Global Portable-ultrasound-bladder-scanner Market Size, Share & Trends Analysis Report, Forecast Period, 2023-2030

Report ID: MS-2235 | Medical Devices | Last updated: Dec, 2024 | Formats*:

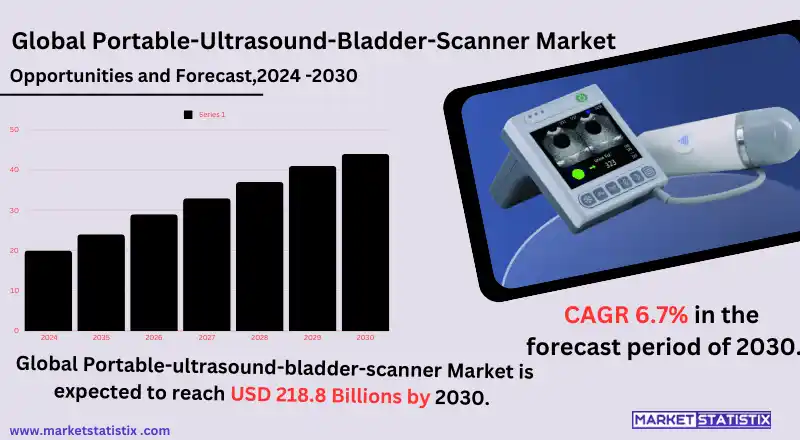

Portable-ultrasound-bladder-scanner Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 6.7% |

| Forecast Value (2030) | USD 218.8 Billion |

| By Product Type | 2D Portable Ultrasound Bladder Scanner, 3D Portable Ultrasound Bladder Scanner |

| Key Market Players |

|

| By Region |

|

Portable-ultrasound-bladder-scanner Market Trends

The portable ultrasound bladder scanner market has also grown out of a rising demand for efficient and non-invasive diagnostic instruments in healthcare facilities requiring fast and accurate bladder volume assessments that minimise catheterizations for improved patient comfort. Patient-centred care being promoted in the healthcare institution has found a good home for portable bladder scan devices within the hospital procedures, clinics, or home care setups. This has a bearing on the current trend of rising numbers of elderly people that come with their health challenges, including the increased incidences of urinary disorders, and require continual monitoring and management to drive market growth further. Among other dominating trends is the incorporation of sophisticated advanced technologies like artificial intelligence (AI) and cloud-based systems in portable ultrasound bladder scanners. These advancements improve the devices' accuracy and simplicity such that healthcare professionals can make faster and more informed decisions. Furthermore, the portability and the cost-effectiveness of these scanners make them a good option considering the willingness of healthcare facilities to cut the cost of operations and improve efficiency.Portable-ultrasound-bladder-scanner Market Leading Players

The key players profiled in the report are Becton Dickinson And Company, Carson, dBMEDx Inc, Vitacon, Laborie Medical Technologies, General Electric Company (GE Healthcare), Mcube Technology Co. Ltd, EchoNous, Patricia Industries (Laborie), Roper Technologies Inc. (Verathon), SRS Medical Systems Inc., OthersGrowth Accelerators

Furthermore, the portable ultrasound bladder scanners market is directly proportional to the increased demand for non-invasive, rapid, and accurate diagnostic tools for use in healthcare settings. These ultrasound systems allow medical professionals to examine bladder volume and partly diagnose urinary retention without the use of a catheter and allow for greater patient comfort and security. In addition, the increasing number of urinary disorders, mainly bladder retention, due to ageing and other chronic issues in many individuals, along with an increase in the number of outpatient care services, has contributed to propelling the demand for portable ultrasound bladder scanners as a more economic and efficient solution for diagnosis. New technologies around simple portability in ultrasound devices are another crucial market-driving factor. The rise of inexpensive, lightweight, and user-friendly devices has opened doorways through which these affordable options can reach hospitals, clinics, and home caregivers. These types of new innovations increase the simplicity of handling and portability for mobile assessments, which could lead to superior patient care and more efficient use of healthcare provider time.Portable-ultrasound-bladder-scanner Market Segmentation analysis

The Global Portable-ultrasound-bladder-scanner is segmented by Type, and Region. By Type, the market is divided into Distributed 2D Portable Ultrasound Bladder Scanner, 3D Portable Ultrasound Bladder Scanner . Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive scenario of the portable ultrasound bladder scanner market is mixed in the spotlight with both established and well-entrenched specialised innovators. Established companies like GE Healthcare, Philips Healthcare, and Siemens Healthineers dominate the market using their well-acknowledged history and strong brands, along with a wider distribution network and extended technological capabilities. These businesses aim mainly to launch a variety of high-quality portable ultrasound bladder scanners, mostly integrated with advanced types of imaging technology and easy-to-use features for healthcare providers seeking intelligent diagnostic solutions. Their market strategies include technological leadership and expansion of portfolios encouraging further demand for non-invasive, easy-to-use bladder scanning devices.Challenges In Portable-ultrasound-bladder-scanner Market

The portable ultrasound bladder scanner market holds a considerable challenge in terms of high start-up costs and minimal reimbursement policies in certain regions. While these devices facilitate non-invasive and convenient assessment of the bladder, the initial investment is a hindrance to many lower-scale healthcare facilities, especially those in developing markets. Further to this, because of the absence of insurance coverage or reimbursements for these devices in some countries, there are barriers to adoption, especially among healthcare providers that would rather not invest heavily into a facility perceived as making significant losses. Another complication is that an operator needs skills to handle the technology well. Although portable ultrasound bladder scanners are essentially made to be user-friendly, accurate results still come with proper training and experience, thus limiting their use in resource-poor environments where health professionals often lack the necessary training.Risks & Prospects in Portable-ultrasound-bladder-scanner Market

There are really great opportunities for using the portable ultrasound bladder scanner in the health care sector because many areas still have restricted access to health care services. These are the portable devices that would serve non-invasive and inexpensive diagnostics for bladder conditions of urinary retention, bladders not working properly, or complications after surgery. As health systems increasingly make requirements for diagnostics that can be accessed or done on the move, portable bladder scanners can be used anywhere—from emergency rooms through nursing homes to home care. Thus, an improvement in patient care and outcomes can be greatly facilitated with this form of technology. Technological advancements, such as improved images in compact designs with wireless capability, are also facilitating the market. The increase in the aged population, which is prone to bladder abnormalities, further supports the demanding need for portable ultrasound bladder scanners with increasing penetration of telemedicine and mobile health.Key Target Audience

The primary target for market portable ultrasound bladder scanners includes healthcare professionals, mainly in urology, nursing, and emergency medical services. They can be used by doctors, nurses, or any clinician to quickly assess bladder volume or find urinary retention or other issues before appropriate patient care management. This equipment is primarily adopted by hospitals, outpatient facilities, and long-term care centres because portable ultrasound bladder scanners provide a non-invasive, accurate, and user-friendly solution to enable diagnoses of urinary tract conditions but with no need for surgical procedures.,, Another important audience is home healthcare agencies and patients who have to monitor their bladder health at regular intervals, for example, those with prostate problems, spinal injuries, or neurological disorders. They are being very well used in rural or remote places where access to specialised medical equipment is very limited.Merger and acquisition

Emerging trends in portable ultrasound bladder scanner markets seem to reflect the trend of mergers and acquisitions, with companies in a race to advance their technology and widen market presence. This involved massive movement in February 2023, when GE HealthCare entered a deal to acquire Caption Health, an AI healthcare provider improving ultrasound diagnoses. Its main aim is to develop more portable ultrasound features, drawing advanced AI technologies into the portfolio, thus improving the diagnostic process. Apart from GE acquiring other companies, other companies are making their efforts to join the merger bandwagon to strengthen market sharing. Mindray introduced the TE Air Wireless Handheld Ultrasound in September 2023, unifying myriad advancement features related to portability for healthcare providers. It has continued to show steady growth prospects, providing estimates showing a market worth USD 188.8 million by 2034, propelled by rising urological conditions and point-of-care use. As competition heats up, market players such as Philips Healthcare and Laborie will likely continue to explore various strategic partnerships and acquisitions to strengthen their product offerings and penetrate more forces into this emerging market. >Analyst Comment

"The portable ultrasound bladder scanner market is now one of the fastest-growing segments in the medical devices market because of the increasing demand for non-invasive, accurate measurement of the bladder volume. These handheld devices employ ultrasound imaging technology to provide real-time images of the bladder, allowing the healthcare professional to evaluate bladder function and residual urine volume. The market for the end-users is directly driven by the increasing prevalence of urinary tract disorders, an older population seeking point-of-care diagnostics, cost-effective, space-saving point-of-care diagnostic devices, and emerging technologies. As technology evolves, portable ultrasound bladder scanners get smaller, easier to use, and less expensive, so more people have access to care."- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Portable-ultrasound-bladder-scanner- Snapshot

- 2.2 Portable-ultrasound-bladder-scanner- Segment Snapshot

- 2.3 Portable-ultrasound-bladder-scanner- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Portable-ultrasound-bladder-scanner Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 2D Portable Ultrasound Bladder Scanner

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 3D Portable Ultrasound Bladder Scanner

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Portable-ultrasound-bladder-scanner Market by End-user

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Hospitals

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Diagnostic Centers

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Clinics

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Ambulatory Surgical Centers

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

6: Portable-ultrasound-bladder-scanner Market by Distribution channel

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Online distribution channel

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Offline distribution channel

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

7: Portable-ultrasound-bladder-scanner Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 Becton Dickinson And Company

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Carson

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 dBMEDx Inc

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 Vitacon

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Laborie Medical Technologies

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 General Electric Company (GE Healthcare)

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 Mcube Technology Co. Ltd

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 EchoNous

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 Patricia Industries (Laborie)

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 Roper Technologies Inc. (Verathon)

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

- 9.11 SRS Medical Systems Inc.

- 9.11.1 Company Overview

- 9.11.2 Key Executives

- 9.11.3 Company snapshot

- 9.11.4 Active Business Divisions

- 9.11.5 Product portfolio

- 9.11.6 Business performance

- 9.11.7 Major Strategic Initiatives and Developments

- 9.12 Others

- 9.12.1 Company Overview

- 9.12.2 Key Executives

- 9.12.3 Company snapshot

- 9.12.4 Active Business Divisions

- 9.12.5 Product portfolio

- 9.12.6 Business performance

- 9.12.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By End-user |

|

By Distribution channel |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Portable-ultrasound-bladder-scanner in 2030?

+

-

How big is the Global Portable-ultrasound-bladder-scanner market?

+

-

How do regulatory policies impact the Portable-ultrasound-bladder-scanner Market?

+

-

What major players in Portable-ultrasound-bladder-scanner Market?

+

-

What applications are categorized in the Portable-ultrasound-bladder-scanner market study?

+

-

Which product types are examined in the Portable-ultrasound-bladder-scanner Market Study?

+

-

Which regions are expected to show the fastest growth in the Portable-ultrasound-bladder-scanner market?

+

-

What are the major growth drivers in the Portable-ultrasound-bladder-scanner market?

+

-

Is the study period of the Portable-ultrasound-bladder-scanner flexible or fixed?

+

-

How do economic factors influence the Portable-ultrasound-bladder-scanner market?

+

-