Global Scale Inhibitors Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-1846 | Chemicals And Materials | Last updated: Sep, 2024 | Formats*:

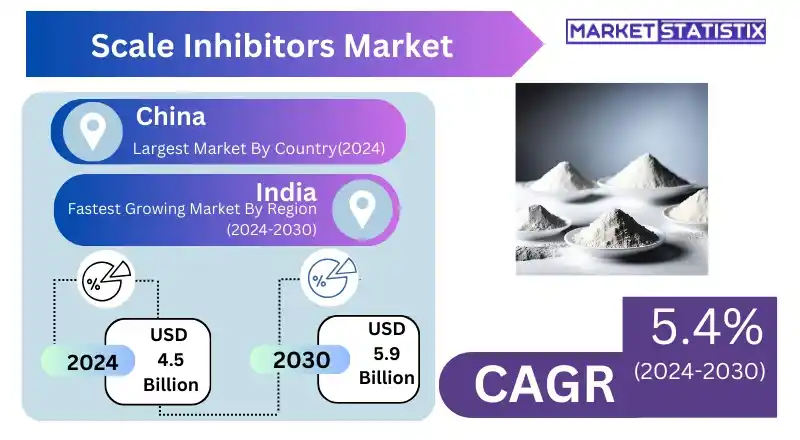

Scale Inhibitors Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 5.4% |

| By Product Type | Phosphonates, Carboxyates/Carbonates, Sulfonates, Fluorides, Other Types |

| Key Market Players |

|

| By Region |

|

Scale Inhibitors Market Trends

Because of its growing popularity in the oil industry, in addition to power generation and water treatment, the scale inhibitor market is booming. One prominent subject of discussion involves the need to guarantee that water does not get contaminated with minerals as it passes through human structures and other equipment. As these companies try to increase their output levels while minimising downtime associated with scaling processes, advanced scale inhibition techniques are gaining acceptance, especially in places where water is scarce. Also important are movements toward eco-friendly or biodegradable types of materials due to growing environmental regulations and sustainability issues. For example, individual businesses are investing heavily into their researchers’ laboratories, helping them to come up with better kinds that will not only help people but also maintain their functionality. There is a strong likelihood that fresh and green-scale inhibitors would be in great demand since proper industry management involves efficiency and environmental compatibility.Scale Inhibitors Market Leading Players

The key players profiled in the report are BASF SE (Germany), Dow (US), Clariant (Switzerland), Syensqo (Belgium), Ecolab (US), Kurita Water Industries Ltd. (Japan), Solenis (US), Veolia (France), Kemira (Finland), Italmatch Chemicals S.p.A. (Italy)Growth Accelerators

The demand that drives the growth of scale inhibitors is mainly influenced by increased consumption from oil and gas, electricity production, and wastewater management industries. These sectors heavily depend on these substances in order to reduce mineral deposits that may cause damage to their machines, decrease their efficiency, and make them incur losses due to time wasted when equipment is down. The increasing pace of industrialisation along with the increasing need for effective water management systems has led to a rise in demand for scale inhibitors; this trend is more pronounced, particularly in the dry areas where there are other problems like water hardness. Furthermore, this needs for pipeline, well, and equipment protection from scaling in the oil and gas sector, mainly influenced by offshore drilling activities and enhanced oil recovery techniques, has also contributed significantly towards the use of these agents. In addition, there have been developments concerning technological advances as well as novel scale inhibitor formulations that lead to improved effectiveness while being environmentally friendly, thus pushing growth in this market forward. As industries increasingly strive to be cost-effective and reduce maintenance costs, demand for scale inhibitors is likely to rise.Scale Inhibitors Market Segmentation analysis

The Global Scale Inhibitors is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Phosphonates, Carboxyates/Carbonates, Sulfonates, Fluorides, Other Types . The Application segment categorizes the market based on its usage such as Power and construction, Oil & gas, Mining, Municipal water treatment & desalination, Food & beverage, Chemical & pharmaceutical, Pulp & paper, Other applications. Geographically, the market is assessed across key Regions like North America(United States.Canada.Mexico), South America(Brazil.Argentina.Chile.Rest of South America), Europe(Germany.France.Italy.United Kingdom.Benelux.Nordics.Rest of Europe), Asia Pacific(China.Japan.India.South Korea.Australia.Southeast Asia.Rest of Asia-Pacific), MEA(Middle East.Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The scale inhibitors market is very competitive and has several main companies, both regional and global, involved in it, which include large manufacturers of chemicals as well as speciality chemical companies. Industrial giants such as BASF SE, Dow Chemical Company, and Solvay have been producing advanced-scale inhibitors for the oil and gas industry, water treatment, and power generation and still supply them to those sectors. They enhance their position by means of product improvement and collaboration with other stakeholders. Smaller players also significantly contribute to this sector by providing tailored solutions for niche marketing or region-specific demands. Numerous players are competing for customers in this sector; hence, the firms are consistently investing in research as well as advancement initiatives aimed at improving the effectiveness of scale inhibitors while adhering to ecologically acceptable levels. The battle for market share among firms selling cheap yet efficient scale inhibitors shall continue since they will always look for innovative ways of preventing precipitation from occurring inside machines or pipes used in various industries.Challenges In Scale Inhibitors Market

Raw materials’ fluctuating prices and availability represent the major challenges facing the scale inhibitor market. A majority of scale inhibitors originate from petrochemical products, thereby subjecting production costs to any oil and gas sector volatility. Such price instability might limit the manufacturer’s ability to offer competitive pricing, especially in industries sensitive to costs like water treatment and oil extraction, thus affecting their profitability. Corrupt practices of chemical-based scale inhibitors compound the problem with more stringent environmental regulations being introduced by various governments. Phosphate, a key ingredient in traditional inhibiting agents or other harmful products, has been linked to pollution of water bodies, among other things. Therefore, there is an increased pressure on manufacturers to come up with eco-friendly and biodegradable scale inhibitors as many industries adopt greener substitutes; however, this entails large investments into research and development whose returns are not immediate, adding complexity into trade dynamics.Risks & Prospects in Scale Inhibitors Market

The scale inhibitor market has ample chances, which come from the increasing need for good water treatment solutions in sectors including oil & gas, power generation, and manufacturing. As these industries encounter the problems associated with scaling in pipes, boilers, and cooling towers, there is a growing need for scale inhibitors that prevent the formation of mineral deposits. The rising use of enhanced oil recovery techniques as well as the expansion of power plants, particularly in developing countries, contribute to the demand for advanced scale inhibition technologies. The rising interest in sustainable green chemistry also offers a platform for research on green scale inhibitors. Biodegradable and less toxic scale inhibitors are being developed due to environmental regulations that discourage harmful chemicals. Municipal councils want industries’ water treatment solutions to be effective yet eco-friendly; hence, they are likely to buy them from companies that engage in research meant to create such products.Key Target Audience

The scale inhibitors market primarily targets industries that are largely reliant on water-based processes like oil and gas, power generation, and chemical manufacturing. These industries apply scale inhibitors for the purpose of hindering accumulation of mineral deposits in pipelines, boilers, and cooling systems so as to ensure smooth functioning of machinery alongside reducing maintenance costs. Hence, they are crucial in enhancing efficiency levels and extending the life span of industrial machines.,, Another important group of customers consists of water treatment facilities as well as utility companies that require the use of scale inhibitors to control hardness in water and avoid scaling within municipal waters. In their efforts to safeguard the quality of their water supplies from impurities caused by mineral deposits, these organisations have found use for scale inhibitors. As a result, there is a growing demand for more effective solutions for water treatment both at industrial levels and municipalities, leading to an increase in sales volume within this segment since it is driven by operational efficiency improvements and equipment upkeep needs.Merger and acquisition

Recent mergers and acquisitions (M&A) activity in the scale inhibitors market is a sign of a broader trend where companies are consolidating strategically so as to improve their technological capabilities and expand their market reach. Companies have been buying smaller players that offer innovative solutions in water treatment, oil, and gas, as well as industrial application areas, which are key sectors driving demand for scale inhibitors. These deals usually focus on the incorporation of advanced chemical formulations and sustainable products that meet the growing need for cost-effective, eco-friendly scale management options. For instance, among the recent transactions is an acquisition under the oil and gas sector with the aim of streamlining operations while enhancing performance via improved implementation of scale inhibitor technologies. In addition, some leading chemical producers have purchased niche companies over the last year to strengthen their presence in fast-growing regions like Asia Pacific or the Middle East (2023). The deals are designed to enhance product lines with new control solutions for the scaling problem facing such industries as power generation and water treatment. In turn, this will cause increased growth opportunities within these markets that would eventually lead to enhanced competition among them soon enough. >Analyst Comment

"The global scale inhibitors market is experiencing steady growth, driven by the increasing demand for efficient and reliable industrial processes. The scale inhibitors are very important in preventing the formation of the scales, which would have otherwise reduced efficiency, cause high maintenance costs, or cause equipment damage in some instances. In this aspect, there is a wide diversity of products available on the market that differ in their chemical composition, application method, and effectiveness. Some of the factors causing an increase in demand include industrialisation, urbanisation, and advancements in technology, as well as a focus on sustainability through energy efficiency. With a steady rise in demand for more efficient and reliable industrial processes, the scale inhibitors market will continue to remain dynamic and competitive by introducing new product innovations and applications that meet the changing needs of different sectors."- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Scale Inhibitors- Snapshot

- 2.2 Scale Inhibitors- Segment Snapshot

- 2.3 Scale Inhibitors- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Scale Inhibitors Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Phosphonates

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Carboxyates/Carbonates

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Sulfonates

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Fluorides

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Other Types

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

5: Scale Inhibitors Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Power and construction

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Oil & gas

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Mining

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Municipal water treatment & desalination

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Food & beverage

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

- 5.7 Chemical & pharmaceutical

- 5.7.1 Key market trends, factors driving growth, and opportunities

- 5.7.2 Market size and forecast, by region

- 5.7.3 Market share analysis by country

- 5.8 Pulp & paper

- 5.8.1 Key market trends, factors driving growth, and opportunities

- 5.8.2 Market size and forecast, by region

- 5.8.3 Market share analysis by country

- 5.9 Other applications

- 5.9.1 Key market trends, factors driving growth, and opportunities

- 5.9.2 Market size and forecast, by region

- 5.9.3 Market share analysis by country

6: Scale Inhibitors Market by Product Type

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Threshold inhibitors

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Crystal modification

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Dispersion

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Other process types

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

7: Scale Inhibitors Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 BASF SE (Germany)

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Dow (US)

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 Clariant (Switzerland)

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 Syensqo (Belgium)

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Ecolab (US)

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 Kurita Water Industries Ltd. (Japan)

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 Solenis (US)

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 Veolia (France)

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 Kemira (Finland)

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 Italmatch Chemicals S.p.A. (Italy)

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By Product Type |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the growth rate of Scale Inhibitors Market?

+

-

What are the latest trends influencing the Scale Inhibitors Market?

+

-

Who are the key players in the Scale Inhibitors Market?

+

-

How is the Scale Inhibitors } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Scale Inhibitors Market Study?

+

-

What geographic breakdown is available in Global Scale Inhibitors Market Study?

+

-

How are the key players in the Scale Inhibitors market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Scale Inhibitors market?

+

-

What are the major challenges faced by the Scale Inhibitors Market?

+

-

What is the list of players included in the research coverage of the Scale Inhibitors Market Study?

+

-