Global Telecom Billing and Revenue Market Size, Share & Trends Analysis Report, Forecast Period, 2023-2030

Report ID: MS-2157 | Application Software | Last updated: Dec, 2024 | Formats*:

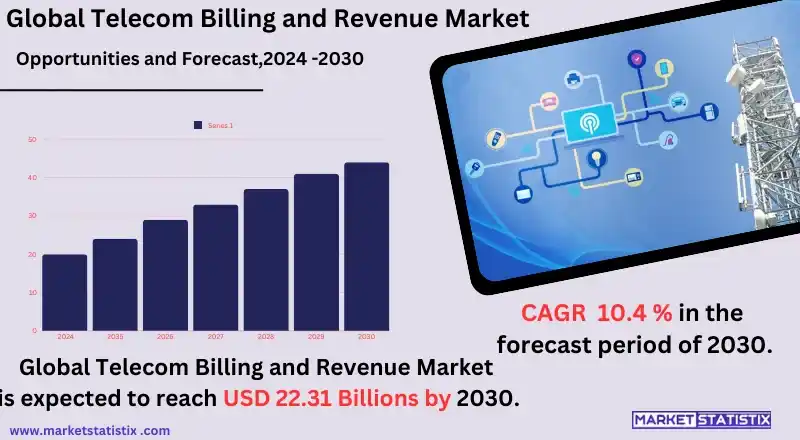

Telecom Billing and Revenue Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 10.4% |

| Forecast Value (2030) | USD 22.31 Billion |

| By Product Type | Mobile Operators, Internet Service Providers |

| Key Market Players |

|

| By Region |

|

Telecom Billing and Revenue Market Trends

The worldwide market for telecom billing and revenue systems is also shifting, gradually embracing new technologies, especially cloud-based systems. More and more telecom companies are leaving traditional on-premises charging systems and moving to more efficient and flexible cloud-computing billing systems. This helps operators to optimize their processes, cut their expenses, and improve the systems’ effectiveness in terms of volume and diversification of the billing operations. Cloud computing solutions, furthermore, support real-time billing, which is a key requirement when managing subscription-based services, integrating price plans and packages, or rendering services with more complex delivery models, enhancing customer satisfaction. Moreover, the other significant trend in the telecommunications billing and revenue assurance market is the deployment of billing management, revenue assurance, and other business process systems that incorporate artificial intelligence, machine learning, and automation. These solutions are particularly important to telecom firms in boosting revenue, fraud risk mitigation, and enhancing marketing targeting. Telecommunication operators are also focusing on implementing billing systems that will support complicated pricing and new ways of making money, like IoT services or 5G applications, due to the most recent development of 5G networks and the growing desire for data. Thus, the market bears more fruits of inventions.Telecom Billing and Revenue Market Leading Players

The key players profiled in the report are Amdocs, Cerillion Technologies Ltd, Comarch SA, CSG Systems, Inc., Formula Telecom Solutions Ltd, Oracle, SAP SE, STL Tech, SUBEX, Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd, Intracom Telecom, Comviva, Netcracker, Optiva, Inc.Growth Accelerators

The global telecom billing and revenue management market growth is largely attributed to the increasing shift towards utilizing advanced billing solutions considering the rise in mobile data, internet, and digital content markets. Mostly, telecom services are adopting complex billing systems that are aimed at different pricing models such as pay-per-use, flat rate, and worked-up groups of services, among others, in order to make corrections in billing and enhance client satisfaction. With the expansion of the fifth generation, technology also calls for the need for more progressive billing systems in order to handle the offered services that include but are not limited to IoT, gaming, and cloud services, among others, hence pushing the market growth. The tendency to embrace digital transformation by players in the telecom sector is another factor that is expected to boost the market. Given the need for service providers to achieve operational efficiency, reduce overall costs, and improve revenue management, telecom corporations have also been making more and more investments in cloud-based billing and automated revenue assurance systems. The pressure for enhanced telecom billing systems is also resulting from the need for advanced integration of multiple services, such as mobile and broadband, as well as enterprise services.Telecom Billing and Revenue Market Segmentation analysis

The Global Telecom Billing and Revenue is segmented by Type, and Region. By Type, the market is divided into Distributed Mobile Operators, Internet Service Providers . Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The telecom billing and revenue management market on a global scale has numerous key players providing end-to-end billing systems for telecom companies, which presents a challenge in the market. This market is occupied by some of the largest billing solution providers, such as Amdocs, Ericsson, and Huawei, who offer end-to-end solutions that include revenue management, customer care systems, as well as analytics. These companies face competition due to their innovative designs in providing more complex solutions for telecommunications operators that have additional services like multi-service billing, real-time billing capabilities, and support for the upcoming technologies, including 5G networks and the Internet of Things (IoT). The importance of innovation and the trends, including cloud-based features, AI-based analytics, and many others, also form the basis of the competition among the companies. Apart from the bigger and older players in the market, there exists a serious threat from niche and regional market vendors who focus on billing-related functions but quite differently using the likes of fraud billing, prepaid billing, and awarding of bills in digital contents. These smaller firms usually compete mainly in terms of cost and the ability to provide solutions suitable for a particular market or region of telecommunications.Challenges In Telecom Billing and Revenue Market

The billing and revenue management sector of the telecom industry presents numerous issues, the most prominent being the making of the billing systems. Telecoms are adopting more and more complicated services, including bundled services, subscriptions, and pay-as-you use models, which all need complex billing systems for effective management and processes of different pricing strategies. And, next-gen services billing, for instance, 5G, IoT, and cloud services, increases billing complexity further, requiring near real-time processing and deployment of intelligent technologies. This, in turn, complicates the maintenance of billing accuracy and customer satisfaction, which is highly difficult in the first place, especially for big players with millions of subscribers. The question of revenue leakage presents yet another challenge. Revenue leakage is the inability of telecom operators to properly capture or bill for certain services offered due to systems’ limitations, malfunctions, or even dishonesty. The revenue leakage, which in most cases is attributed to old billing systems, can result in loss of potential revenue and limit profitability. In addition, the operational load is increased due to the risk of cyberattacks and data breach incidents, as well as the need to comply with regulatory obligations. Telecom providers have to enhance their defences against possible attacks and meet the demands of the changing business environment that has tougher laws globally, which integrates even more pressure in the already stressed market.Risks & Prospects in Telecom Billing and Revenue Market

The global market for telecom billing and revenue management offers ample avenues of growth primarily from the upsurge of 5G networks and growing demand for sophisticated telecommunications services. Telecom operators are at the moment seeking advanced billing solutions that will be easy to implement, high-complexity, and varied pricing strategies, subscriptions, and real-time billing for data and IoT devices, as well as OTT services. The billing systems incorporate artificial intelligence and machine learning together with process automation. Presents an opportunity for service providers to streamline revenue enhancement, customer satisfaction, and operational costs. In addition to that, the rising penetration of the cloud-enabled infrastructures and the need for adaptive and scalable billing solutions represent another major market driving force. To improve operational effectiveness, decrease capital expenditures, and provide more flexible service offerings, telecom operators are progressively adopting cloud-based billing solutions. The blooming of mobile payment systems and digital wallets, as well as the provision of cross-border telecom services, creates new types of billing solutions that are capable of managing international transactions, foreign currency exchange, and multi-currency billing systems.Key Target Audience

The primary customer base for the worldwide telecom billing and revenue market consists of providers of telecommunication services, such as cellular network operators, ISPs, and cable television service providers. These businesses need powerful billing systems that can deal with different pricing strategies, subscription models, and customer billing periods without compromising on the accurate billing and collection of revenue. The telecom operators look for sophisticated billing applications that can provide billing processes that collect and bill for data ready for consumption, voice services, and value-added service solutions, as well as enterprise billing solutions with an aim of maximizing revenue while cutting down their running costs.,, The other important segment is composed of the resellers that are software vendors, system integration service providers, and consulting firms that offer billing solutions, cloud services, and billing revenue assurance. Such providers seek out striking billing system solutions for the telecom operators who wish to upgrade their current billing systems and enhance service delivery for their customers as well as flexible pricing solutions.Merger and acquisition

The recent activities in mergers and acquisitions in the telecommunications billing and revenue management systems in the world denote the continuing industry trend focused on improvement of the technological aspects, especially now that cloud and 5G technologies are coming into play. For example, CSG Systems International has introduced cloud solutions such as Ascendon Communications and the Mediation platform, whose objective is to increase the agility of service providers and meet the demands of modern service provision systems with a focus on 5G. These progressions are in line with the high demand for flexible and scalable systems capable of managing the complexities of the networking and telecommunications enterprise structures in their new business model. Moreover, companies such as Oracle, Amdocs, and Netcracker have also been pursuing strategic M&A activity to build out their offerings. Amdocs, for instance, has continued to develop its billing systems with artificial and human intelligence to help telecommunications firms transition into digital service providers. In the same way, the relationship between the likes of Netcracker and telecom operators is bringing about the implementation of innovative billing systems while ensuring compliance with regional regulatory requirements. These trends are some of the several reasons that have seen firms making huge investments in upgraded billing systems more than ever before in order to provide better customer service, more efficient collection management, and faster deployment of 5G services.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Telecom Billing and Revenue- Snapshot

- 2.2 Telecom Billing and Revenue- Segment Snapshot

- 2.3 Telecom Billing and Revenue- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Telecom Billing and Revenue Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Mobile Operators

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Internet Service Providers

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Telecom Billing and Revenue Market by Component

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Solutions

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Services

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

6: Telecom Billing and Revenue Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Amdocs

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Cerillion Technologies Ltd

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Comarch SA

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 CSG Systems

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Inc.

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Formula Telecom Solutions Ltd

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Oracle

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 SAP SE

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 STL Tech

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 SUBEX

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Telefonaktiebolaget LM Ericsson

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Huawei Technologies Co.

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Ltd

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 Intracom Telecom

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Comviva

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 Netcracker

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 Optiva

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

- 8.18 Inc.

- 8.18.1 Company Overview

- 8.18.2 Key Executives

- 8.18.3 Company snapshot

- 8.18.4 Active Business Divisions

- 8.18.5 Product portfolio

- 8.18.6 Business performance

- 8.18.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Component |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Telecom Billing and Revenue in 2030?

+

-

How big is the Global Telecom Billing and Revenue market?

+

-

How do regulatory policies impact the Telecom Billing and Revenue Market?

+

-

What major players in Telecom Billing and Revenue Market?

+

-

What applications are categorized in the Telecom Billing and Revenue market study?

+

-

Which product types are examined in the Telecom Billing and Revenue Market Study?

+

-

Which regions are expected to show the fastest growth in the Telecom Billing and Revenue market?

+

-

What are the major growth drivers in the Telecom Billing and Revenue market?

+

-

Is the study period of the Telecom Billing and Revenue flexible or fixed?

+

-

How do economic factors influence the Telecom Billing and Revenue market?

+

-