Global Sterilization Pouch Market – Industry Trends and Forecast to 2031

Report ID: MS-1835 | Healthcare and Pharma | Last updated: Sep, 2024 | Formats*:

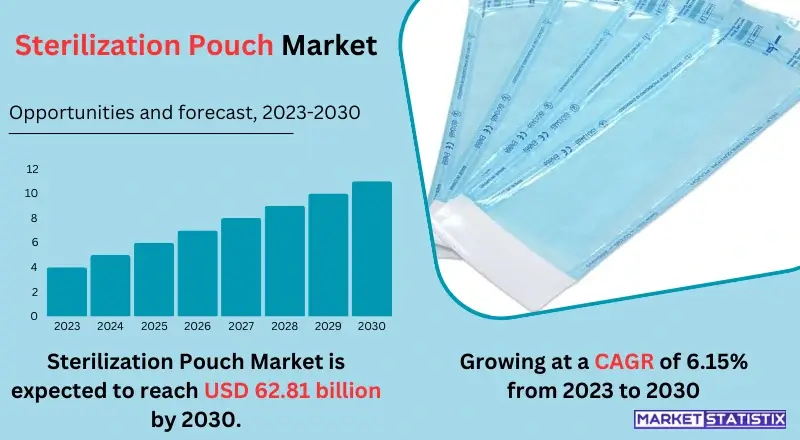

Sterilization Pouch Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2031 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 6.15% |

| By Product Type | Sterilization Pouches, Sterilization Wrapping, Sterilization Containers, Others |

| Key Market Players |

|

| By Region |

|

Sterilization Pouch Market Trends

The sterilisation pouch market is experiencing increasing demand for infection control and patient safety, thus attracting several notable trends in the industry. Sterilisation pouches are important for maintaining high levels of hygiene and preventing cross-contamination as they pack medical instruments or devices to ensure they remain sterile until used. In addition, there is also an increase in the use of advanced materials like medical-grade plastics or barrier films, which improve these pouches’ durability and effectiveness. The main trends driving the market include a growing focus on healthcare facility safety, particularly with stringent infection control regulations. Another trend associated with this is the increasing use of eco-friendly and biodegradable sterilisation pouches as part of wider sustainability efforts. Therefore, as concerns over security and environment continue to shape healthcare practices, demand for sterilisation pouches will rise accordingly.Sterilization Pouch Market Leading Players

The key players profiled in the report are 3M (US), Dynarex Corporation (US), PMS Healthcare Technologies (US), Getinge Group (Sweden), Smurfit Kappa (Ireland), STERIS (Ireland), Certol International (US), Bischof+Klein (Germany), Wihuri (China), Cardinal Health (US), Amcor plc (Australia), Mondi Group (Austria), Berry Global (US), YIPAK (China), Cantel Medical Co. (US), AMD Medicom Inc. (Canada), STERIMED (US), Shanghai Jianzhong Medical Equipment Packing Co., Ltd. (China), Proampac (US), OthersGrowth Accelerators

The rising demand for infection management and sanitation in hospitals or healthcare centres builds the market for sterilisation pouches. Sterilisation pouches are basic to maintain sterility in instruments and devices used in medicine, especially for hospitals, clinics, and laboratories. Healthcare-associated infections (HAIs) have brought about this surge in demand as healthcare providers seek patient safety while meeting strict regulations on infection control. Moreover, other factors driving growth in this sector are advancements in medical technology, an increasing number of surgeries performed, and the expansion of health infrastructure in developing countries, thereby pushing up demand for sterilisation pouch products. Market growth is further fuelled by trends such as the transition towards disposable medical products, rising concerns over cross-contamination, and packaging solutions that are both affordable and reliable. The market for sterilisation pouches is likely to grow steadily as hospitals continue to make infection control a priority.Sterilization Pouch Market Segmentation analysis

The Global Sterilization Pouch is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Sterilization Pouches, Sterilization Wrapping, Sterilization Containers, Others . The Application segment categorizes the market based on its usage such as Hospitals, CSSDs, Clinics, Others. Geographically, the market is assessed across key Regions like North America(United States.Canada.Mexico), South America(Brazil.Argentina.Chile.Rest of South America), Europe(Germany.France.Italy.United Kingdom.Benelux.Nordics.Rest of Europe), Asia Pacific(China.Japan.India.South Korea.Australia.Southeast Asia.Rest of Asia-Pacific), MEA(Middle East.Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The sterilisation pouch industry exhibits a competitive environment whereby well-established medical packaging firms as well as sterilisation pouch manufacturing specialists coexist amicably. Among these market leaders are Berry Global, Sealed Air DuPont, and Berry Plastics, who provide all manners of sterilisation pouches used in different medical sectors. Their hold on the market can be traced back to their proficiency, production capabilities, and distribution channels. Besides the big players, there are also many smaller, specialised companies that develop and manufacture advanced sterilisation pouch technologies. Such firms contribute to the general vibrancy and heterogeneity of this industry due to their distinctive products offered at competitive prices in many cases.Challenges In Sterilization Pouch Market

Experts in this field say that sterilisation pouch companies must innovate constantly, and they have to comply with increasingly strict rules. This happens because antibiotic treatments are becoming more powerful every day and hence need increasingly safe ways of transmitting them into body systems where they can function properly. As a result, approval timeframes for new products may become longer while adherence costs go up. Maintaining quality and fulfilling these specifications is not an easy task for manufacturers. Another issue causing consumer packaging manufacturers problems remains alternative options available that can either reduce or eliminate such pouches altogether. In addition, other innovators, such as researchers who specialise in sterilisation processes, may also compete with traditional products’ characteristics. Therefore, organisations need to be aware of technological improvements so that they can remain competitive in terms of product or service delivery. Costs versus benefits remain vital aspects guiding expansion within the sterilisation pouch sector.Risks & Prospects in Sterilization Pouch Market

The market for sterilisation pouches is full of possible chances because the demand for infection prevention and control, together with sterile packaging systems, has steadily grown among healthcare and medical sectors. Sterilisation pouches play an important role in protecting the sterility of medical instruments as well as supplies when they are kept or transported. The rise in healthcare procedures and surgeries and the need for stringent infection control practices have created a demand for high-quality sterilisation pouches that facilitate safe and effective sterilisation of medical instruments. Moreover, emerging markets’ developing healthcare infrastructures, together with the increasing knowledge on prevention and control of infections, offer opportunities for growth for manufacturers of sterilisation pouches. With hospitals putting more emphasis on security and efficiency during these processes, there will be an increase in market size for such products due to global innovations or more investment in health care systems.Key Target Audience

Among the primary target groups of the sterilisation pouch market are healthcare institutions such as hospitals, clinics, and dental offices that need sterilised tools and equipment for medical procedures. These pouches are crucial for keeping surgical instruments, medical devices, and laboratory equipment sterile. Moreover, manufacturers of medical devices as well as sterilisation service providers in search of acceptable packing options to guarantee product safety and efficiency during storage and transportation are also target markets.,, Furthermore, pharmaceutical companies along with laboratories have a vested interest in this industry because they rely heavily on contamination prevention measures. Regulatory authorities and certification organisations do have their part in the industry by establishing standards for disinfection processes to follow, thus ensuring adherence to regulations concerning them and avoiding dangers posed by non-compliance with those rules. Aspirations for controlling infections keeping on escalating within health institutions inform the expansion of the sterilisation pouch market since it requires reliable sterilisation solutions across diverse sectors.Merger and acquisition

Recent mergers and acquisitions within the sterilisation pouch market illustrate strategic growth and consolidation in the industry, spurred by a rise in demand prevalent across healthcare and hygiene-related segments. 3M, Berry Global, and Amcor plc, among others, have been taking over smaller companies or merging with similar players to widen their product range as well as enhance their global visibility. These initiatives are meant to benefit from the increasing importance given to sterilisation solutions due to people wanting safer medical packaging. The competitive environment is also changing through strategic partnerships and collaborations. For example, there are companies that enter into joint ventures so as to manufacture modern sterilisation products that meet international regulatory requirements. This trend enables market leaders to provide integrated solutions for hospitals, clinics, and other health care establishments, meeting heightened concerns about infection control and patient safety.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Sterilization Pouch- Snapshot

- 2.2 Sterilization Pouch- Segment Snapshot

- 2.3 Sterilization Pouch- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Sterilization Pouch Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Sterilization Pouches

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Sterilization Wrapping

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Sterilization Containers

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Others

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

5: Sterilization Pouch Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Hospitals

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 CSSDs

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Clinics

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Others

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

6: Sterilization Pouch Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 3M (US)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Dynarex Corporation (US)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 PMS Healthcare Technologies (US)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Getinge Group (Sweden)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Smurfit Kappa (Ireland)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 STERIS (Ireland)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Certol International (US)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Bischof+Klein (Germany)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Wihuri (China)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Cardinal Health (US)

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Amcor plc (Australia)

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Mondi Group (Austria)

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Berry Global (US)

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 YIPAK (China)

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Cantel Medical Co. (US)

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 AMD Medicom Inc. (Canada)

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 STERIMED (US)

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

- 8.18 Shanghai Jianzhong Medical Equipment Packing Co.

- 8.18.1 Company Overview

- 8.18.2 Key Executives

- 8.18.3 Company snapshot

- 8.18.4 Active Business Divisions

- 8.18.5 Product portfolio

- 8.18.6 Business performance

- 8.18.7 Major Strategic Initiatives and Developments

- 8.19 Ltd. (China)

- 8.19.1 Company Overview

- 8.19.2 Key Executives

- 8.19.3 Company snapshot

- 8.19.4 Active Business Divisions

- 8.19.5 Product portfolio

- 8.19.6 Business performance

- 8.19.7 Major Strategic Initiatives and Developments

- 8.20 Proampac (US)

- 8.20.1 Company Overview

- 8.20.2 Key Executives

- 8.20.3 Company snapshot

- 8.20.4 Active Business Divisions

- 8.20.5 Product portfolio

- 8.20.6 Business performance

- 8.20.7 Major Strategic Initiatives and Developments

- 8.21 Others

- 8.21.1 Company Overview

- 8.21.2 Key Executives

- 8.21.3 Company snapshot

- 8.21.4 Active Business Divisions

- 8.21.5 Product portfolio

- 8.21.6 Business performance

- 8.21.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

Which application type is expected to remain the largest segment in the Global Sterilization Pouch market?

+

-

How do regulatory policies impact the Sterilization Pouch Market?

+

-

What major players in Sterilization Pouch Market?

+

-

What applications are categorized in the Sterilization Pouch market study?

+

-

Which product types are examined in the Sterilization Pouch Market Study?

+

-

Which regions are expected to show the fastest growth in the Sterilization Pouch market?

+

-

What are the major growth drivers in the Sterilization Pouch market?

+

-

Is the study period of the Sterilization Pouch flexible or fixed?

+

-

How do economic factors influence the Sterilization Pouch market?

+

-

How does the supply chain affect the Sterilization Pouch Market?

+

-