Global Radiopharmaceuticals in Nuclear Medicine Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2031

Report ID: MS-2046 | Healthcare and Pharma | Last updated: Nov, 2024 | Formats*:

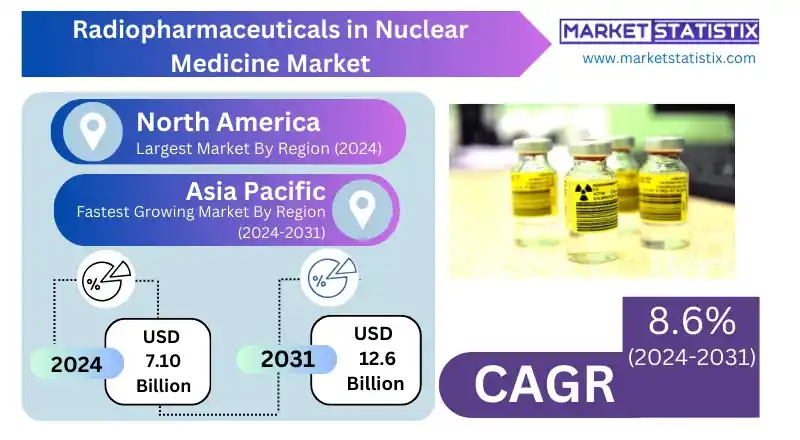

Radiopharmaceuticals in Nuclear Medicine Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 8.6% |

| By Product Type | Diagnostic Nuclear Medicine, Therapeutic Nuclear Medicine |

| Key Market Players |

|

| By Region |

|

Radiopharmaceuticals in Nuclear Medicine Market Trends

The nuclear medicine market for radiopharmaceuticals is in increased demand and growing rapidly as a result of improved imaging technologies coupled with their applications in oncology, cardiology, and neurology. Targeted therapy is one of the observed growing trends, especially regarding the treatment of cancers where radiopharmacology is used both in diagnosis and treatment. This paradigm shift towards targeted therapy is improving treatment compliance’s effectiveness but reducing the side effects therein, hence ensuring an increased utilisation of radiopharmaceuticals in clinical practice. Furthermore, new radiotracers as well as isotope development are widening the scope of nuclear medicine diagnostics, availing active and effective disease process identification and follow-up. As radiopharmaceuticals consistency in quality and availability has become more important, there has been a significant shift towards the production and supply chains of the radiopharmaceuticals. Furthermore, rising incidence of molecular imaging as well as hybridization techniques like PET/CT or SPECT/CT rapidly accelerates the market by allowing more detailed diagnostic information. These trends demonstrate how essential technology progress is to all actors in nuclear medicine the pharmaceutical industry, healthcare providers, and regulators in enhancing the system functioning of nuclear medicine and ultimately its ability to benefit patients.Radiopharmaceuticals in Nuclear Medicine Market Leading Players

The key players profiled in the report are Lantheus Holdings Inc., Life Molecular Imaging, Siemens Healthineers AG, Telix Pharmaceuticals Inc., Y-mAbs Therapeutics Inc., Curium Pharma, NorthStar Medical Radioisotopes LLC, Bracco S.p.A., Cardinal Health Inc., Progenics Pharmaceuticals Inc., Nordic Nanovector, Pharmova Limited, Mallinckrodt, Bayer AG,, GE Healthcare,, NTP Radioisotopes SOC Ltd., Jubilant, General Electric Company, Eckert & ZieglerGrowth Accelerators

The market for radiopharmaceutical products in nuclear medicine is highly reliant on the increasing incidences of oncological as well as cardiovascular diseases, which demands better diagnostic and treatment techniques. The increased focus on prevention-orientated and timely diagnosis in health care, especially cancer, has led to the creation of new radiopharmaceuticals with exceptional imaging capabilities. Moreover, the rising popularity of personalised medicine has also increased the attention on designing targeted and effective radiopharmaceuticals to improve treatment outcomes and reduce adverse effects. The growth in the demand for early diagnosis and better patient management by healthcare systems across the globe also continues to drive the growth of the radiopharmaceuticals market. Another contributing factor to the rise in demand for radiopharmaceuticals is the improvements in nuclear imaging systems, specifically positron emission tomography (PET) and single photon emission computed tomography (SPECT). These technologies boost the efficacy of radiopharmaceuticals, enabling users to scan for diseases and track their progress within the body. Supportive regulations as well as funding for research in nuclear medicine also play a major role in creating new possibilities and expanding the range of use of radiopharmaceuticals in different therapeutic areas, which ultimately improves the landscape of healthcare overall.Radiopharmaceuticals in Nuclear Medicine Market Segmentation analysis

The Global Radiopharmaceuticals in Nuclear Medicine is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Diagnostic Nuclear Medicine, Therapeutic Nuclear Medicine . The Application segment categorizes the market based on its usage such as Oncolog, Cardiology, Neurology, Endocrinology, Others. Geographically, the market is assessed across key Regions like North America(United States.Canada.Mexico), South America(Brazil.Argentina.Chile.Rest of South America), Europe(Germany.France.Italy.United Kingdom.Benelux.Nordics.Rest of Europe), Asia Pacific(China.Japan.India.South Korea.Australia.Southeast Asia.Rest of Asia-Pacific), MEA(Middle East.Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Challenges In Radiopharmaceuticals in Nuclear Medicine Market

The market for radiopharmaceuticals in nuclear medicine has to contend with quite a number of challenges, the most significant of which are related to the regulatory frameworks and the supply chain. First, the regulatory approval timelines for new radiopharmaceuticals tend to be long and complicated processes involving massive clinical trials to prove safety or efficacy, which in turn affects the time to market for new products, thus threatening growth and limiting available treatment and diagnostic solutions. Furthermore, the operationalization of such regulations, particularly with regard to the manufacture, use, and transport of radioactive materials, poses further burdens on the supply chain, making it impossible for producers to be on-off supply. The high cost of development and production of radiopharmaceuticals is another major issue that can preclude smaller companies from accessing the market and may also result in a lack of such products in developing economies. This is also because of the requirement of radioactive waste management, which is unclearly intensive and expensive, as well as the provision of specific plants and state-of-the art machinery. It is imperative to mitigate these barriers in order to scale up the use of radiopharmaceuticals so that they can continue to be useful in the practice of nuclear medicine today.Risks & Prospects in Radiopharmaceuticals in Nuclear Medicine Market

The nuclear medicine radiopharmaceuticals market is becoming more opportunistic as technological advancement faces imaging and a global increase of cancer and heart diseases. As far as most health systems are concerned, more emphasis is being put on early diagnosis and individualised healing; along with that, targeted therapy is in high demand, and the accuracy of the diagnosis is of great attention. Radiopharmaceuticals are used in diagnostic imaging and treatment, especially when it comes to cancers, by means of targeted radionuclide therapy. The growing acceptance and implementation of nuclear medicine techniques creates a need for the innovation of radiopharmaceuticals that can increase treatment rates and improve patient prognosis. Furthermore, the increase in the research and development of radiopharmaceuticals allows pharmaceutical partnering opportunities with other science-focused companies and national agencies. This is further enhanced by the rising nuclear medicine market plus the fact that the development of new radiopharmaceuticals concentrating on safety and sieving out the effective ones has reached convergence. In addition, growth in the use of radiopharmaceuticals for the purpose of imaging of and therapy with the use of radiopharmaceuticals in Alzheimer's disease is bringing new segments, thus adding to the growth.Key Target Audience

The primary focus of the radiopharmaceuticals market in nuclear medicine is on healthcare providers hospitals and diagnostic imaging centres that employ nuclear medicine for patients’ diagnosis and treatment as chief among them. Such establishments depend on a variety of radiopharmaceuticals for multiple of their services, including imaging and targeted treatment, more so in oncology, cardiology, and sometimes neurology. This is evident among specialists such as nuclear medicine physicians, residents, and oncologists who are routine custodians of radiopharmaceuticals due to their demand for high-quality imaging and treatment techniques, which results in enhanced healthcare services.,, Pharmaceutical organizations and research departments, who develop and manufacture radiopharmaceuticals, are also an important audience. This segment is concerned with the improvement of this technology, e.g., radiopharmaceutical production and new isotope discovery. Moreover, the agencies and the governments are also important audiences since they ensure that these products are approved and safe for use in clinical practice.Merger and acquisition

The dynamics of the radiopharmaceuticals market in recent history have been chiefly characterised by the growth of M&As, which underscores the increasing demand for targeted therapies for cancer treatment. For instance, AstraZeneca disclosed that it was going to acquire Fusion Pharmaceuticals for an amount reaching up to 2.4 billion dollars, a figure that represents a premium on Fusion’s shares. This acquisition is also significant as it shows that AstraZeneca seeks to pursue the effectiveness of radiopharmaceuticals in cancer treatment, especially after the success of Novartis’ prostate cancer medicine, Pluvicto. The acquisition gives AstraZeneca an opportunity to expand its resources for producing and distributing these complex medications, which are considered suitable options in place of radiation therapy. Moreover, Bristol Myers Squibb managed to finalise the RayzeBio acquisition for about 4.1 billion dollars, which features a victorious pipeline of actinium-based solid malignancy-focused radiopharmaceutical development. This acquisition also extends the BMS oncological range, enabling the company to outstrip an active position in the burgeoning radiopharmaceutical market. In another deal, Telix Pharmaceuticals also announced that it will acquire RLS (USA) Inc. for up to $250 million to bolster its distribution and manufacturing capabilities within the country. These deals follow the trend of consolidation among leading companies in an effort to harness the power of radioligands in the treatment of cancers.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Radiopharmaceuticals in Nuclear Medicine- Snapshot

- 2.2 Radiopharmaceuticals in Nuclear Medicine- Segment Snapshot

- 2.3 Radiopharmaceuticals in Nuclear Medicine- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Radiopharmaceuticals in Nuclear Medicine Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Diagnostic Nuclear Medicine

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Therapeutic Nuclear Medicine

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Radiopharmaceuticals in Nuclear Medicine Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Oncolog

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Cardiology

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Neurology

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Endocrinology

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Others

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

6: Radiopharmaceuticals in Nuclear Medicine Market by End User

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Hospitals

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Ambulatory Surgical Centers

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Specialty Clinics

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Diagnostic Centers

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

- 6.6 Others

- 6.6.1 Key market trends, factors driving growth, and opportunities

- 6.6.2 Market size and forecast, by region

- 6.6.3 Market share analysis by country

7: Radiopharmaceuticals in Nuclear Medicine Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 Lantheus Holdings Inc.

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Life Molecular Imaging

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 Siemens Healthineers AG

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 Telix Pharmaceuticals Inc.

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Y-mAbs Therapeutics Inc.

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 Curium Pharma

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 NorthStar Medical Radioisotopes LLC

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 Bracco S.p.A.

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 Cardinal Health Inc.

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 Progenics Pharmaceuticals Inc.

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

- 9.11 Nordic Nanovector

- 9.11.1 Company Overview

- 9.11.2 Key Executives

- 9.11.3 Company snapshot

- 9.11.4 Active Business Divisions

- 9.11.5 Product portfolio

- 9.11.6 Business performance

- 9.11.7 Major Strategic Initiatives and Developments

- 9.12 Pharmova Limited

- 9.12.1 Company Overview

- 9.12.2 Key Executives

- 9.12.3 Company snapshot

- 9.12.4 Active Business Divisions

- 9.12.5 Product portfolio

- 9.12.6 Business performance

- 9.12.7 Major Strategic Initiatives and Developments

- 9.13 Mallinckrodt

- 9.13.1 Company Overview

- 9.13.2 Key Executives

- 9.13.3 Company snapshot

- 9.13.4 Active Business Divisions

- 9.13.5 Product portfolio

- 9.13.6 Business performance

- 9.13.7 Major Strategic Initiatives and Developments

- 9.14 Bayer AG

- 9.14.1 Company Overview

- 9.14.2 Key Executives

- 9.14.3 Company snapshot

- 9.14.4 Active Business Divisions

- 9.14.5 Product portfolio

- 9.14.6 Business performance

- 9.14.7 Major Strategic Initiatives and Developments

- 9.15

- 9.15.1 Company Overview

- 9.15.2 Key Executives

- 9.15.3 Company snapshot

- 9.15.4 Active Business Divisions

- 9.15.5 Product portfolio

- 9.15.6 Business performance

- 9.15.7 Major Strategic Initiatives and Developments

- 9.16 GE Healthcare

- 9.16.1 Company Overview

- 9.16.2 Key Executives

- 9.16.3 Company snapshot

- 9.16.4 Active Business Divisions

- 9.16.5 Product portfolio

- 9.16.6 Business performance

- 9.16.7 Major Strategic Initiatives and Developments

- 9.17

- 9.17.1 Company Overview

- 9.17.2 Key Executives

- 9.17.3 Company snapshot

- 9.17.4 Active Business Divisions

- 9.17.5 Product portfolio

- 9.17.6 Business performance

- 9.17.7 Major Strategic Initiatives and Developments

- 9.18 NTP Radioisotopes SOC Ltd.

- 9.18.1 Company Overview

- 9.18.2 Key Executives

- 9.18.3 Company snapshot

- 9.18.4 Active Business Divisions

- 9.18.5 Product portfolio

- 9.18.6 Business performance

- 9.18.7 Major Strategic Initiatives and Developments

- 9.19 Jubilant

- 9.19.1 Company Overview

- 9.19.2 Key Executives

- 9.19.3 Company snapshot

- 9.19.4 Active Business Divisions

- 9.19.5 Product portfolio

- 9.19.6 Business performance

- 9.19.7 Major Strategic Initiatives and Developments

- 9.20 General Electric Company

- 9.20.1 Company Overview

- 9.20.2 Key Executives

- 9.20.3 Company snapshot

- 9.20.4 Active Business Divisions

- 9.20.5 Product portfolio

- 9.20.6 Business performance

- 9.20.7 Major Strategic Initiatives and Developments

- 9.21 Eckert & Ziegler

- 9.21.1 Company Overview

- 9.21.2 Key Executives

- 9.21.3 Company snapshot

- 9.21.4 Active Business Divisions

- 9.21.5 Product portfolio

- 9.21.6 Business performance

- 9.21.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By End User |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the growth rate of Radiopharmaceuticals in Nuclear Medicine Market?

+

-

What are the latest trends influencing the Radiopharmaceuticals in Nuclear Medicine Market?

+

-

Who are the key players in the Radiopharmaceuticals in Nuclear Medicine Market?

+

-

How is the Radiopharmaceuticals in Nuclear Medicine } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Radiopharmaceuticals in Nuclear Medicine Market Study?

+

-

What geographic breakdown is available in Global Radiopharmaceuticals in Nuclear Medicine Market Study?

+

-

Which region holds the second position by market share in the Radiopharmaceuticals in Nuclear Medicine market?

+

-

How are the key players in the Radiopharmaceuticals in Nuclear Medicine market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Radiopharmaceuticals in Nuclear Medicine market?

+

-

What are the major challenges faced by the Radiopharmaceuticals in Nuclear Medicine Market?

+

-