportunities

- 9.6.2 Market size and forecast, by Type

- 9.6.3 Market size and forecast, by Application

- 9.6.4 Market size and forecast, by country

- 9.6.4.1 Middle East

- 9.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 9.6.4.1.2 Market size and forecast, by Type

- 9.6.4.1.3 Market size and forecast, by Application

- 9.6.4.2 Africa

- 9.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 9.6.4.2.2 Market size and forecast, by Type

- 9.6.4.2.3 Market size and forecast, by Application

- 9.6.4.1 Middle East

- 10.1 Overview

- 10.2 Key Winning Strategies

- 10.3 Top 10 Players: Product Mapping

- 10.4 Competitive Analysis Dashboard

- 10.5 Market Competition Heatmap

- 10.6 Leading Player Positions, 2022

11: Company Profiles

- 11.1 CATL

- 11.1.1 Company Overview

- 11.1.2 Key Executives

- 11.1.3 Company snapshot

- 11.1.4 Active Business Divisions

- 11.1.5 Product portfolio

- 11.1.6 Business performance

- 11.1.7 Major Strategic Initiatives and Developments

- 11.2 BYD Company Ltd.

- 11.2.1 Company Overview

- 11.2.2 Key Executives

- 11.2.3 Company snapshot

- 11.2.4 Active Business Divisions

- 11.2.5 Product portfolio

- 11.2.6 Business performance

- 11.2.7 Major Strategic Initiatives and Developments

- 11.3 SK Innovation Co. Ltd.

- 11.3.1 Company Overview

- 11.3.2 Key Executives

- 11.3.3 Company snapshot

- 11.3.4 Active Business Divisions

- 11.3.5 Product portfolio

- 11.3.6 Business performance

- 11.3.7 Major Strategic Initiatives and Developments

- 11.4 Hitachi

- 11.4.1 Company Overview

- 11.4.2 Key Executives

- 11.4.3 Company snapshot

- 11.4.4 Active Business Divisions

- 11.4.5 Product portfolio

- 11.4.6 Business performance

- 11.4.7 Major Strategic Initiatives and Developments

- 11.5 FIAMM

- 11.5.1 Company Overview

- 11.5.2 Key Executives

- 11.5.3 Company snapshot

- 11.5.4 Active Business Divisions

- 11.5.5 Product portfolio

- 11.5.6 Business performance

- 11.5.7 Major Strategic Initiatives and Developments

- 11.6 Samsung SDI Co. Ltd.

- 11.6.1 Company Overview

- 11.6.2 Key Executives

- 11.6.3 Company snapshot

- 11.6.4 Active Business Divisions

- 11.6.5 Product portfolio

- 11.6.6 Business performance

- 11.6.7 Major Strategic Initiatives and Developments

- 11.7 Contemporary Amperex Technology Co. Ltd.

- 11.7.1 Company Overview

- 11.7.2 Key Executives

- 11.7.3 Company snapshot

- 11.7.4 Active Business Divisions

- 11.7.5 Product portfolio

- 11.7.6 Business performance

- 11.7.7 Major Strategic Initiatives and Developments

- 11.8 LG Chem Ltd.

- 11.8.1 Company Overview

- 11.8.2 Key Executives

- 11.8.3 Company snapshot

- 11.8.4 Active Business Divisions

- 11.8.5 Product portfolio

- 11.8.6 Business performance

- 11.8.7 Major Strategic Initiatives and Developments

- 11.9 Panasonic Corporation

- 11.9.1 Company Overview

- 11.9.2 Key Executives

- 11.9.3 Company snapshot

- 11.9.4 Active Business Divisions

- 11.9.5 Product portfolio

- 11.9.6 Business performance

- 11.9.7 Major Strategic Initiatives and Developments

- 11.10 Toshiba

- 11.10.1 Company Overview

- 11.10.2 Key Executives

- 11.10.3 Company snapshot

- 11.10.4 Active Business Divisions

- 11.10.5 Product portfolio

- 11.10.6 Business performance

- 11.10.7 Major Strategic Initiatives and Developments

- 11.11 Exide Industries Limited

- 11.11.1 Company Overview

- 11.11.2 Key Executives

- 11.11.3 Company snapshot

- 11.11.4 Active Business Divisions

- 11.11.5 Product portfolio

- 11.11.6 Business performance

- 11.11.7 Major Strategic Initiatives and Developments

- 11.12 Godrej Boyce

- 11.12.1 Company Overview

- 11.12.2 Key Executives

- 11.12.3 Company snapshot

- 11.12.4 Active Business Divisions

- 11.12.5 Product portfolio

- 11.12.6 Business performance

- 11.12.7 Major Strategic Initiatives and Developments

- 11.13 A123 Systems LLC

- 11.13.1 Company Overview

- 11.13.2 Key Executives

- 11.13.3 Company snapshot

- 11.13.4 Active Business Divisions

- 11.13.5 Product portfolio

- 11.13.6 Business performance

- 11.13.7 Major Strategic Initiatives and Developments

- 11.14 AMARON

- 11.14.1 Company Overview

- 11.14.2 Key Executives

- 11.14.3 Company snapshot

- 11.14.4 Active Business Divisions

- 11.14.5 Product portfolio

- 11.14.6 Business performance

- 11.14.7 Major Strategic Initiatives and Developments

12: Analyst Perspective and Conclusion

- 12.1 Concluding Recommendations and Analysis

- 12.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Electrochemical System |

|

By Manufacturing Technology |

|

By End-User Industry |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Next-Generation Advanced Batteries in 2032?

+

-

Which type of Next-Generation Advanced Batteries is widely popular?

+

-

What is the growth rate of Next-Generation Advanced Batteries Market?

+

-

What are the latest trends influencing the Next-Generation Advanced Batteries Market?

+

-

Who are the key players in the Next-Generation Advanced Batteries Market?

+

-

How is the Next-Generation Advanced Batteries } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Next-Generation Advanced Batteries Market Study?

+

-

What geographic breakdown is available in Global Next-Generation Advanced Batteries Market Study?

+

-

Which region holds the second position by market share in the Next-Generation Advanced Batteries market?

+

-

Which region holds the highest growth rate in the Next-Generation Advanced Batteries market?

+

-